This Duratec (ASX:DUR) analysis was originally posted on February 1, 2024. This is an updated version from 29/3/2024.

About

Duratec Limited (ASX:DUR) is an Australian company specializing in the assessment, protection, remediation, and refurbishment of various assets and infrastructure, particularly focusing on steel and concrete. Founded in 2010, Duratec operates through several segments, including Defence, Mining & Industrial, Building & Facade, and Energy. The company provides a wide range of services such as asset protection, building refurbishment, infrastructure upgrades, recladding, durability engineering, specialist access systems, construction, and spatial integration. Duratec leverages in-house assessment technologies, including 3D capture and modeling with predictive analysis tools, to deliver solutions across industries like defence, mining, building, and energy. The company has grown its presence across all Australian states and territories, working with clients in sectors that have different business cycles, aiming for sustainable growth and shareholder value by maintaining high standards of corporate governance and ethical conduct.

https://www.duratec.com.au/

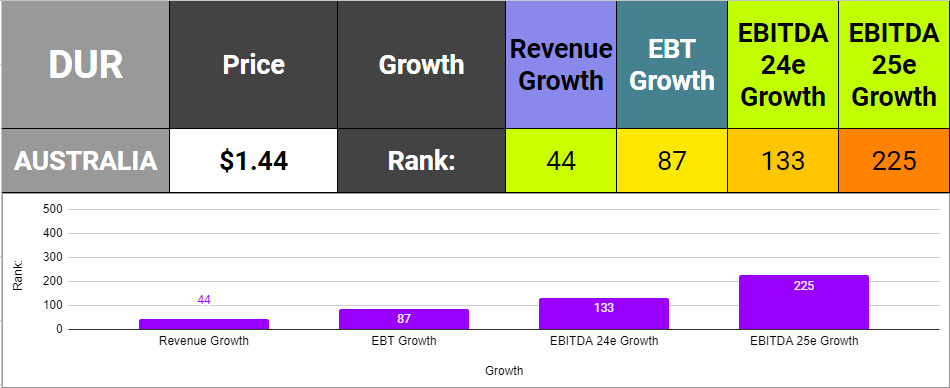

Growth rankings

Present and predicted future growth is in the top of half of the 500 stocks I track. The latest results have been stronger than what analysts predict to come. That could easily change though.

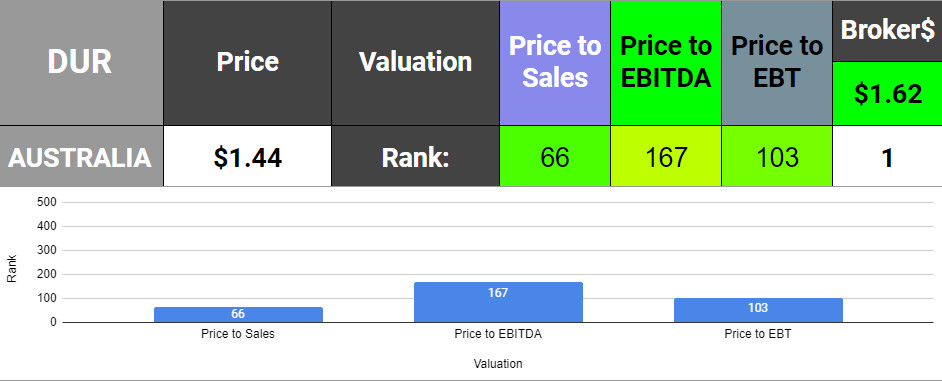

Valuation rankings

Duratec (ASX:DUR) looks relatively inexpensive on a the three valuation measures I look at:

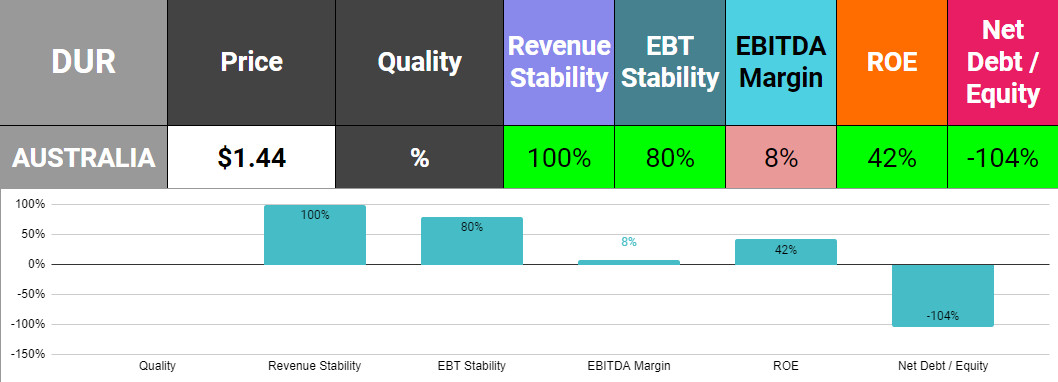

Quality rankings

By almost all measures of quality that I give weight to, Duratec (ASX:DUR) is a high quality to company. Only EBITDA Margin is lower than I like to see. Encouragingly, it has been increasing though.

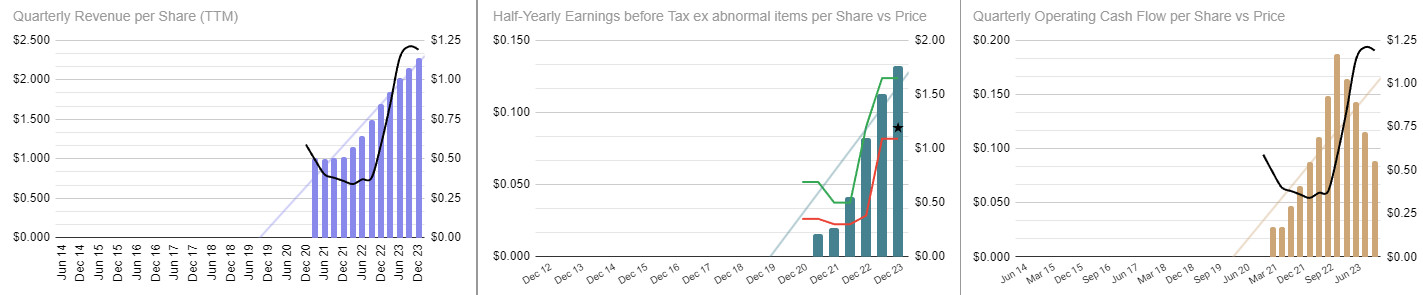

Fundamentals

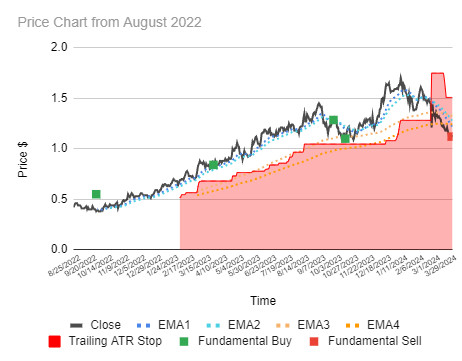

Duratec (ASX:DUR) Price chart

Duratec (ASX:DUR) Final Thought

The share price rose from around 30c in mid-June 2022 to around $1.70 at the start of this year. Since then, the stock has been falling. Growth levels look solid, valuation doesn’t appear stretched and quality looks to be improving. Revenue growth has been rapid and consistent and earnings have followed. The only concern has been falling operating cash-flows. In the past, I have seen examples where the cash-flows have signalled signs of problems ahead of earnings. Caution is justified right now. However, any sign of improvement in this metric along with continued improvement in revenues and earnings in their next update, should see a resumption to the uptrend in the share price.

Note: This is a live chart. The technical analysis in this report should be considered up to the date of this report.

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Duratec (ASX:DUR) Analysis