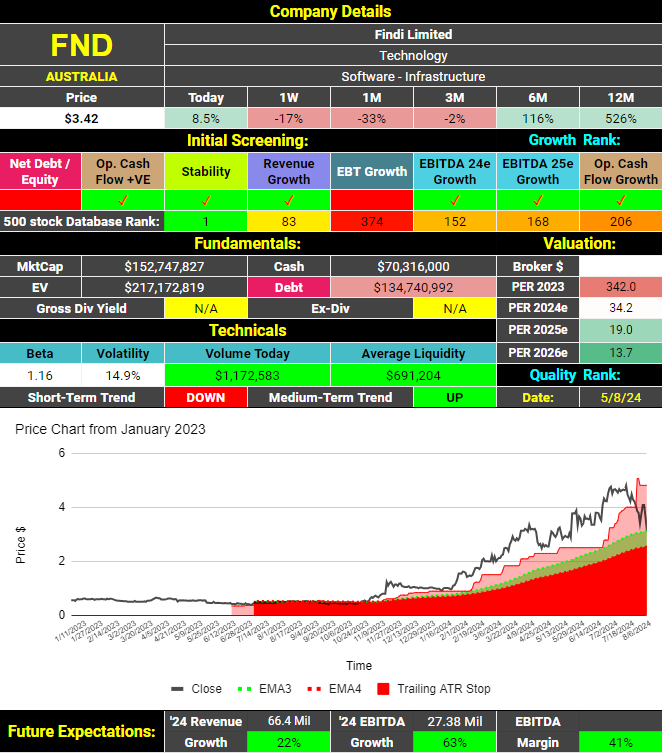

Initial Financial and Technical Screening

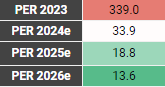

The latest report shows an increase in operating cash flows and revenues on a trailing 12-month basis. The company maintains a strong cash position and chooses to reinvest in the business rather than paying dividends. Analysts forecast EBITDA growth for 2025, although at a more moderate level compared to 2024. The stock currently has a P/E ratio of 34, which isn’t cheap, but strong growth is anticipated. This suggests that the valuation could improve significantly over the next couple of years.

Technically, the medium-term price trend remains upward, though the short-term trend has recently turned negative. Despite a decline of over 33% in the past month, the shares are still up an impressive 526% compared to 12 months ago. The only notable downside is that the company failed to increase earnings before tax and abnormal items in the last report.

Fundamental Analysis

Findi listed on the ASX in 2007 as Vortiv and rebranded on August 24, 2022.

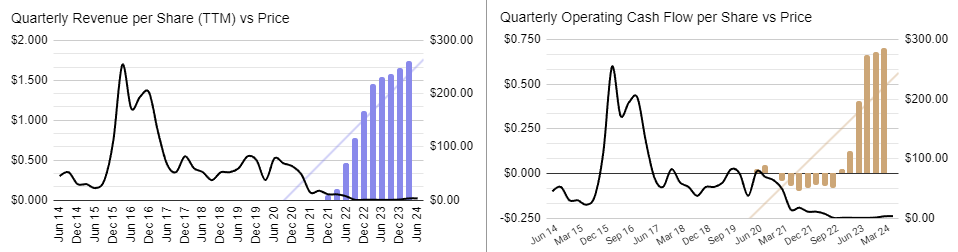

Since the rebranding, revenues and operating cash flows have shown steady and consistent growth.

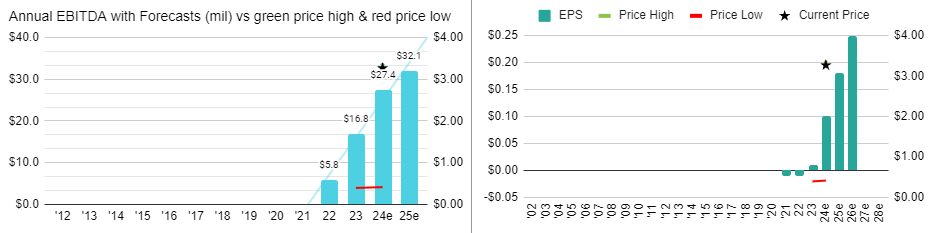

Likewise, EBITDA and Earnings Per Share (EPS) have been increasing and are forecast to continue to do so.

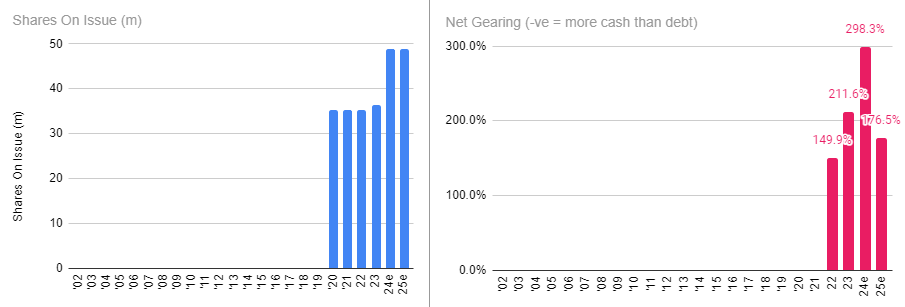

The company has financed its expansion through a mix of cash flows, equity, and debt. Shareholders have experienced significant dilution more recently mainly due to the conversion of options.

Findi (ASX:FND) does not feature at all on the ASX list of most shorted stocks. With a market cap of only ~$150M, it’s too small.

Quality Assessment

So far revenues have increased every time since the company changed its name to Findi. Earning before tax and abnormal items have been more inconsistent. Margins and return on equity (ROE) are acceptable and, more importantly, improving. The company is funding some of its expansion with debt but with positive cash flows and a healthy cash balance, this is of no concern at this time. Overall, Findi is an emerging company that could currently be classified as medium quality. However, if its current trajectory continues, it could be considered high quality in the coming years.

Valuation Considerations

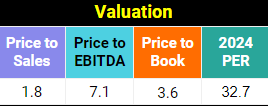

All of these metrics look reasonable for an emerging growth company. Based on analyst projections, the price-to-earnings ratio (PER) is expected to fall below 20 next year and under 15 the following year. Of course a lot can happen between now and then and being a small company, there may only be one analyst covering it. I cannot apply my valuation model to Findi as it has not been listed long enough.

All of these metrics look reasonable for an emerging growth company. Based on analyst projections, the price-to-earnings ratio (PER) is expected to fall below 20 next year and under 15 the following year. Of course a lot can happen between now and then and being a small company, there may only be one analyst covering it. I cannot apply my valuation model to Findi as it has not been listed long enough.

Recent News From The Company

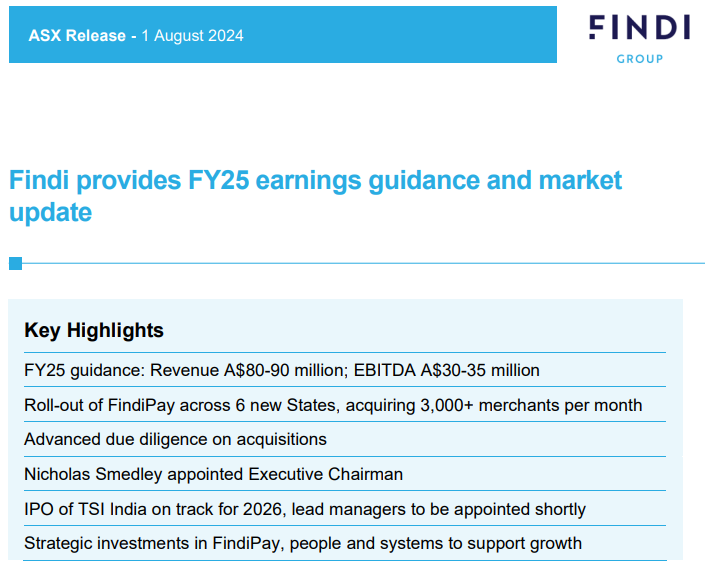

The company recently raised its revenue guidance while maintaining its EBITDA forecast. This suggests additional revenues may be allocated to expansion costs. The upcoming Indian IPO offers potential benefits and risks. It could lead to shareholder dilution but might also result in a higher valuation multiple. The success of the IPO will depend on the prevailing conditions in the Indian stock market. While the market has been buoyant recently, conditions could change.

Technical Analysis

Findi’s share price rose significantly from October 2023 to July 2024. However, it has since fallen 37% over 39 days. The short-term uptrend has paused, with the share price recently finding support around $3.20. This level aligns with the 38.2% Fibonacci retracement level. Investors will hope for a bounce and a move back toward the $3.86 level. If this support fails, the next level to watch is $2.67, which aligns with the 50% retracement level. The medium-term uptrend remains intact for now.

Concluding Statement

Findi Limited (ASX: FND) has strategically shifted its focus to Indian operations, particularly through its substantial stake in TSI India. The company’s consistent growth in revenues, operating cash flows, and earnings demonstrates a strong upward trajectory, despite some shareholder dilution from increased equity. With a P/E ratio expected to drop below 20 next year, the market may not yet fully appreciate Findi’s growth potential. The recent 37% decline in share price has brought the stock to a more attractive valuation level, potentially offering an entry point for investors confident in the company’s long-term prospects.

The upcoming Indian IPO represents a pivotal moment for Findi, presenting both opportunities and risks. A successful IPO could unlock a higher valuation multiple and provide additional capital for expansion, though it also carries the potential for shareholder dilution and the effects of market volatility in India. Overall, while Findi faces some near-term uncertainties, its strong financial foundation and strategic focus on the high-growth Indian e-transactions and payments market position it well for future success. The growth outlook for this emerging fintech company remains promising.

ABOUT STOCKS UNDER THE HOOD

If you’re an active investor or would like to become one, Stocks Under The Hood is your ideal companion. I provide a wealth of educational resources, including detailed company dashboards, in-depth reports, and model portfolios. My goal is to help you cut through market noise with clear, actionable insights and educational content, empowering you to make informed investment decisions. With a strategic, growth-focused approach, I guide you toward the best opportunities in the market.

A FREE 14 Day TRIAL is available enabling you full access to the site (just provide your name and email address – no credit card is required). You will then be able to view all of the Stock Reports, Company Dashboards, and two Model Portfolios. ALSO, request ONE STOCK OF YOUR CHOICE from the Australian or US market and I will do a full stock report for you.

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Findi (ASX:FND) Analysis