Let’s have a look at some companies reporting today.

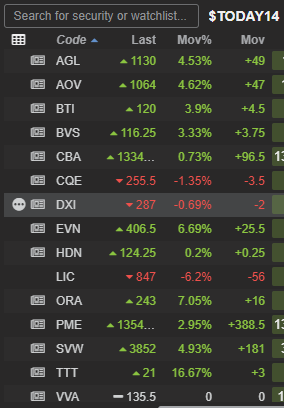

Reporting Season 14/08/2024 Watchlist at Market Close

In the end, the big winner was ASX:BVS which for mine, clearly had the best result in terms of beating expectations.

It’s been a tough 4 or so years for this company but today’s result goes a long way to supporting the argument that it’s finally turning things around. At the moment it remains a cost-out story but management seem confident they can return ASX:BVS to growth. If so, this one clearly has a lot of upside potential.

Reporting Season 14/08/2024 Watchlist at 10:28AM

A good day to report with the market up 46pts.

Seven Group Holdings ASX:SVW

https://www.sevengroup.com.au/

In-line / Slight Miss

Revenue: $10.6B vs $10.818 expected (up 10% on last year)

EBITDA: $1.93B vs $1.938 expected (up 14% on last year)

Outlook: 25FYe EBIT “High single digits growth” vs 9.6% forecast

A solid chart perhaps ready to start a new uptrend

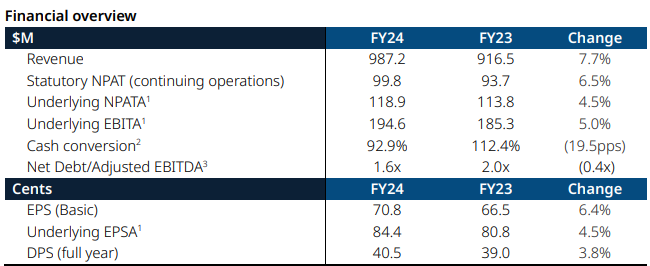

Amotiv ASX:AOV (Formerly GUD Holdings)

In-line (according to the company)

The name change, the sale of one business and the acquisition of two new ones seems to have thrown my data provider. The only data that appears comparable is Revenues.

Revenue: $987.2M vs 993.29M expected (up 7.7% on last year)

Outlook: Forecast for Revenue and EBITDA growth in 2025.

The company says that the result is in-line with forecast. We’ll find out if the market agrees at 10:10AM.

Bravura Solutions ASX:BVS

https://www.bravurasolutions.com/australia/

Beat

Return of capital and share buy-back.

Revenue: $250.4M vs $248.81M expected (up 0.34% on last year)

EBITDA: $25.8M vs $21.03M expected (up from negative last year)

NPAT: $8.777M vs $6.85M expected (up from negative last year)

Outlook: Earnings to grow but revenue to fall due to removal of one-off items.

Evolution Mining ASX:EVN

https://evolutionmining.com.au/

Beat

EBITDA: $1428.3M vs $1399.02 (up 69% on last year)

AGL Energy ASX:AGL

Beat

Underlying EBITDA: $2216M vs $2168.5M expected (up 63% on last year)

Underlying NPAT: $812M vs $795.6M expected (up 189% on last year)

Outlook: EBITDA: $1870 – $2170M vs %1967.9M expected

Viva Leisure ASX:VVA

In-line

Revenue: $163.6M vs $162.64M expected (up 15.9% on last year)

EBITDA: $35.4M vs $35.82 expected (up 21% on last year)

Outlook: More growth but no numbers provided.

ProMedicus ASX:PME

Slight Beat

Revenue: $161.5M vs $161.8M expected (up 29.3% on last year)

EBT: $116.5M vs $112.46M expected (up 35.3% on last year)

NPAT: $82.8M vs $80.13M expected (up 36.5% on last year)

No outlook given

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Reporting Season 14/08/2024 – Today I have a look at ASX:SVW, ASX:AOV, ASX:BVS, ASX:EVN, ASX:PME, ASX:VVA and ASX:AGL