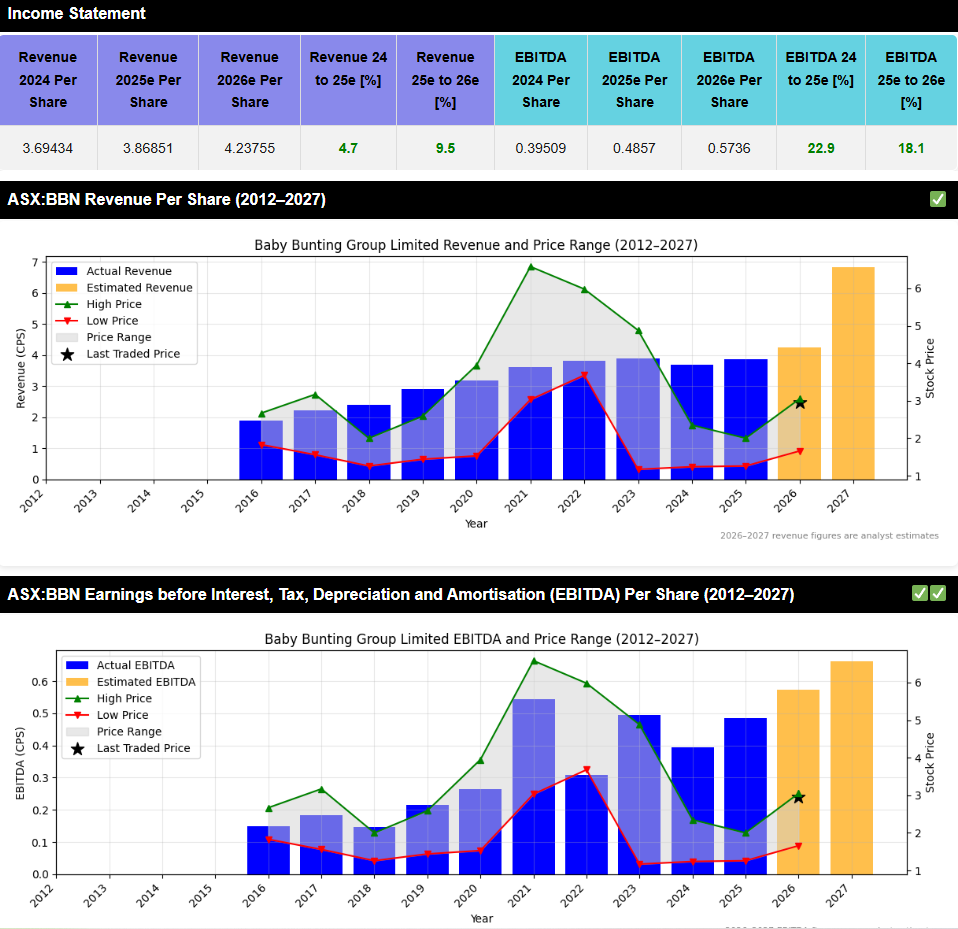

A Busy Engine Behind a Calm Ride

When you look at the performance tables, the Plato Global Alpha Fund (ASX:PGA1) jumps off the page.

Since its strategy began in 2021, it has delivered returns in the mid-20s per annum (after fees), against low-teens for the MSCI World Net Returns Index – roughly 12 percentage points of excess return per year over a strong global bull market. That kind of result gets attention, and it should. But it also raises obvious questions:

- What on earth is it doing to get there?

- How repeatable is it?

- And what risks sit under the hood?

PGA1 only listed on the ASX as a “complex ETF” in late 2024, providing a convenient vehicle for local investors to access the underlying Plato Global Alpha strategy. In this article I’ll focus less on the wrapper and more on the engine: what the portfolio actually looks like, how much it trades, and what that tells us about the way Plato is trying to generate “all-weather” alpha.

What is PGA1, in simple terms?

At its core, PGA1 is a global equity long/short fund:

- It owns (“goes long”) a large basket of shares it expects to outperform.

- It also shorts a large basket of shares it expects to underperform – that is, it sells borrowed shares and profits if they fall.

- It uses the cash from shorting to buy more longs, so the fund ends up with more than 100% of its capital invested on the long side, partly funded by those shorts.

In the latest update, the typical positioning looked roughly like this:

- Around 140–145% long

- Around 45–50% short

- Net exposure still close to 100% “in the market” – you’re not buying a market-neutral hedge fund, you’re buying a geared global equity exposure with an internal alpha overlay.

The process is systematic. Plato describes it as:

- A bottom-up, factor-driven stock selection model that scores companies on value, growth, quality and sentiment, and

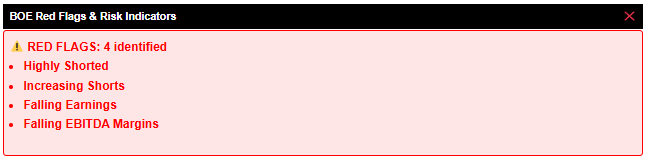

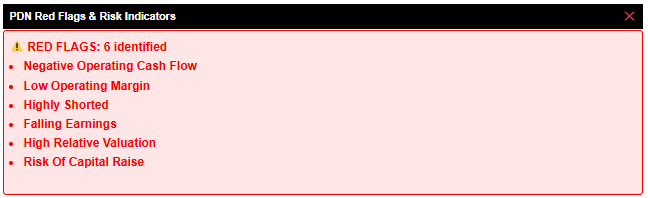

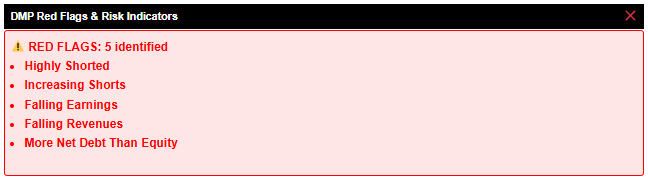

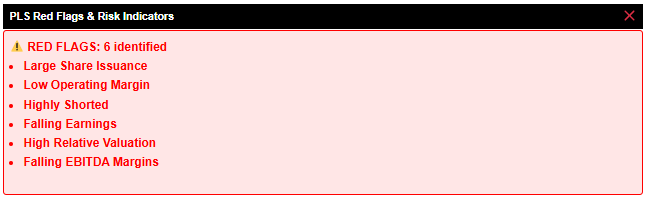

- A large “red flag” library (100+ checks) designed to spot accounting issues, balance sheet risk, earnings deterioration and other potential “landmines” – both to avoid on the long side and to target on the short side.

The result is not a concentrated “best 30 stocks” portfolio. It’s a very broad book:

- Over 1,000 long positions

- Several hundred short positions

- Each individual position is typically small – often measured in a few tenths of a percent of the portfolio, rather than big 5–10% bets.

That breadth and diversification are key to understanding what comes next.

Are they constantly churning the portfolio?

One of the simplest ways to test how a fund behaves is to compare what it owned at two different points in time.

For PGA1, I looked at two full portfolio disclosures:

- End of December 2024

- End of June 2025

These are the only two complete holdings snapshots we have so far, but they already tell us quite a bit.

1. Name turnover vs capital turnover

On a name count basis, the portfolio looks very busy:

- The December snapshot held about 1,260 individual securities.

- By June, this had increased to roughly 1,350 securities.

- Around 70% of the December names were still in the book by June.

- The remaining 30% or so had disappeared, and there were hundreds of new names in their place.

If you stopped there, you’d conclude the fund is churning through positions at a furious rate.

But when you look at capital, the picture is almost the opposite:

- Roughly 95% of the December portfolio by weight was still invested in the same names six months later.

- Only about 5% of the capital had been recycled into completely new positions that weren’t in the December list at all.

- Coming the other way, roughly 90%+ of the June portfolio by weight was already present in December; only high single-digits by weight were genuinely new.

In other words:

There’s lots of activity in the tails – many small positions coming and going – but the core capital is remarkably stable.

From a trading-behaviour point of view, PGA1 looks less like a trader jumping in and out of big bets, and more like a large, systematic engine continually re-sizing a huge number of small positions as its models update.

2. Long to short flips (and vice versa) are rare but meaningful

With a long/short fund, a good stress-test is to ask:

How often do they flip a stock from long to short, or from short to long?

Between December and June, only a handful of names did a full U-turn:

- A small group moved from being net long (owning more than they shorted) to net short.

- A slightly larger group did the opposite.

Given the fund runs well over 1,500 aggregate positions, the fact that only a dozen or so names flipped direction over that six-month window tells you something:

- Most shorts are not “we hated it last quarter, now we love it” trades.

- They tend to be more structural expressions of the model – a stock sits in the doghouse for a while before earning its way out, and the position size moves gradually rather than whipping around.

When a name does flip from long to short or short to long, the change is usually meaningful in size. You’re seeing the model say, “This stock now scores very differently,” and the portfolio reflecting that.

What sort of companies does the fund actually own?

The October 2025 investment update gives a nice snapshot of the aggregate characteristics of the long book versus the index.

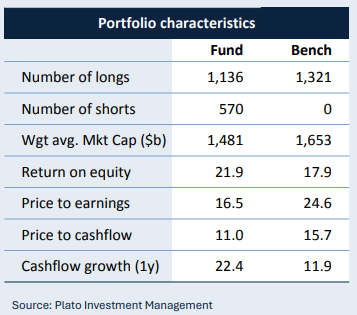

On average, the companies held long in PGA1 show:

- Higher profitability: return on equity around 22% vs ~18% for the benchmark.

- Faster growth: cash-flow growth roughly double that of the index.

- Cheaper valuations: price/earnings and price/cash-flow ratios notably lower than MSCI World.

So the long side of the portfolio, in broad terms, looks like “cheap quality growth”:

Companies earning strong returns on capital, growing faster than the average, but not trading at the most extreme growth-stock multiples.

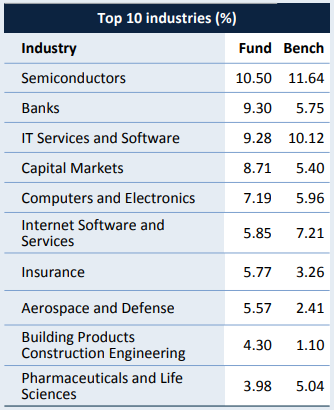

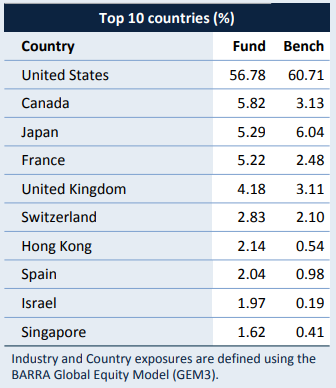

On the sector and country mix, the portfolio:

- Holds a big chunk in US mega-cap tech and AI winners (NVIDIA, Apple, Microsoft, Alphabet, Amazon, Meta, Broadcom and friends).

- Shows clear overweights to financials (banks, capital markets, insurers) and some real-economy cyclicals like building products and defence.

- Is underweight more defensive areas such as consumer staples and large-cap pharmaceuticals.

- Is biased to the US but with active tilts towards selected non-US markets (Canada, parts of Europe and Asia).

Meanwhile, several of the worst detractors over the prior year came from the short book – for example, short positions in some mining and energy names that rallied hard. That’s a useful reminder that:

The short side is very real in this strategy – when a theme the fund is shorting goes on a tear, it can hurt.

High active share, modest tracking error – why that matters

Two statistics in the update are worth dwelling on:

- Active share ~90%+

- Tracking error ~3–3.5%

Active share measures how different the fund’s holdings are to the index. At 90-plus percent, PGA1 is about as far from a closet indexer as you’ll find in a listed ETF.

Tracking error measures how much the fund’s returns typically wiggle around the benchmark over time. A figure around 3% is not especially high; many “high conviction” long-only global funds run tracking errors in the mid-single digits.

Putting those two together:

- At the stock level, PGA1 is very different to the index – it owns and shorts a huge number of names that aren’t in MSCI World at all, and is constantly re-sizing them.

- At the portfolio level, the combination of long and short baskets is engineered to keep overall risk close to the market in terms of volatility and beta.

For investors, the practical translation is:

You’re getting something that behaves a lot like a global equity fund in terms of overall risk, but looks nothing like the index inside the engine bay.

That’s both the appeal and the danger: if the process continues to extract alpha from its stock-picking and risk controls, tracking error stays “cheap”; if the process hits a rough patch, you feel it quickly.

Fees, incentives and what you’re really paying for

A strategy like this doesn’t come at index-ETF prices.

For the quoted ETF class (PGA1 on the ASX), the key elements are:

-

A management fee of 0.85% p.a. of the fund’s net asset value. Ordinary operating expenses are bundled into this.

-

A performance fee of 15% of any outperformance (after management fees and costs) relative to the MSCI World Net Returns Index (unhedged, in AUD). This accrues daily and is typically paid semi-annually when the fund has a positive performance-fee balance.

-

Indirect costs (for things like underlying vehicles and OTC derivatives) have historically been very small – estimated around 0.03% p.a. in recent disclosure.

For regulatory reasons, the PDS also has to quote an estimate of total “management fees and costs” that includes an assumption for performance fees based on the strategy’s actual history. Using performance up to 30 June 2024, that all-in figure comes out around 1.18% p.a. – effectively saying: “If future performance fees looked like they did over the last few years, the average ongoing cost would have been roughly this level.”

A few practical points:

-

You only pay a performance fee if the fund beats its benchmark after costs. If it underperforms for a while, the negative accrual has to be earned back before the manager gets paid again.

-

When the alpha engine is firing, performance fees can be material – which you can see indirectly in the fact that the long-term returns quoted are after both management and performance fees.

-

Compared with plain-vanilla global index ETFs (often in the 0.10–0.20% range), you’re paying a clear “complexity and skill” premium here. The real question isn’t whether the fee is high or low in isolation; it’s whether the net, after-fee outcome justifies owning a strategy like this at all.

In other words:

PGA1 is priced more like a hedge fund than a cheap index tracker – but so far, the net numbers have been strong enough that investors haven’t had to squint to see what they’ve received for that fee drag.

The risk, of course, is that if the alpha fades and the fee meter keeps ticking, the gap between fund and benchmark can close quickly – or turn the other way.

Performance so far: excellent, but don’t anchor on it

The scoreboard to 31 October 2025 looks outstanding:

- Since inception (Sept 2021): fund ~25–26% p.a. vs benchmark ~13% p.a.

- 1-year to October 2025: fund over 40%, benchmark around 22%.

- Upside capture: the fund has historically captured roughly 128% of rising markets.

- Downside capture: it has historically captured around 65% of falling markets.

In plain English:

So far, PGA1 has gone up more than the market in good times and fallen less in bad times, while running similar overall volatility.

That is exactly the shape of return profile investors dream about – hence the attention.

But a couple of sobering points are worth emphasising:

-

The track record, while not microscopic, is still one market cycle dominated by an enormous bull market in US growth and AI-related names.

-

A lot of the headline alpha has come from being on the right side of that regime – large positions in mega-cap growth winners, plus strong selection within the mid-cap and smaller-cap parts of the universe.

-

Quant strategies are not immune to prolonged drawdowns when their particular blend of factors falls out of favour.

Past performance – especially exceptional performance – is not a forecast. It’s evidence that the process has worked so far, in a particular environment.

What could go wrong?

No strategy is bullet-proof. Some of the key risks I’d flag, particularly for a fund like this, include:

Factor regime risk

The fund leans into a particular combination of value, growth, quality and sentiment signals. There have been long periods in history where some or all of those signals have gone cold. If the environment rotates in a way the model doesn’t handle well (for example, a sudden, sustained rotation out of quality growth and into deep cyclical value), underperformance can be sharp.

Short-book and leverage risk

Running ~140–150% long and ~45–50% short means the fund has gross exposure well above 100%. That’s fine as long as the alpha engine is working. If longs and shorts both move against the fund at the same time, losses can compound faster than in a traditional, unlevered fund.

Crowding and capacity

The underlying strategy now runs a material pool of capital. If many quant funds end up chasing similar signals in the same parts of the market, some of the edge can erode, and liquidity can dry up just when it’s least convenient.

Model risk and “unknown unknowns”

A big part of the appeal here is the red-flag library and the depth of the data the team uses. The flip side is that the behaviour of a large, complex model is always partly a black box to outside investors. You’re outsourcing a lot of decision-making to a process you can’t fully see.

None of these are arguments against the fund. They’re simply the other side of the coin when you venture away from traditional, long-only benchmarks into high-breadth, leveraged, long/short quant territory.

How I’d frame PGA1 in a portfolio conversation

Without making a recommendation, I’d summarise Plato Global Alpha (ASX:PGA1) like this:

- It’s not a simple “set and forget” global index tracker.

- It is a sophisticated, high-activity engine that:

- Runs hundreds of small long and short positions.

- Keeps the core holdings surprisingly stable over time, while constantly tuning position sizes at the margin.

- Seeks to own a portfolio of profitable, growing companies at reasonable valuations, and short those that fail a set of forensic-style red-flag tests.

- Has so far delivered very strong excess returns with index-like overall risk.

The key questions for any investor thinking about it are:

- Can the team maintain this level of alpha as assets grow?

- How does the strategy behave if we get a long period without a dominant US-tech/AI tailwind?

- Is the 4% p.a. targeted outperformance over MSCI World (after fees) a realistic long-term guide, or was the early period unusually favourable?

This is a complex, active global equity strategy inside an ETF wrapper. It may be a powerful diversifier, but it’s not a plain-vanilla index fund, and it deserves the same level of due diligence you’d apply to any specialist manager. Anyone considering it should read the Product Disclosure Statement, understand the risks, and think carefully about how a fund like this would sit alongside their other holdings and risk tolerance.

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Inside Plato Global Alpha (ASX:PGA1)