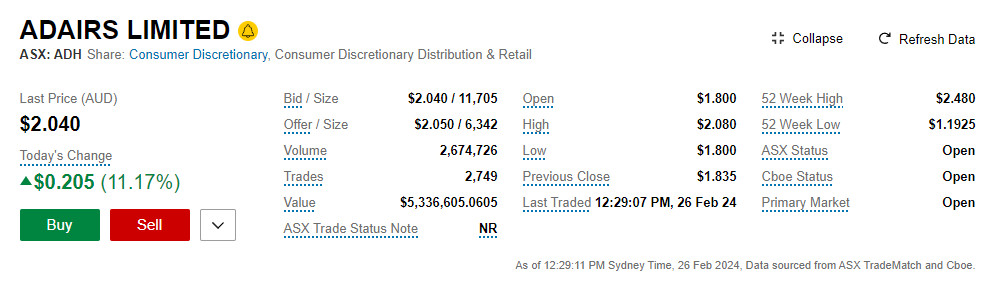

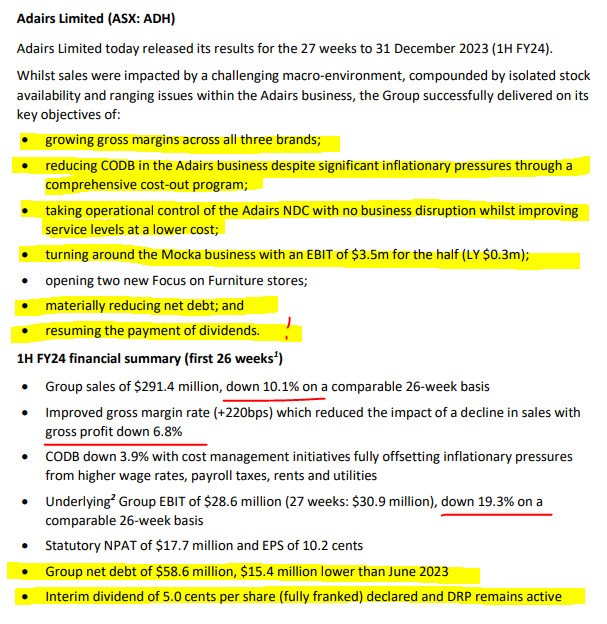

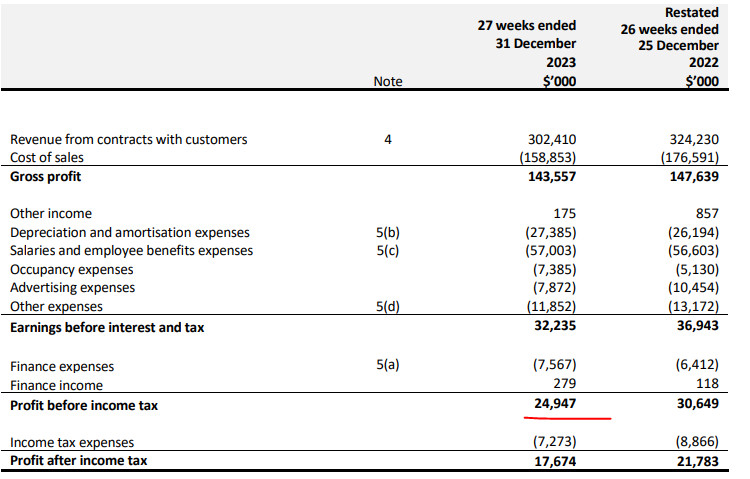

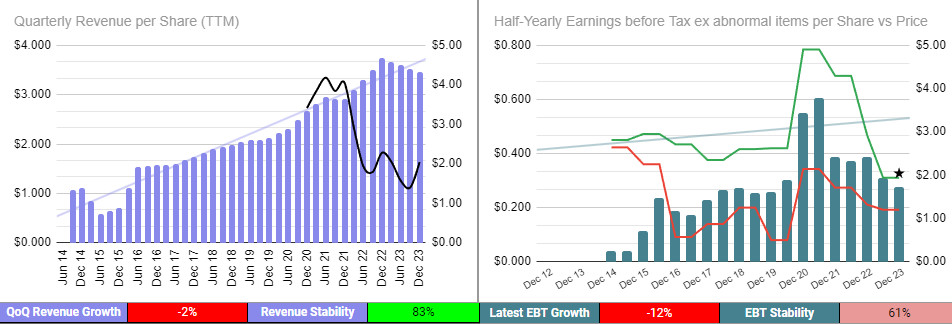

Tue Feb 27, 2024 ASX earnings & outlook observations along with a look at broader market movements. ASX:DGL, ASX:PNV, ASX:JLG, ASX:PSQ, ASX:PLY and ASX:TYR and are featured at today.

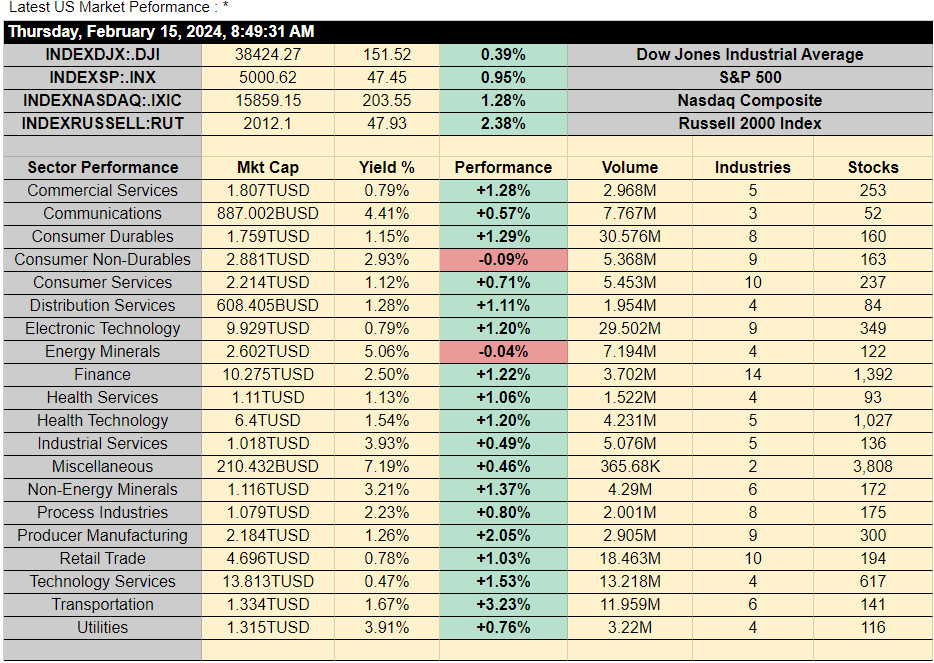

…. last update 11.47am

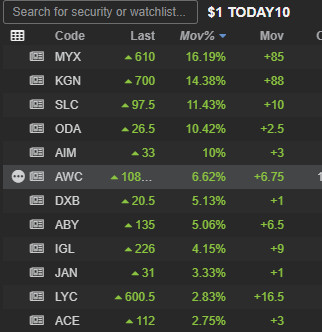

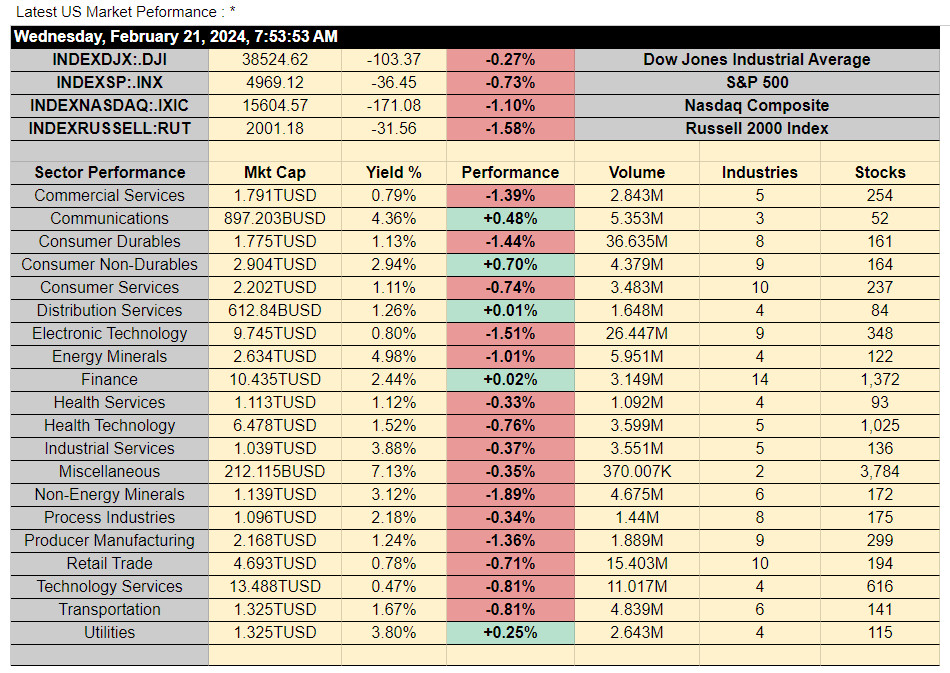

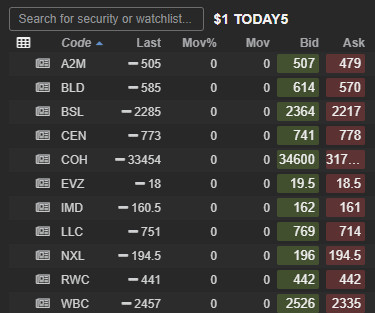

ASX AFTER THE OPEN

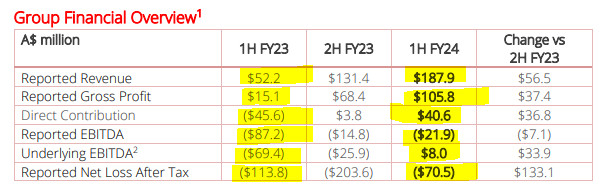

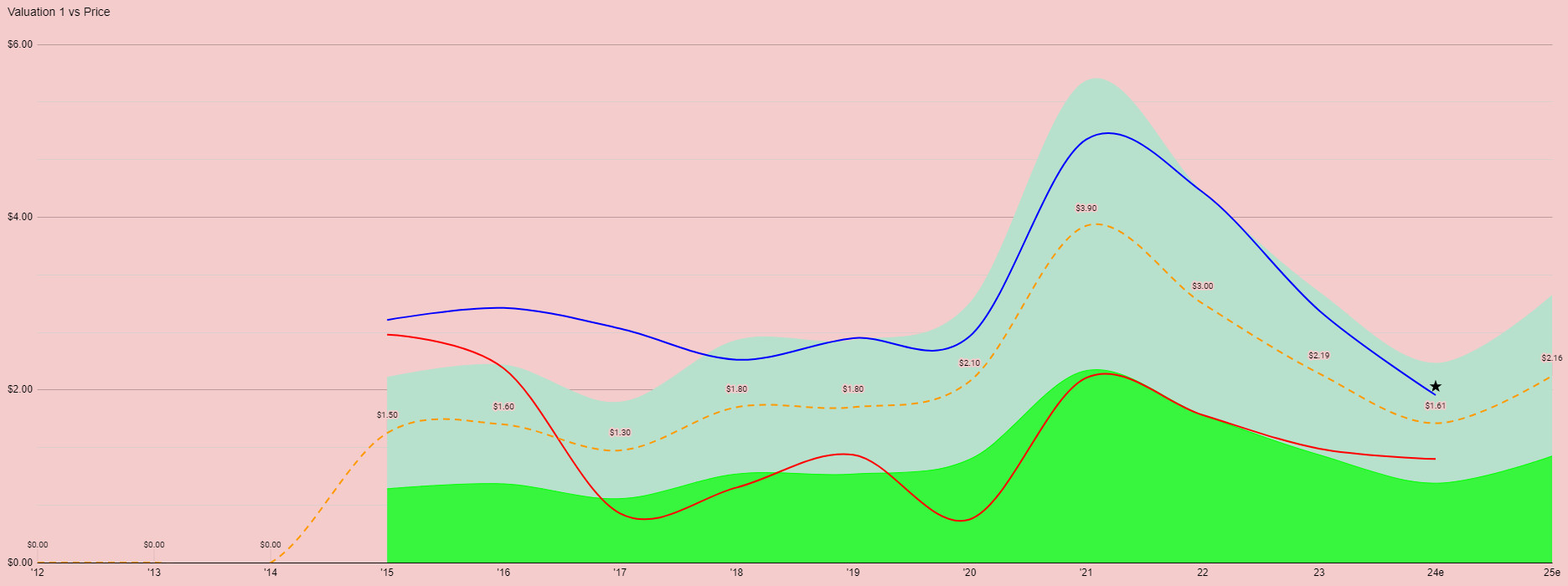

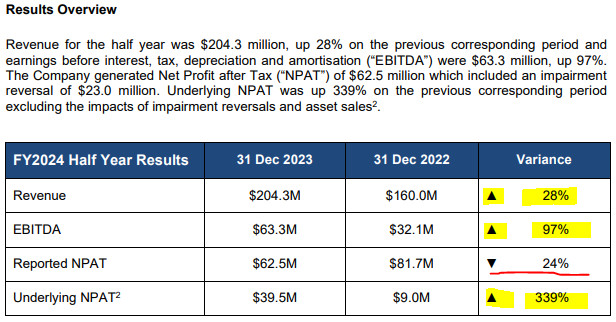

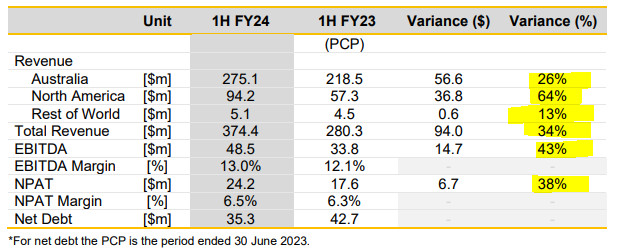

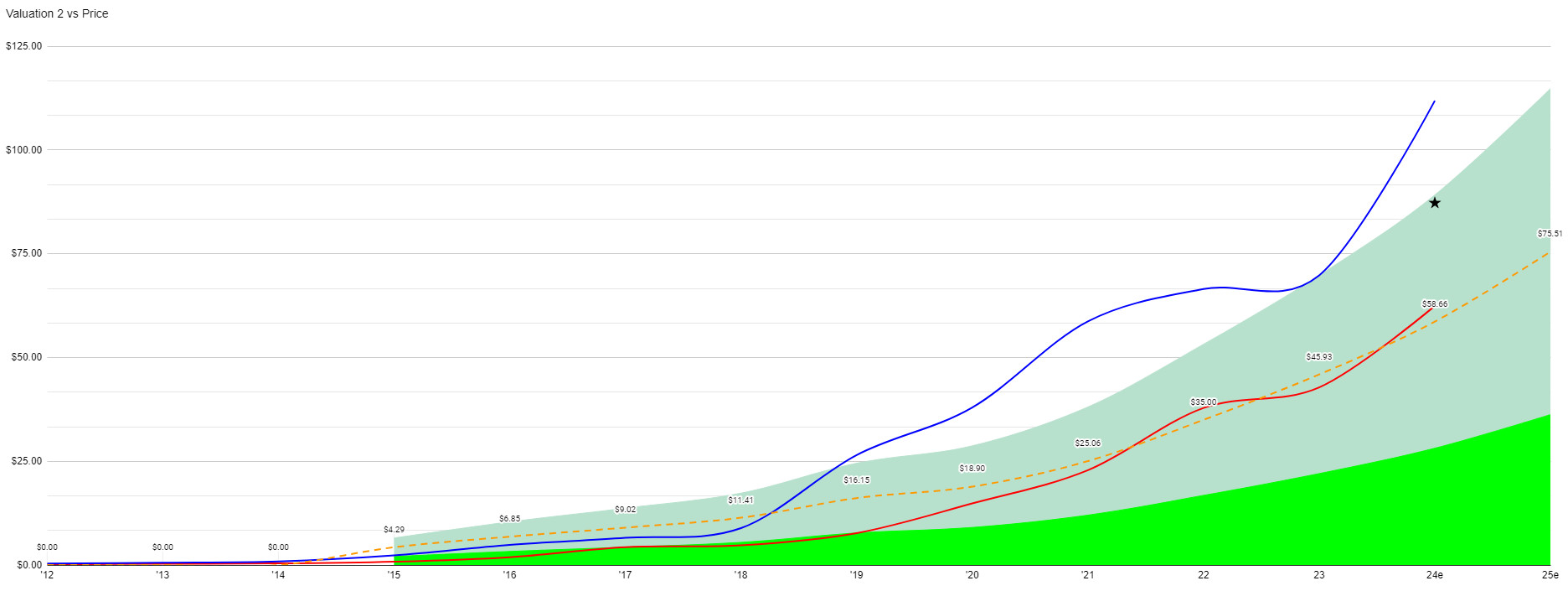

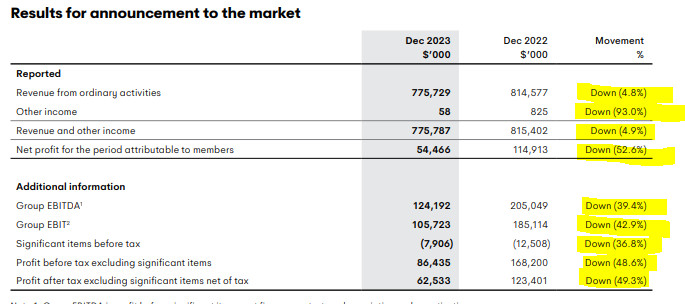

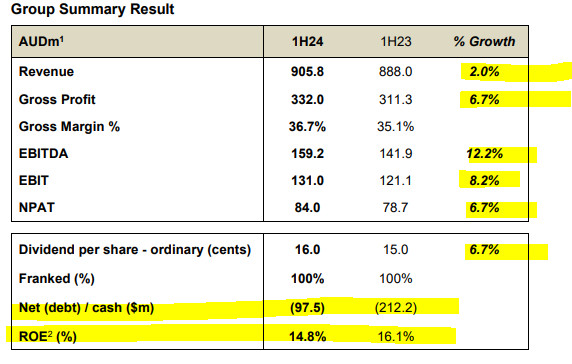

DGL Group (ASX:DGL)

https://www.dglgroup.com/

![]()

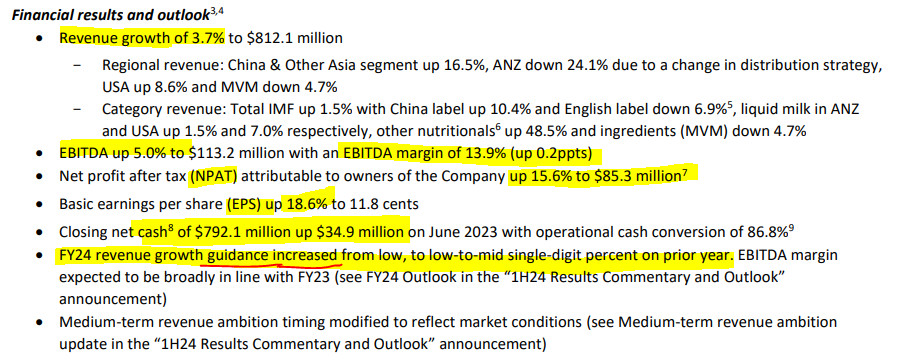

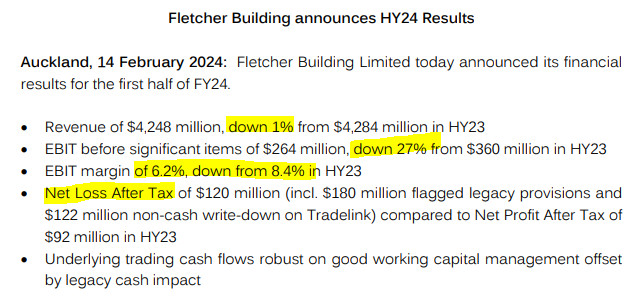

I’m unsure whether I should waste my time looking at this result. I am somewhat curious though.

Doesn’t sound amazing but doesn’t sound like it should be down 42%!

I’ll quickly run the numbers and see if there is anything lurking down below.

Ok I won’t bother posting graphs. This issue with this company, as I see it is … debt. They have $138.5M in borrowings. They only have $21M in cash. At today’s price the market cap of the company is only $171M. I’d say the market is getting worried that the company may need to do a rather substantial and dilutive capital raising to bring this back into balance.

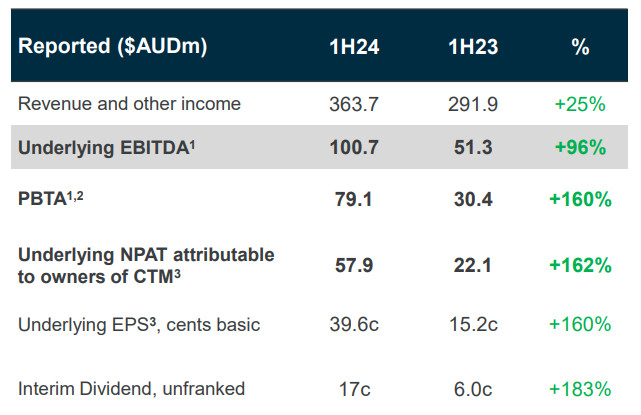

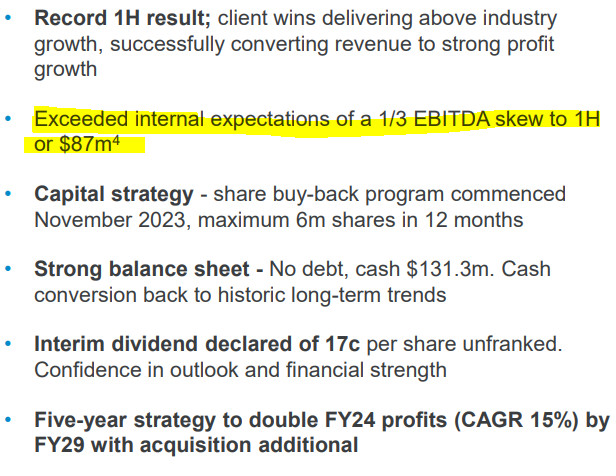

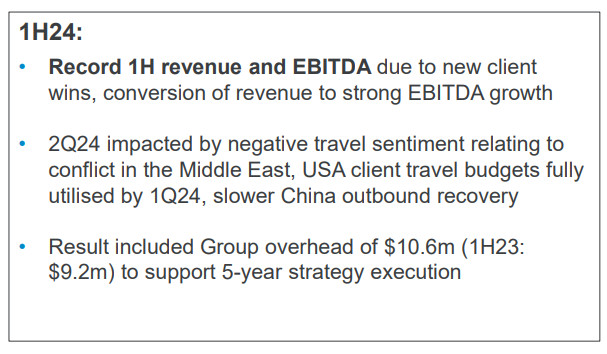

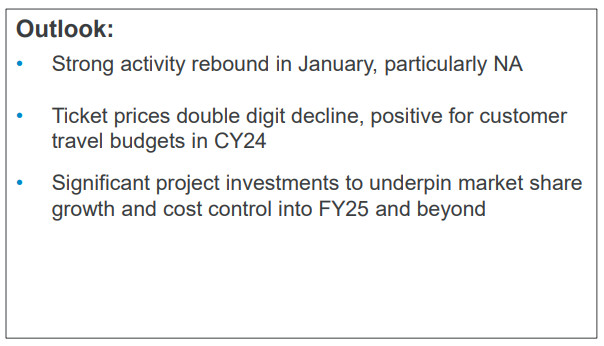

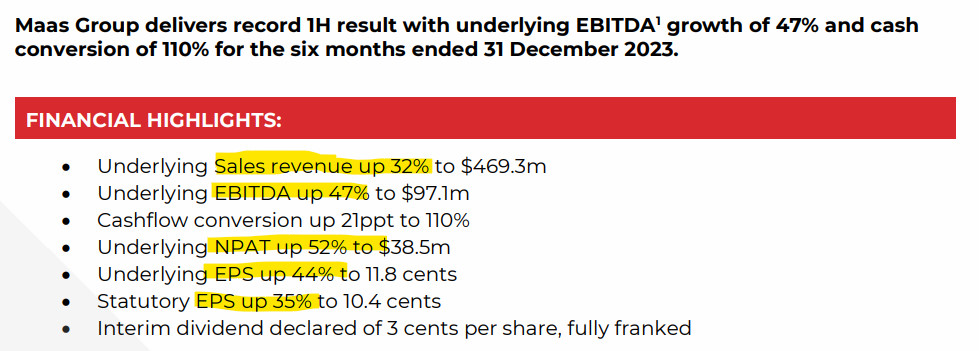

Polynovo (ASX:PNV)

https://au.polynovo.com/

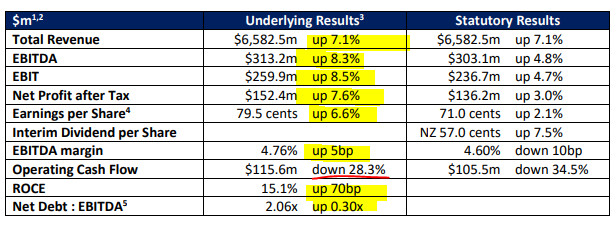

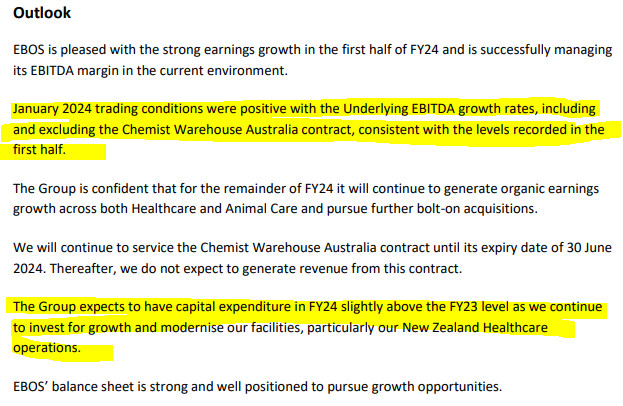

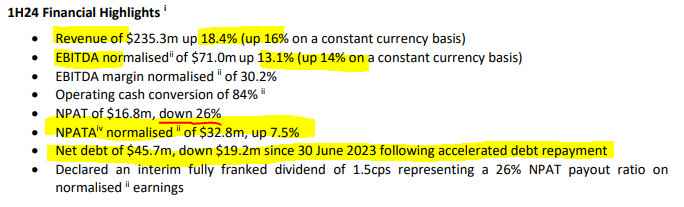

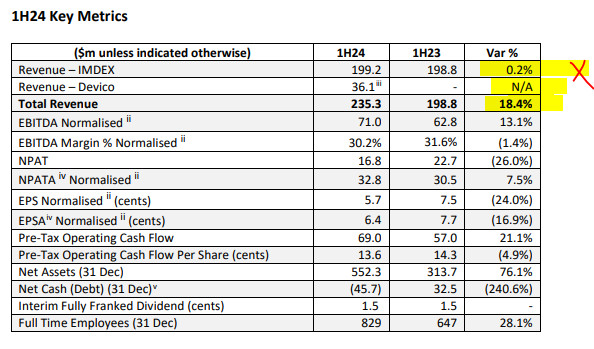

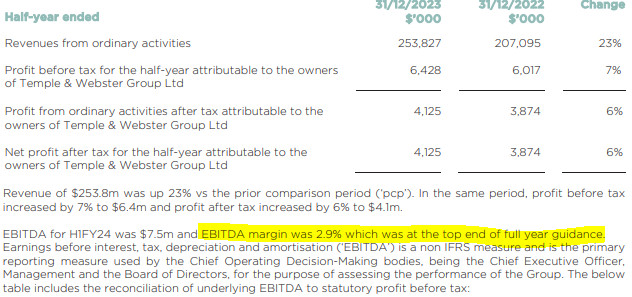

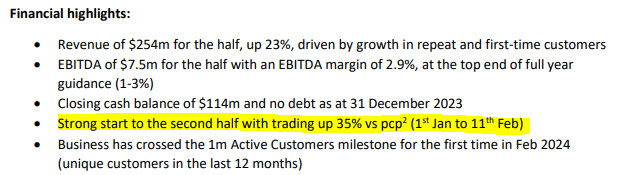

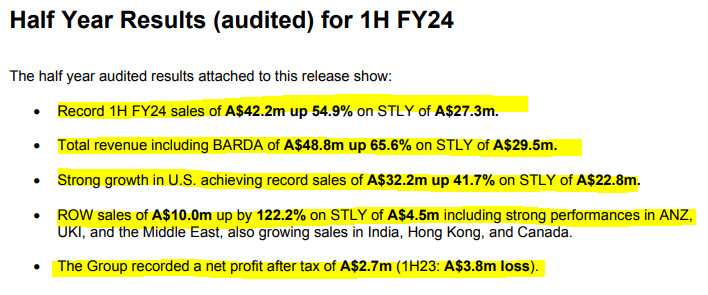

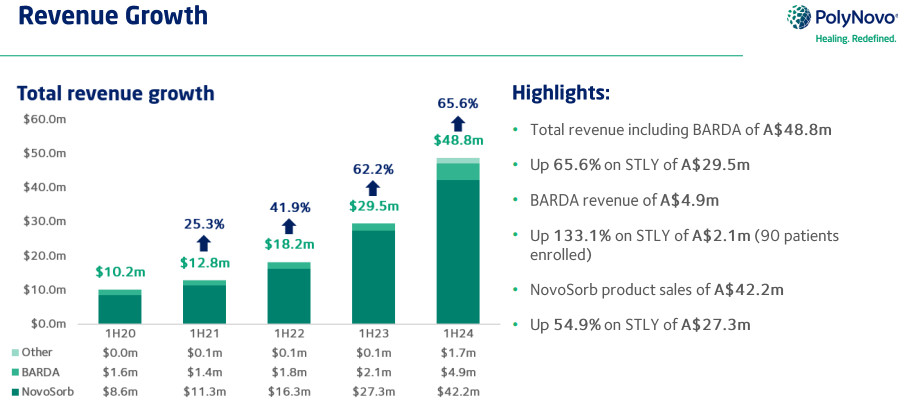

Just out is Polynovo (ASX:PNV) result.

Strange comment.

Presentation out after the first pause in trade. Another odd way to handle it.

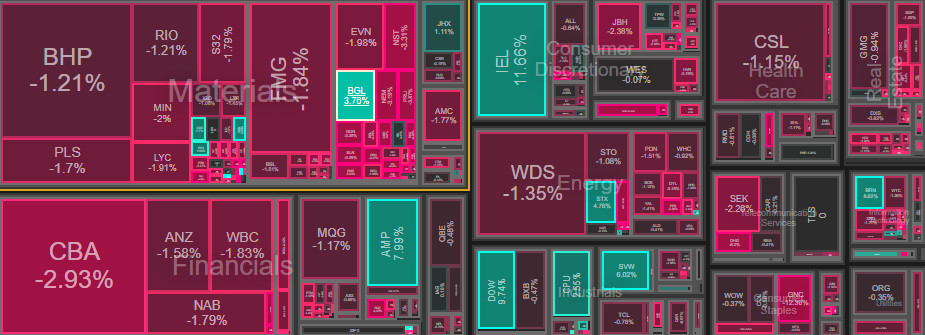

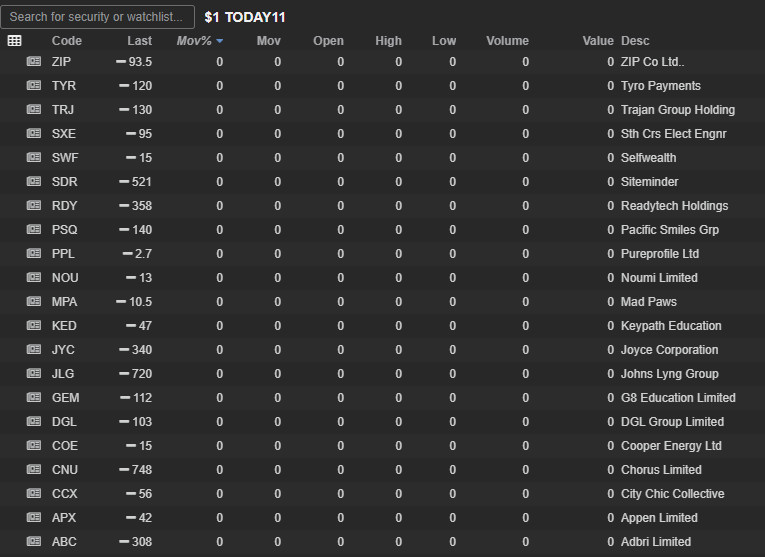

Some very big moves today on the back of announcements. Let’s look at a couple of the fallers.

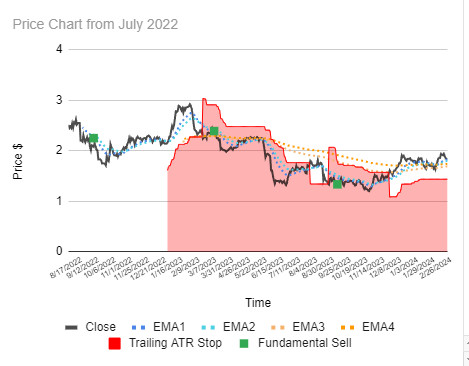

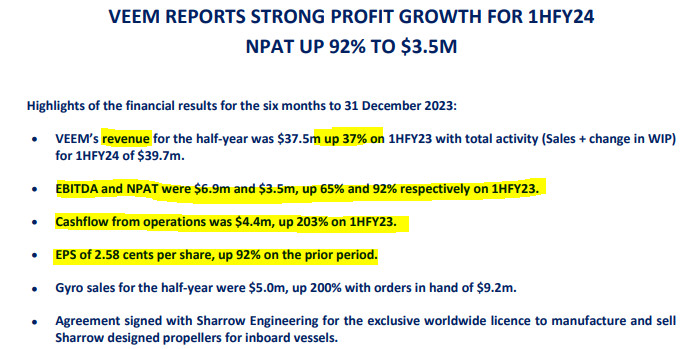

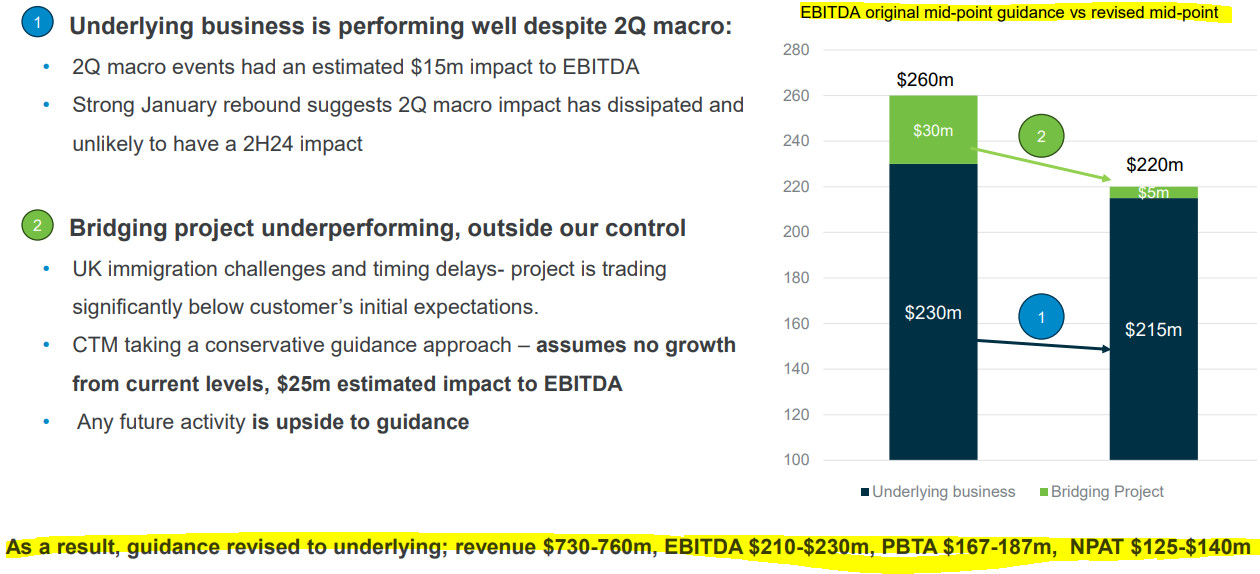

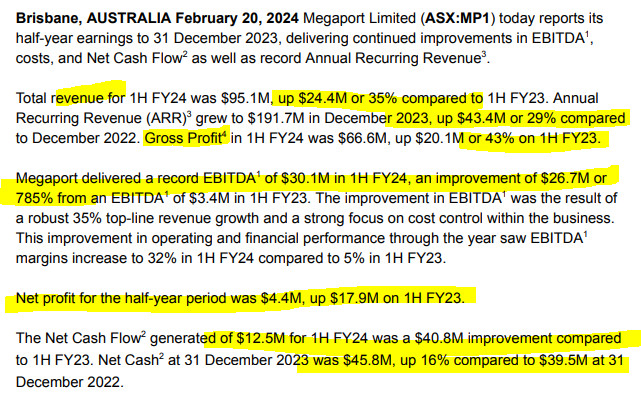

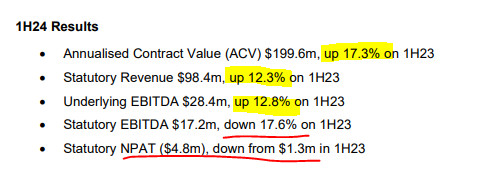

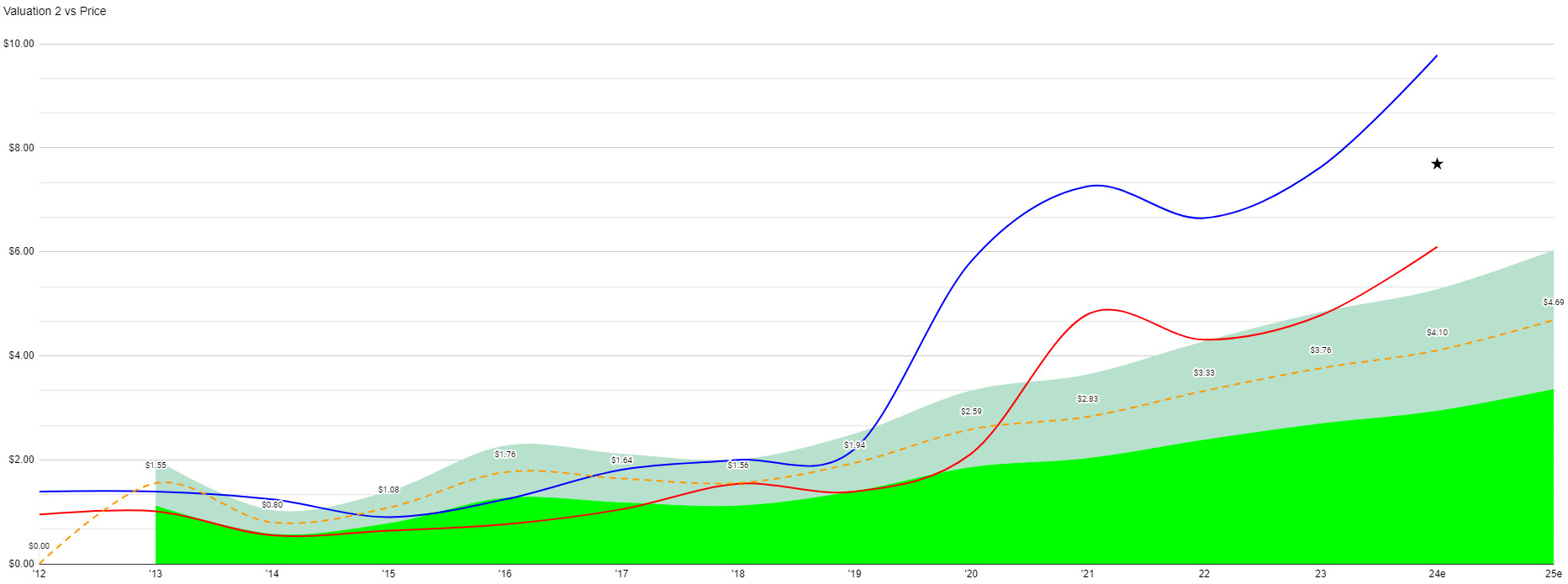

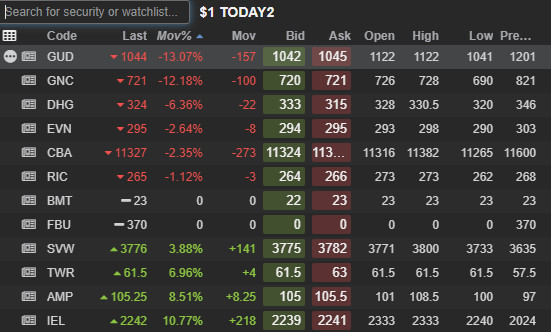

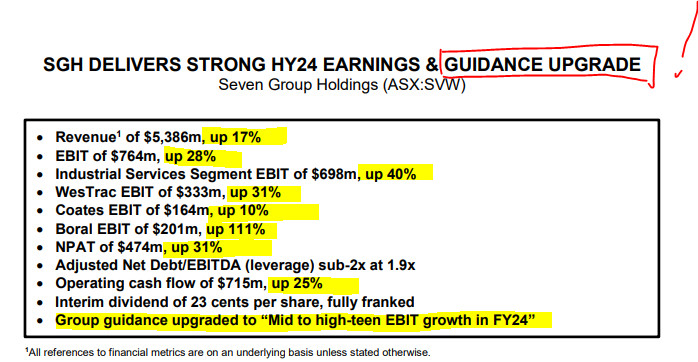

Johns Ling Group ASX:JLG

![]()

Curious they fell so much on an upgrade!

Will have to go digging deeper. Not the first stock to fall this reporting period on an upgrade. ASX:AUB did it then bounced the next day but remains lower today.

I think for now I’ll skip the presentation and just go straight to the financials because the numbers often tell their own story – the real one!

Ok I see a number of issues that you wouldn’t have suspected from reading that headline. Revenue, earnings and cash-flows are all down on the same period last-year.

Now maybe this is no big deal. Maybe they’re anticipating a big 2nd-half. I’m not going to read further to find out. What I will say is this. ASX:JLG has a PER of roughly 45 based on 2023 earnings. That’s very high. However, it’s enormous if the company is not growing. I like ASX:JLG. I think they’re in the right spot at the right time. However, over the past few years, every man and his dog has felt the same pushing the value of the company well beyond fair value. Today is the day that all of those people get a serious wake-up call.

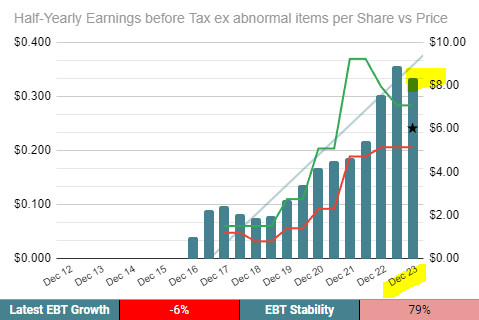

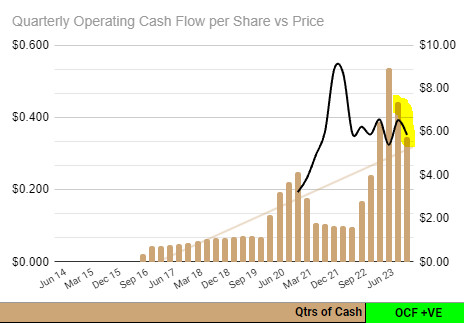

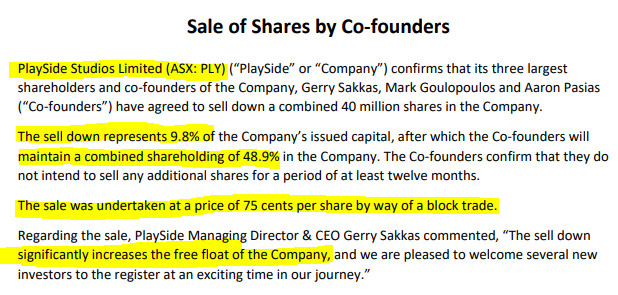

Playside Studios (ASX:PLY)

https://www.playsidestudios.com/

This is always an interesting situation. Founders are selling down shares in ASX:PLY. 10% of the company is a significant amount. To do so they have to sell at at discount. The shares will 100% of the time drop on this announcement because some of those that were lucky enough to buy the shares at 75c will attempt to take a quick profit. The share price opened at 81c so some certainly succeeded. It’s the nature of the game. The price was driven down to 72.5c. The shares are back to 75c which is what you would expect.

But is this announcement a positive or a negative for the company?

Some would say it’s negative as the founders are selling so they must think it’s a good time to get out. But on the other hand, they still own 50% of the company. You would think that for most of them that is still the bulk of their net worth so I would argue against that proposition.

ASX:PLY had a market cap of $335M before today. That sees them as the 560th biggest company on our market. They would be in some small cap and tech indices. Too small obviously for the ASX:300 just yet. However, weightings are not decided by market cap but by free float value. Director holdings are not considered part of the free-float. This will lift the weighting of the company in these indices. It gets them closer to being added to other indices. Indices are important for a number of reasons. It’s when institutions take an interest. More analysts will cover the stock. More people will become interested in the story.

In order for ASX:PLY to continue to grow and be recognised, more of it’s shares need to be available to trade. While the shares are down today and 75c will probably remain a resistance point until those looking for a quick profit can exit, the announcement can only be seen as an important step on the journey for a small cap to have any chance of one-day becoming an index recognised big-cap.

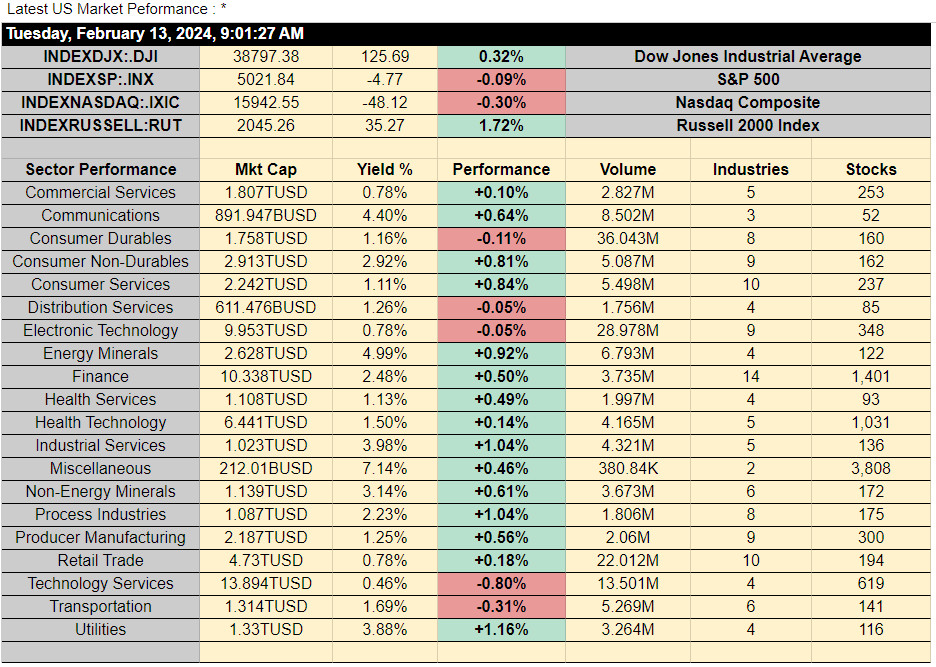

ASX PRE-MARKET

A quiet session in the US overnight sees our market set to open around 4 points lower.

The remain theme for our market remains earnings reports. This is today’s list so far (as at 9.16am)

Adelaide Brighton (ASX:ABC) is on the list because they are yet another building materials company that has received a takeover offer. That’s the third with Boral (ASX:BLD) and CSR (ASX:CSR) also currently sitting with bids. With the Australian dollar so low, ASX companies are sitting ducks and are getting picked off it feels at around 1 or 2 per day.

Prospa (ASX:PGL) is another company that has signed a scheme today I see.

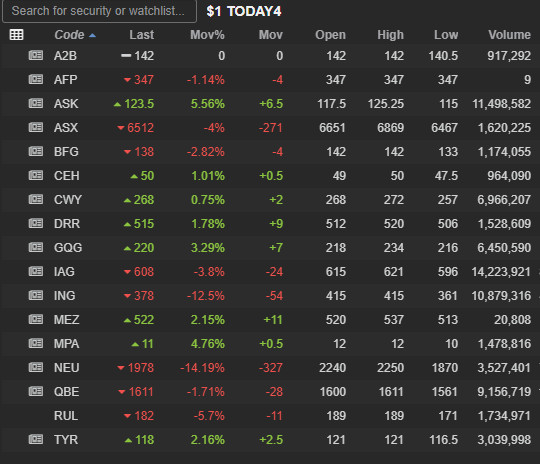

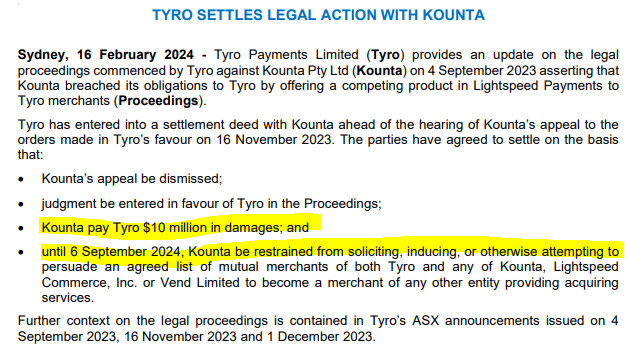

Tyro (ASX:TYR)

https://www.tyro.com/

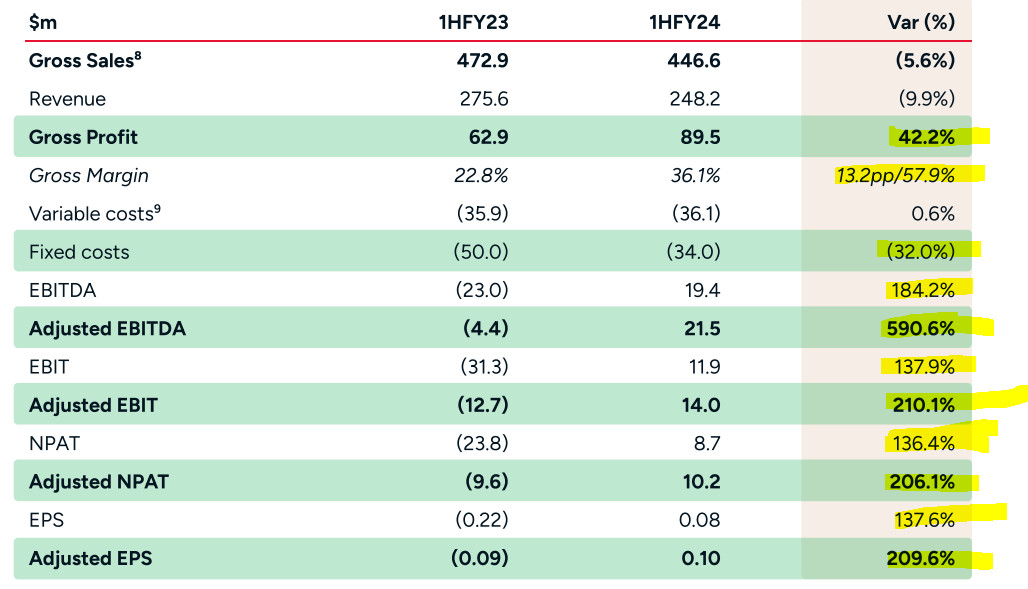

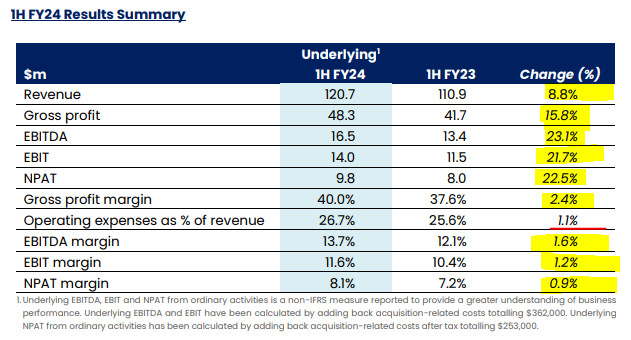

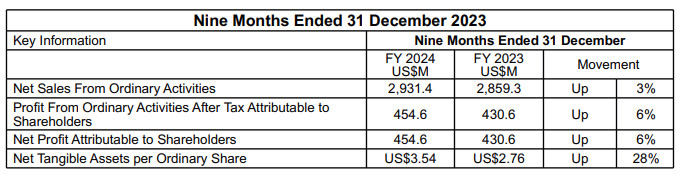

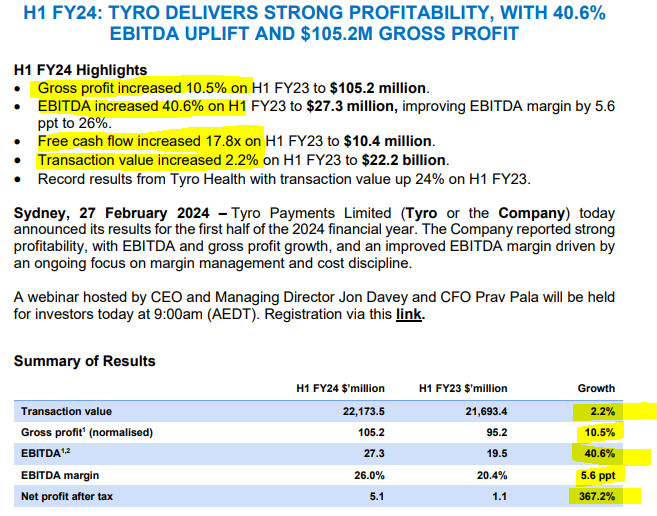

Ok first result I want to look at is Tyro (ASX:TYR). This company is interesting to me as I had some contact with them when I owned my small business. The point of sale system I used later offered an integration with Tyro. I though it was a clever way for them to gain market share. I know many businesses operating in the industry I was in (Health Foods) using the same POS (Point of sale ie cash register) as me took up the offer.

Recently though, that strategy has worked against Tyro. They had a similar partnership with a company called Lightspeed who’s POS is popular in the hospitality industry. Lightspeed decided they would offer their own payments and and clients that continued to use Tyro would be penalised. Tyro recently won a court case against the parent company of Lightspeed with a cease and desist order but I question if the compensation really covered the damage to the Tyro business. As for the cease and desist, from what I can tell, the damage was already done.

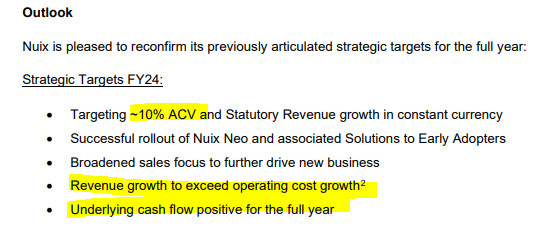

I don’t know if this result is good or bad but 2.2% growth in transactions doesn’t seem like much and I feel like the issue I outlined above could still be playing out negatively for ASX:TYR.

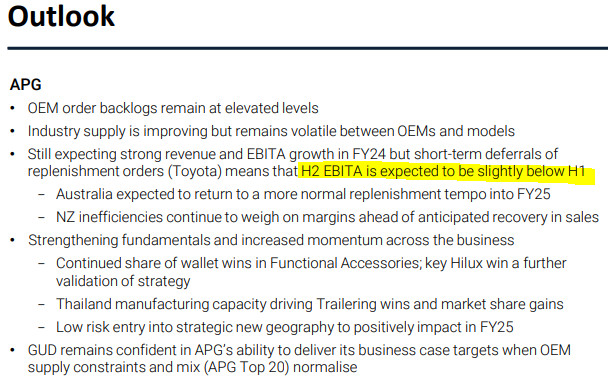

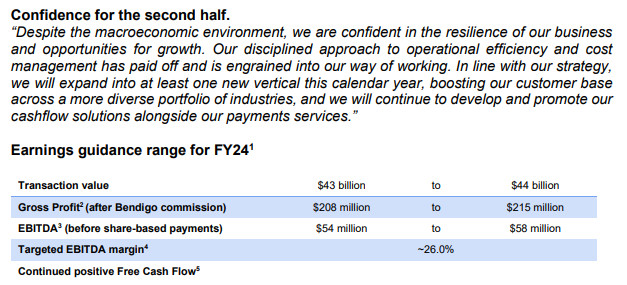

No growth at the top-line but importantly EBITDA is expected to continue to improve. The adjusting for share based payments really annoys me but that’s for another day.

ASX:TYR looks set to rise at the open from what I can see. I guess the market likes the improving EBITDA more than then lack of top-line growth.

Pacific Smiles (ASX:PSQ)

https://pacificsmilesgroup.com.au/

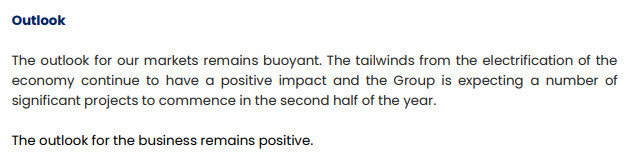

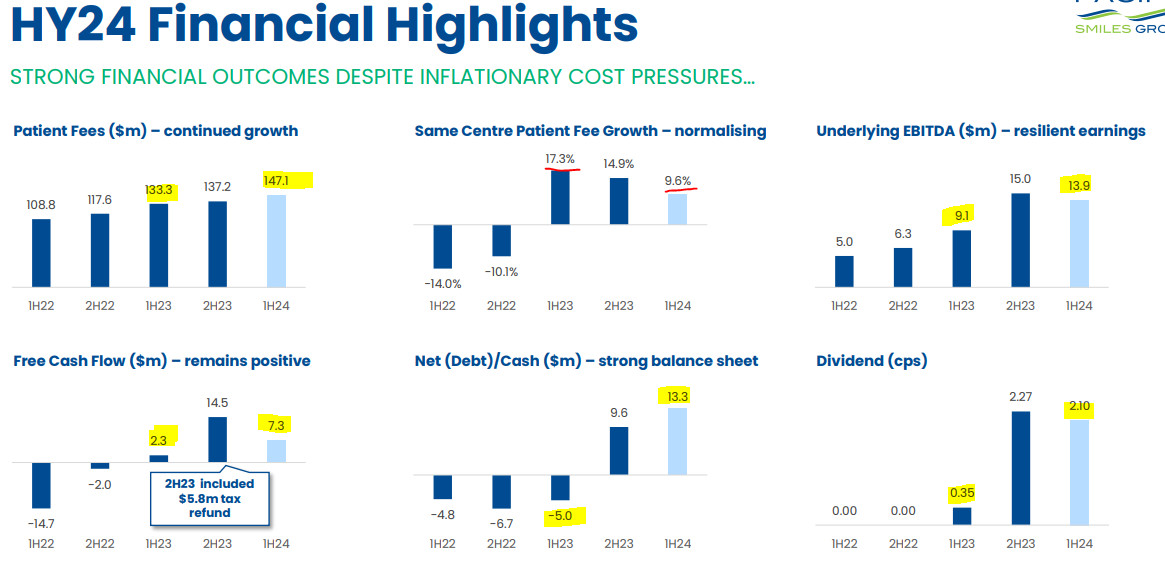

Next stock of interest to me is Pacific Smiles (ASX:PSQ). It’s a recovery story. Let’s see if they’re still improving.

Everything seems to be moving in the right direction albeit unspectacularly. They’ve also had some private equity sniffing around at the $1.40 level. Be interesting to see if this result can push them beyond that price and if it will get the PE to bite.

Outlook looks good, albeit roughly in line with what the market was expecting.

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Tue Feb 27, 2024: ASX:DGL, ASX:PNV, ASX:JLG, ASX:PSQ, ASX:PLY, ASX:TYR