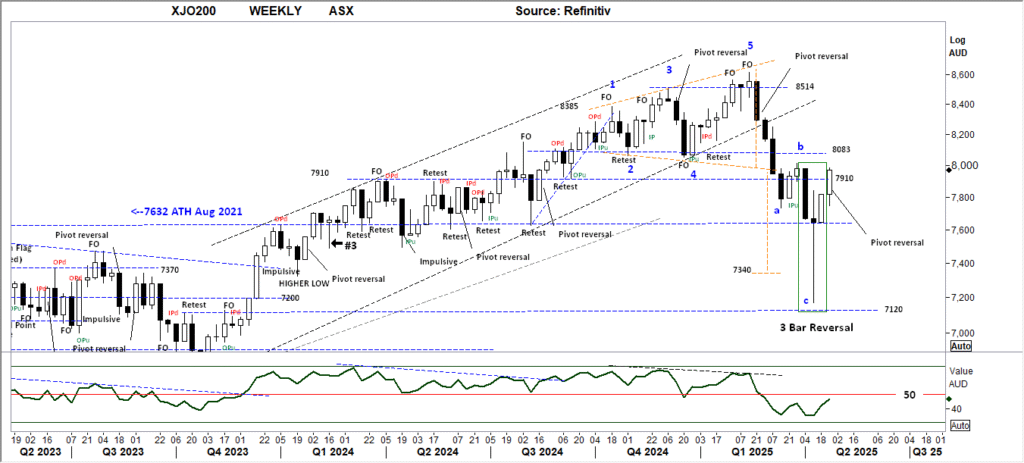

Current ASX Technical View – April 26, 2025

1. Big Picture Context

-

Rising Channel: The market was trending within a well-defined upward-sloping channel from Q4 2023 through late 2024, marked by higher highs and higher lows.

-

Completed 5-Wave Structure: There’s a labeled Elliott Wave 5 top at 8514, then a sharp breakdown — classic behavior once a 5-wave sequence matures.

-

Break of Structure: The channel was broken decisively downward — not a subtle leak, but a fast impulsive break. That’s a major bearish signal.

2. Current Pattern

-

ABC Correction: The chart now shows a pretty clean ABC corrective pattern:

-

adown -

bbounce (weak) -

cdown (sharp, into the 7340 low)

-

-

3 Bar Reversal: After the

cwave low, you have a 3 Bar Reversal formation — classic short-term bullish reversal pattern, especially off a major level like this.

3. Key Levels

-

Support:

-

7340: Big-time support.

-

7120: If 7340 breaks again, that becomes the next magnet (7120).

-

-

Resistance:

-

7910: Immediate cap.

-

8083: Major test above.

-

-

ATH Reference: Still far away at 7632 (Aug 2021 ATH) — now intermediate support if the rally continues.

4. Momentum (RSI below)

-

RSI is weak but attempting a bottom:

-

It dipped well below 50 and is trying to hook up.

-

The divergence isn’t massive, but there is a slight positive divergence compared to price — a small bullish tilt.

-

5. Theoretically, What Should Happen Next?

Based on the textbook setup:

-

After a 3 Bar Reversal post-ABC correction, you typically expect a multi-week bounce.

-

Targets: 7910 first, then 8083 — and if very strong, a retest of 8200-8300.

-

BUT the broader picture has shifted bearish:

-

The uptrend channel is broken.

-

8514 was a major blow-off top.

-

This bounce is a countertrend rally unless it reclaims the broken channel. That’s important — rallies into resistance should be treated with skepticism unless proven otherwise.

-

6. Realistic Scenarios

-

Scenario 1 (Most Likely for Now): Rally into 7910-8083 zone → stall → new wave of selling, possibly to retest 7340 or even threaten 7120.

-

Scenario 2 (Less Likely but Possible): A much stronger rally, breaking 8083, grinding higher, but this would need serious momentum and news catalysts (e.g., rate cuts, macro tailwinds).

7. Current ASX Technical View Summary:

✅ ABC correction complete

✅ 3-bar reversal signals tactical rally

✅ 7910-8083 major resistance

⚠️ Big-picture trend broken — rallies are guilty until proven otherwise

⚠️ Failure to reclaim 7910 convincingly risks a re-test of 7340, even 7120

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Current ASX Technical View