This would have to be one of the most upbeat earnings calls I’ve heard for a while and think it’s worth sharing.

If you use Google Chrome and have the “Read Aloud” extension, you can highlight the text and then select “Read Aloud” to have it read it to you.

Company Website

Operator

Good morning and welcome to the Ai-Media Technologies FY ’24 Results Webinar for the period ending 30 June 2024. Presenting today is Ai-Media’s CEO, Tony Abrahams; and CFO, John Bird.

Today’s format will have the team run through the results presentation, followed by a Q&A session. Investors are able to submit questions via the Q&A function at the bottom of the screen. I’ll now pass to Tony.

Anthony Abrahams

Thanks very much, Mel. Good morning and thank you very much for joining JB and myself on this Ai-Media FY ’24 results webinar.

I would like to acknowledge the traditional custodians of the lands on which we are joining here in North Sydney being the Cammeraygal people, and I pay my respects to their elders, past and present.

I co-founded Ai-Media 21 years ago this month, and I’ve never been more excited about the trajectory of the business than I am today. I’ve just got back from 4 months overseas, where I spent most of the time in North America and a couple of weeks in Europe.

It’s worth reflecting that for the first 18 years at Ai-Media, humans were required in every single product and a human in the loop was required to power every AI solution right up until 3 years ago. And by 2021, we had noticed that advances in AI had already seen 16% of U.S. broadcasts delivered with AI technology rather than services. And that was the moment at which we bought EEG.

We bought EEG because of the unique workflows that have enabled us to tailor AI-driven solutions for any customer workflow. The unique competitive advantage that the encoder suite and iCap network have provided us has been essential in driving the successful transition to technology from services.

Again, just 3 years ago, in 2021 when we acquired EEG, the entire company had USD 8 million in revenue. Today, 3 years later, we are reporting all the $32 million in technology revenue alone from North America, with the majority of that, 74% being technology sales at greater than an 80% gross margin. And we are only just at the beginning of the AI revolution in Language Services.

So, this has very much been an America-first strategy over the last few years and things are very much going according to plan.

Over the last 4 months, I’ve visited broadcast, government, and education customers in the U.S., Canada, U.K., Europe, and in particular, in Geneva, in Switzerland with the United Nations organizations. It’s fair to say that we have achieved product market fit over the last several years in areas beyond that of the traditional EEG business being North American broadcast.

When we acquired EEG, about 98% of the sales were coming from North American broadcasts. Now, while we’ve grown that pie and we’ve delivered $32 million in technology revenue from North America, we see an enormous opportunity to continue to grow and to continue that transformation, which has seen over the last 3 years, the company moved from $49 million in revenue and an EBITDA loss of $9 million.

So, that was in 2021 being in 2024, delivering $66.2 million in revenue and an EBITDA profit of $4 million. I’m proud that this growth has all been self-funded through operating cash flow. And indeed, a lot of the investments that we’ve made in products that have enabled us to continue to grow geographically into different sectors and into more AI-generated products than live captioning. I’m excited that almost all of that has been expensed.

So, we have a very clean balance sheet, and we continue to deliver improvements in products and improvements in sales efforts all through operating cash flow that are already delivering positive economic benefits.

Over the last few weeks, we achieved a very significant milestone, which was capturing of the Paris Olympics. We did that in Australia. We did that in the U.S. for NBCU. And we also did it for Telemundo in Spanish.

I’m delighted to report that for the very first time, we delivered this with LEXI in Australia and the mix of human services, and it was a full LEXI delivery in North America and in Spanish with Telemundo.

The result of that was exceptional. We had 0 complaints recorded for what was the greatest show on Earth. And in fact, that has delivered enormous confidence in us and in our customers that this technology transition will continue to accelerate. And in fact, what we have confidence on is that we will be at 80% technology revenue within the next 18 months, that is by December of 2025.

It’s worth pointing out that what we’ve reported today in terms of overall technology revenue is a view for the entire year. So, at 50% technology revenue split, we obviously finished the year at a much higher percentage. And because of the breakthrough difference that LEXI 3.0 has had and because of the continued improvement in the underlying AI technology, we have every confidence that, that acceleration into the technology space will continue. So, that 50% will be 80% within the next 18 months.

So, what does that mean? What it means is that we feel we’ve got organically the wherewithal to replicate the success that we’ve had with U.S. broadcast, to replicate those increases in the light blue graph that you can see there. And we’re intending to do that in 3 different directions.

The first is geographic. And so, while America has been first, Europe is definitely second. And a lot of the focus that we’ve got in FY ’25 is about replicating the success that we’ve had in U.S. broadcast in a market that’s relatively new to the EEG devices in terms of Europe, but one in which we have just covered off 50 new countries as being capable of working with EEG equipment and iCap.

The second area that we’re expanding is outside of broadcast into government and into enterprise, and there are some great product releases that we’ve got slated coming up that are going to attack that area.

And the final area of expansion is in terms of new products. While we’ve delivered well over 80% of our current revenue is live captioning, the opportunity to address a greater total addressable market is coming from our release of products that are in the broader AI language area.

So, aspirationally, what that means is over the next 5 years, organically, we feel based on the current trajectory, that we should continue to grow that top line at north of 30%, with EBITDA growing faster because of the transition to those higher-margin services.

And really, what that leaves us with is an organic line of sight to an aspirational target of $150 million in revenue with those 3 over the next 5 years and an EBITDA number of around $60 million. And that’s taking advantage of the geographic expansion, the sector expansion, and the product expansion and having conversations with customers who all want to know how they can embed AI in their workflow and realize the savings.

What’s important to note as well is that for every dollar of revenue that we are recording, where that is a substitution sale, many of our customers are saving $9 often with competitors in that legacy human business.

In summary, we are very much on track with our AI transformation, we are nearing the completion to a tech business. And over the course of the rest of this webinar, I’ll cover off quickly some highlights and operating updates. J.B. will provide some details on financials. I’ll then come back and give a view on the strategy and outlook. But I do want to take quite a bit of time after Q&A. So, as Mel has said, please do pop those questions in the chat panel.

In terms of our financial highlights, total revenue is up 7% to $66.2 million, and that’s notwithstanding a $4.5 million decline in the legacy services business. Gross margin is up to 64%, driven by that tech gross margin of 85%.

That tech revenue is up 37%, set gross profit up 39% and the cash balance is holding up, notwithstanding the payments of $8 million for the final EEG payments. And operating cash flow held up well, notwithstanding the fact that we made a concerted effort to invest additionally in inventory off the back of the release of, in particular, our new LEXI DR product that allows for local delivery of previously services that could only be accessed through the cloud.

That requires a very expensive build with NVIDIA chips and so on. We’re not expecting that inventory number to go any higher. That’s really a one-off reset.

What’s worth spending a little time on is this EEG infrastructure and ecosystem and why this gives us a unique opportunity to leverage all of the benefits on the improvements in AI right across the language services market, not just in live captioning because of the unique position of the EEG encoders in line in customer workflows.

So, if you look at #2, the encrypted encoding, the Falcon, Alta, and encoder products receive a direct input from customers’ audiovisual output. That is then directed to a real-time captioning engine via the proprietary iCap network that we have successfully monetized for the first time this year and across which all of the LEXI toolkit products are delivered.

This then gets embedded back into the captioned video output, all seamlessly automated for customers and embedded in their particular workflows.

Before acquiring EEG, we did not have the benefit of having a piece of equipment embedded within a customer workflow. And of the errors that we saw in terms of lost minutes of captioning, 100x more errors were caused by workflow issues than actually caused by the core technology. And that is why a workflow solution that is fully automated and embedded within a customer’s existing workflow is such a valuable proposition for our customers.

These products work. They have been used in U.S. broadcasts to pass through not just the captions but the audio and the visual content since 1980. That is probably the first and most important metric and why we have almost 0 churns on our technology customers once the encoders are installed. Because to pull those encoded out of line of the broadcast chain is to interfere with a system that gets the signal on air.

The second element is the iCap network. I mentioned that we began tolling that network for the first time this year, and we’ve managed to increase the resiliency of that network from 99.8% to 99.99% in the last 3 years.

But, of course, all the special source is really in LEXI and the continued AI advances. That’s for the very first time with LEXI 3.0 has seen the quality of the AI-generated captions exceed that of the humans for the first time in live captioning.

We’re seeing that advantage continue to extend, and we’re seeing that advantage also in the recorded space, which is giving us the opportunity to address a greater market size.

This is some new information on this slide, which I did want to share. So, as I said, it’s been very much an America-first strategy this year to tackle the largest market in the world where we have absolutely undeniable product market fit and in particular, with those logos in the Americas.

AWS is worth calling out. We have become a critical partner for Amazon in the delivery of captioning services for their broadcast playout system. They’ve been very public and open about that partnership.

And in fact, at the upcoming IBC conference in Amsterdam in the next couple of weeks where we will be launching our first non-captioning AI products through the LEXI toolkit, being LEXI Audio description and LEXI Voice. We will actually have a co-branded presence on the AWS stand at IBC as well.

Similarly, Google, we are deepening and extending that relationship while Disney, ESPN, Warner, Fox, the NBA, and Paramount are all looking at significant increases in the technology commitment to Ai-Media, including looking at purchasing more of that AI tool kit as we roll those products out.

You can see from the EMEA slide that, that’s a less populated slide at the moment. And as I mentioned, that is a key focus for FY ’25. We legalized the encoders for much of Europe just this year. That was a multiyear effort in terms of the development, but we are now fully operational in 50 additional countries, which is also helping us in the APAC region.

One thing to call out is that in terms of the core segment, 62% of our current revenue is broadcast with 34% being enterprise. As I mentioned, we see a huge opportunity to grow both the enterprise and especially the government line. And that’s certainly also going to be a key focus in FY ’25 and beyond, as we stretch towards that aspirational target of $150 million in revenue and $60 million EBITDA in 5 years.

This is probably the key slide that gives me the greatest degree of confidence that the journey we’re on is the right one, the strategy that we’ve got is the right one and that we’re executing in the right way.

That America first strategy is really proving out in the largest market that we’ve got. Those donuts are not to scale, by the way. So, on where the scale it would look even better but fully 74% of the $43.3 million that was sold into North America was delivered with technology.

When you look at then our aspirational target of achieving 80% by December of 2025, and you realize that all our focus has initially been on converting this U.S. market first. That’s why we have that degree of confidence that we will be there by then.

You can also see that APAC is still very heavily in the services bucket. That’s very much weighted towards Channel 9, Channel 7, and Foxtel legacy contracts. As I mentioned at the outset following the Olympics, we really got the green light to accelerate that transformation. And J.B. can give a bit more color on that as well.

In terms of EMEA, again, with Europe being the focus there, we have sold our first in codes to Europe in the second half of FY ’24, and the pipeline is looking extremely strong for FY ’25.

So, with that, I will just tack over to the operational update, which shows the continued growth in the iCap network and the even faster growth in LEXI.

What I wanted to highlight in and I won’t go through all of this in detail, but just to highlight that there were some very, very significant product milestones that we achieved in FY ’24 based on investments in product and engineering that have been expensed, not capitalized. Only $300,000 of that $7.5 million was capitalized.

And, as I said, we can now deliver the encoders and the EEG kit to over 50 more countries than we could 12 months ago, and we have implemented a LEXI local device for our government customers to ensure that no data ever leaves the customer’s firewall.

In terms of the iCap network in cloud, we successfully monetized to deliver $1.6 million annual in revenue, funding the improvements in resilience and uptime to 99.99%. And then massive improvements in LEXI underpinned by underlying improvements in AI and generative AI topic models.

We’ve also added considerably to the LEXI toolkit with that LEXI DR box, which I mentioned, was responsible for a lot of the increase in inventory. And our LEXI DR box allows our customers to finally turn off all elements of human workflow, including for disaster recovery.

And excitingly, LEXI Recorded, which was launched in March 2024, which is already delivering better results in terms of quality than LEXI Live is because the AI has the ability to watch the entire program before making an assessment.

So, that’s a little bit of color as to what we’ve invested in, and the operational highlights can demonstrate that we’re already seeing benefits from that. So, our hardware revenue grew 40%. We’ve continued to add languages other than English.

We have delivered massive improvements in stability and uptime in terms of iCap. And, of course, our LEXI revenue continues to lead the growth of our technology revenue.

And finally, in terms of services transition, that continues successfully. We have released some OpEx and some cost of sales through some head count reductions. And, as I said, we’re expecting that process to continue and accelerate through the end of calendar 2025.

I just wanted to provide a bit of an example before handing to JB on just a couple of case studies here. So, this really looks at this almost a point of inflection between FY ’23 and FY ’24 with the difference being that LEXI quality, overtook the quality of human in that point. And these are 3 of our target customers who are already spending high 6 figures, all of whom have increased their spend based on the success of LEXI and the importance of those encoders to deliver LEXI.

The case study 3 being a Fortune 500-company is particularly interesting. This is a customer who is a recent seller of ours. That’s our way to accelerate sales in a lot of the territories that we’re operating in.

That reseller has stopped offering human casting to their customers off the back of the success of LEXI and they have completely flipped that delivery for their customers. And as a result, spending 75% more with us this year than they were last year. So, anecdotal, but still some very exciting case studies of very important customers for us.

And I’ll now hand to JB to run through the financials.

John Bird

Yes. Thanks, Tony. And I’d like to thank all of you for your attendance because I think this is a pretty exciting time. Tony has already set the tone on some of the numbers. And I apologize in advance, I’m going to reiterate some of these because it’s very important in the messaging.

Firstly, I have to say numbers, guys. I think this is an absolutely fantastic result and one that I’m particularly proud of. I joined Ai-Media just after the IPO. And as Tony mentioned, the results for 2021 were probably disappointing.

We had revenue of less than $50 million. EBITDA was negative, and I repeat, negative $9 million. That’s a $15 million turnaround on the EBITDA alone. So, we since focused in the technology opportunity, and we’ve achieved since then 11% compound annual growth in our revenue and the $4 million plus in EBITDA.

Even a couple of years ago, it was only $1 million EBITDA. So, I was pretty proud of that. So, you can imagine I am ecstatic with the performance that we’ve got. But this is not simply numbers. This has been an achievement that was driven by a great team from the Board through the executives to all of the players in the organization.

Integrating EEG was a tough task, but I think we’ve achieved success. And the transition of the revenue to technology is testimony to that success.

We no longer are a service business. I believe we truly are a technology business. And when you start to unbundle what we call revenue and transition or hybrid revenue, this is fast moving to technology.

I think Channel 7, Channel 9, Sky, they all have the hardware in place. They’ve all adopted LEXI, and now it’s a matter of getting all of their programming across into LEXI. And we’re seeing some of that is resulting in the people being let go, as we mentioned, and I’ll talk about that a little bit further.

So, in effect, we’ve crossed the Rubicon and the tech-delivered revenue is now well in excess of 50%. Early indications are that it will drive way past the 60% quickly, particularly when we pivot these big companies across.

And this continues to drive the increased gross margin, which, as Tony mentioned, is now sitting at 64%, up yet again from last year at 60%, which was up on the prior year. So, this technology is really driving this gross margin, and we’ve always represented that the technology products run between 80% and 90% margin.

And, of course, one of the key things that everybody does want to know is that you’re also keeping a focus on your expenses. And we have elected to grow the business through the development of sales, marketing, and product. We’ve driven head count improvements. We’ve reduced the number of staff just in the last year by 20%.

Interestingly, while still building the head count in sales so you can see that we’re actually cutting the right areas and building sales and product resources. I consider it an amazing outcome that we’ve grown the business while we transitioned the revenue from services to tech in the whole while increasing the margin and focusing on what I think is a key driver in this business, that 20 number of EBITDA. Turn on the next slide.

I just thought it was relevant to actually extract some of the high-level numbers because it’s still very easy for us as we did say in February, we expected that we would see sales expenditure increase. And so, we’ve sort of detailed that a little bit more so people can understand that it is increasing.

We don’t expect expenses to grow substantially as they have in the last year. That was a concerted effort and investment. We’re investing in the future. And it’s a focus on all sales channels. Yes, some of this was staff, it was support staff in sales, it was technical salespeople, and it’s also building those other means of sales, the integrators, the value-added resellers.

If we isolate sales and marketing expenses, our growth has been increasing, particularly in the people, but also trade shows. One of the strengths of the trade shows is the sales team arranging formal meetings with would-be customers to the tune of NAB, the biggest broadcast show in the world, 200 meetings were arranged.

We’ve got another show the IBC at Amsterdam in a couple of weeks, and we’re already past 100 meetings. These are customers who we know will be on our customer list. They are the 2 world’s biggest broadcast conventions. And when I talk about customers, these trade shows made them aware of LEXI.

15 months ago, LEXI was a word. It’s now a product and we’re developing it extensively. And we’ve got introductions of these to AFL, the American Football League, Amazon, Google, Netflix. This is where they came. This is where they saw us. So, the spend there attracts the big broadcasters of the world. That’s where we got Telemundo, and others. They have first interest there. So, it’s very valuable.

And, of course, the other material area is product. As Tony mentioned, in the product arena, we spent in excess of $7.5 million, and we only capitalized 300,000 in the last year. And this is conservative.

One of the drivers for being so conservative is product must be aligned to sales activity. It must be seen to draw revenue in the near to medium term into the sales. We forecast to spend another $8 million in the coming year. And I know that Tony will talk about this in the next evolution, there will be products that will augment the experience of people desiring enhanced interactions, dubbing audio descriptions are recouped.

While these areas of spend are a necessary part of growing the business, the investment in both sales and product are paying for themselves very quickly. Next slide, Tony.

I always feel that I’m sounding old school when I say this, but I was brought up on a diet of cash is king and I don’t scribe simply to spending money unless there is a readily identified full benefit. The $8.1 million that we spent in the first column, finalizes all payments for the acquisitions that we’ve done over the past years. Effectively, all the cash we generate from now on is for us, for us to invest as to deliver.

Our operating cash flow, $3.6 million is somewhat in line with EBITDA, but also reflects our investment in the future. Inventory, as Tony mentioned, has grown. One of the reasons for that is we wanted to service our pipeline in sales faster.

We want to be responsive to our customers, and so, we did make a conscious decision to build the inventory. I think it will stabilize at probably about 20% less than where it is.

We had an early ramp-up. The NVIDIA ships on the disaster recovery box do not come cheap. But effectively, I think we’ll actually see a decline over time in inventory as we move to outsource some of our higher-volume products.

With a clean balance sheet, no debt, $11 million in cash. I think we’re in a pretty good position. I guess if I was to say a great position. So, I’d like to leave you with just some interesting take outs. EBITDA has gone from minus $9 million to $4 million, that’s $15 million turnaround. So, when Tony talks about aspirational targets, we do have some runs on the board.

I believe we are now truly a technology company. The services business is ancillary. It’s a necessary part of the business. It gives the customers the satisfaction of knowing we can do what they need, but the technology is the future. Ai-Media is a technology company generating cash. It has a clean balance sheet with almost $11 million in cash.

And, one of the interesting things, our share price in the last 12 months has risen 50%. I think we’re extremely well placed for the future. I expect the share price will reflect that in time. I thank you for your support, and thank you, Tony.

Anthony Abrahams

Thanks, JB, and huge thanks to you for your leadership of the finance function over the last 4 years. This is the fourth set of results that we’ve prepared together. And I think 4 years ago, we would have been very happy to look forward and see this. A lot of the hard work has been done and a lot of those expenditures are behind us for what we can tackle in the years ahead.

So, looking forward, then what do we see as being particularly exciting? Look, really, it is this opportunity that this unique position embedded within our customers’ workflows give us to expand the number of services, AI-powered services that our customers are hungry for. Now, if you look at that language services market, that language services market is a 2023 view, which means it’s got human costs embedded into it.

So, when you actually try and pull that down to actually look at what an AI price is, then you’re going to discount that a little bit, but you’re still going to end up with multiple billions of dollars in terms of the language services market to give you some comfort as to that $150 million, the reasonableness, I should say, of tackling that $150 million.

So, really, the bottom piece of the pie, the $1.8 billion, that’s the area that we’re currently servicing with the sort of 85% of our business that delivers live. It’s a multiple on top of that where you talk about recorded. And that’s why growing our LEXI recorded business and launching it this year has been so significant.

But attacking the $69 billion market, that’s moving into the other AI products like audio description, like voice, like translation. And we are seeing very, very encouraging results in our LEXI Lab on all of those elements. We won’t be doing this in a flow fashion, we will be launching new AI products at the pace at which the underlying technology is allowing for that, which is incredibly quickly.

The trick for us is actually in productizing emerging technology. There is no technology gap that we have identified. We’ve looked at a number of acquisitions this year and passed on them all because it was simpler and easier for us to just embed that technology within that existing team that we’ve got that team that we’re spending $7.5 million a year on.

So, in terms of the growth priorities for this particular year, it is encoded everywhere. It’s targeting the new territories, the 50 new countries where we have product market fit. It’s expanding into those new industries of government and of enterprise.

It’s growing those channel partnerships like case study 3, it’s improving the scalability and resilience of the overall network and it’s leveraging the new LEXI toolkit releases to help drive more encoder sales.

So, it might not be necessarily that it’s the existing product that we’ve got that’s going to drive future encoder sales and that’s something where we’re looking at. How many more SKUs that encoded could we develop to allow us to gain that critical entry point into customer workflows in different settings, and that’s certainly an area of great interest to our R&D team.

Growing the iCap network, putting that iCap network in more countries and more industries, growing that LEXI toolkit. So, I said that the LEXI DR products and LEXI Recorded products were only launched in the fourth quarter of last year, and we are launching next month, LEXI Audio description and LEXI Live voice stubbing, which again gives us the very first opportunity to tackle that much larger market size.

And then the services transition, we will continue to right-size that business to move it from being kind of the core operating model to, as JB alluded to, more of a wrap-up around which we can provide a total level of service and comfort to our customers.

What we’re also looking to do in our growth markets is certainly not to add further services overhead, but to look to partner with those third-party organizations who are now customers of AI on the iCap network to deliver that services record.

So, it’s very much a case of dealing with our legacy customers in a very essential way to wrap up that end-to-end service in terms of where we see that technology revenue kind of getting to that 80%, while 20% we’ll keep as that kind of services wrap up. In terms of our product launches, I would encourage everyone to follow us on LinkedIn.

If you’re not doing already, there’s a lot more that we disclose on LinkedIn than we can on the ASX platform. Some really exciting product releases, the 2 I’ve spoken about at IBC, generative AI topic models coming a month later.

We are adding sound effects recognition into LEXI in November, which we think is going to certainly massively improve the capability of Lexi recorded because that’s a key thing that at the moment, humans can do that the AI can’t.

We’re expecting further improvements in latency or speed in January and a brand-new translation module as well, which is going to power that translation. And then final slide and then I hand over for questions. Really, if you look at where we’ve delivered the bulk of the success to date, it’s really been in the top left corner. It’s really just been broadcast and America’s.

We will continue to focus on that sector, and we are expecting that the growth in that sector can sustain itself for several years. And then we’re looking to expand that into EMEA and APAC with a particular focus on U.K. and Europe at the moment, while developing trusted networks of resellers in those important countries in Asia.

As I mentioned before, a key part of the product development cycle last year has been building out the LEXI Local product for use in government. And we’re working very aggressively within the product team to find exactly what the product market fit looks like 4 various encoder types within the government sector in both the U.S., Australia, and the U.K.

In the U.K., what we’re also looking to do is leverage the relationships that we’ve got with the U.K. parliament into what’s largely an untapped European market and similarly to do that in Australia with our New South Wales and Victorian Parliament wins and breaking out into other areas of government as well.

Remembering, of course, that government is only 4% of our current revenue, and we think it could well be 1/3. So, there’s a lot of opportunity there. And then finally, in terms of enterprise, Ai-Media traditionally, certainly when we listed 60% of our business was actually enterprise, and it’s still 34%.

A lot of that has been a little slower to transition, but we’ve got our brand-new product releases, delivering LEXI into our world-class AI live viewer and looking at really delivering an always-on, always available service into universities and corporates, is a key area of focus again in terms of organic growth.

So, it’s really focusing on growing out those 9 sectors and opportunities. The roughly speaking, they’re probably all of equal size in terms of TAM and keeping in mind that really, it’s only in the top left corner where we’ve kind of got any sizable market presence at the moment that gives us the confidence that, that aspirational target of $150 million revenue and $60 million in EBITDA in the next 5 years is achievable.

So, now with that, I might hand over to you to curate the Q&A.

Operator

Thanks, Tony. Just on the growth initiatives. One of our questions relates to how you’re tracking with unlocking opportunity. At the last earnings call, you mentioned that one of the things keeping you up is how sales are attacking new markets and new opportunities.

Can you update us on the progress of that and how you evaluate or rank the success relative to your expectations?

And the second part of that question is, how well did you do accelerate into new opportunities? And how well have you carved out the right ready to kick through?

Anthony Abrahams

Yes, great question. Look, short answer, it’s still what keeps me awake at night is, are we covering off enough of the opportunities? And so, the dominant question that the executive team go through every week is how can we go faster? And where are we seeing opportunity? And we’re looking at that opportunity right across the board.

So, in terms of areas where we already have strong market presence, strong brand recognition, hiring additional internal salespeople into the sales teams has been very successful.

Those salespeople have an annual target of USD 1.2 million in sales. They get a 7% flat commission structure, and many of them achieved 2 to 3x their target last year. So, learning from that rinsing and repeating and then extending that into the government space, we’ve done. So, we’re just in the process of standing up a dedicated government sales team in the U.S. with the presence as well in EMEA and in APAC.

And so, they’re a brand-new internal team that are being stood up at the start of FY ’25. But really importantly, we’ve got our partnerships with people like AWS with the zone with Vivero that are helping us to really maximize the delivery of LEXI through effectively resellers and systems integrators, which has also been really important.

And then finally, it’s going through nominated agents in countries like Korea and the Philippines to kind of help us get through some of the local knowledge. And it’s working out what’s the right model for what type of the expansion strategy and keeping a close eye on it.

How do we track success? It’s pretty simple. It starts with pipeline. And then that pipeline converts to sales. I mean we’ve been saying for, I think, 3 years, every result that our pipeline continues to expand. Well, it does.

And also, that pipeline continues to track through the closed one deal. And those closed one deals then tend to be incredibly sticky. I’m actually not aware of a single customer that has churned in the last 2 years from our technology products. And I don’t know if any other similar company that could boost that level of statistics.

Have we had churn from our legacy services business? Absolutely. Some of it churns to us and then some of it will churn away. But of the business that we are winning with our AI LEXI toolkit, 0 churn that I’m aware of over the last couple of years. JB, did you have anything that you wanted to add on that on the sales acceleration front?

John Bird

No, Tony, I think you covered it. I do think it’s a highlight that we don’t have churn in the technology sales. Tony, I think that’s something that we service the customers well, but we love the product, they love the product.

And I think, once again, very important is, it becomes part of their DNA. It’s in their workflow. So, they don’t sort of go, well, I’m going to change horses because they’re with us. We’re solving a big problem for them.

Operator

The next question from Michael is, the media proxy partnership shows the potential of integrating your technology into other hardware. Are you considering similar collaborations with other AV equipment providers? If so, what factors would make these partnerships most viable?

Anthony Abrahams

Great question, Michael. Thank you. Look, as I said, the strategy is encoded everywhere and as JB said, we’re absolutely not tied to manufacturing our own equipment. So, an ability for us to install and deliver iCap functionality on third-party equipment would be extremely interesting for us.

And the relevant test would be how much latent demand is there within that particular environment for services that can be delivered across iCap being the AI-powered LEXI toolkit. And then sort of how do you do the commercial deal? But, no, that would be something very interesting.

Operator

Thank you, Nick Harris has 3 questions. So, firstly, on Page 12 of your investor presentation, it’s 35% reduction in head count, resulting in significant reduction in OpEx. Can you please expand on this? Specifically, FY ’24 OpEx listed year-on-year. Did FY ’24 OpEx include any material redundancy costs? I might let you add to that first before I get to the next 2 questions.

Anthony Abrahams

Yes. So, I guess, again, this is 2 businesses, Nick. One is a growth business, which is the technology business, which is growing at 37%, 40%. We’ve invested more, and we’ve identified very clearly, we’ve invested more in sales and we’ve invested more in product.

What we’ve also done is we’ve released A lot of those are human in the loop operators, the coordinators, the supervisors and the team leaders that go in and around that. Some of that is cost of sales, but some of that is also OpEx. JB, I don’t know if there’s anything you wanted to add on that?

John Bird

Well, I’ll add on the second part, which is the redundancies. Yes, we did incur some redundancies. Fortunately, we’ve managed that very well. Deanne Weir runs operations. And I think the number is around 300,000, Nick.

And so, it’s not particularly material. But I think what we’ve done is we’ve transitioned some of those roles. It’s interesting. Some of the people have actually from an operations perspective, moved into sales support type roles, too. So, we’re managing it well.

The 35% is the head count in that services business. And we have had some overhead cost reductions, be it finance, be it people team. But generally, a lot of that is driven from the transition into our technology business.

And, Nick, you do ask whether we should see an uplift or a decline. I think we’ll see; we sort of addressed the graph on operating expenditure. We’ll still see operating expenditure increase, just the nature of people getting pay increases. But I don’t think we’ll see the same step-up function that we have had in maybe the last year or so.

Operator

And just in terms of the OpEx savings in FY ’25 from further head count reductions, Nick has also, can you please give us an idea of whether we should expect OpEx to drop in FY ’25 as a result of restructuring? Or are you likely to reinvest those savings into other areas to deliver revenue growth?

John Bird

Yes. Look, I think as I said, we’re not going to see an OpEx decline. We are spending money to grow the business. We just don’t think it will be as significant as it was in the current year. But we invested, as I think Tony mentioned, a number of people we’ve invested in sales.

The sales and marketing are probably our biggest growth area of spend, and that’s got a direct correlation to the sales activity. And even commissions have gone up. We did improve the commission rates on people who were selling to encourage more activity and its paid dividends.

So, I think we’ll see a sustained OpEx rather than seeing a step function in OpEx in ’25. Do you agree, Tony?

Anthony Abrahams

Absolutely. And I think as well, like what’s been really key for us and I know JB shares this passion as well is that our growth is sustainable and funded through operating cash flow.

One of the things that I think we’ve got a lot more confidence on this set of results that we probably even didn’t have 6 months ago, is that I’ve got a lot more confidence that there isn’t the requirement for a big capital raise coming forward to get to that target of $150 million revenue and $60 million EBITDA.

We’ve got a lot of that either in the bank or we’ve got the technologies readily available through partners to deliver what are going to be absolutely transformational experiences for our customers well beyond what you’re currently seeing from live captioning.

Live capturing is the tip of the iceberg. It’s literally 1% of the total market. We’ve delivered in spite on the most difficult market for that, which is U.S. broadcast and the largest market over the last 3 years, we’re just going to look to replicate that success in the other markets.

And, Nick, as the previous question said like, what’s my biggest concern? My biggest concern is that we’re not going fast enough. So, really, yes, we will look to reinvest whatever available cash we have into growth right now, given where the market is and given this explosive interest for AI products from the top end of town that we’re talking to.

Operator

And just further to that, we have had a question if you could confirm your EBITDA target mentioned?

Anthony Abrahams

Yes. Look, again, it’s an aspirational target but it’s based on the historical trends and the data that we can see and where we’re looking to go, and that’s very much within 5 years, organic growth based on those 3 directions of expansion being geographic, being sectors and being products to get to $150 million revenue and $60 million in EBITDA in 5 years.

Operator

With the move into non-English markets, does the software AI or AI also extend to translation software, i.e., English to Spanish?

Anthony Abrahams

That is a great question. And what’s really probably a data point that’s super interesting is that at the moment, 98% of all demand for live captioning is same language captioning. So, it’s English into English, French into French, Spanish into Spanish, Russian into Russian, Arabic into Arabic.

So, what we’re doing is we’re doing more and more of those same language transcriptions because that’s where the demand is. Of the 2% that we’re talking about that’s actually translation, there are some key customers that are really looking at this in a big way. And I’ve slated the January 2025 being our LEXI Translate 2.0 release, where we’re expecting a step change in that translation function that will hopefully do for the translation market, what LEXI Live 3.0 did when we released that in May of 2023, which is delivering a product that’s comparable to the humans.

At the moment, you can do that with a couple of language pairs. But again, the resiliency of that is probably a step further down the line, and that’s one of the product areas that we’ll add to that revenue and EBITDA boost over the 5 years ahead.

Operator

Joshua asks, this year, the company has been intending many trade shows. Can you give us a sense of the feedback from these shows? Also, do you see the trade shows as an area to sign on new customers or promote the business?

Anthony Abrahams

I’ve got to say I’ll invite JB to give his commentary on this as well. When we acquired EEG, Phil McLaughlin, who was the vendor said the only marketing spend he ever made was trade-shows. And at the time, we had a much broader mix of marketing activities, we were using different social media campaigns, ad words, et cetera, et cetera.

Phil was right. It’s literally the only thing that works in this business is trade show. Why? Because all the customers are there. They’re all there with a specific proposition in terms of what they’re looking for. And they all actually want to make sure that they’re buying a solution that is industry-consistent.

They don’t want to be a shag on a rock. They don’t want to be the 1 broadcaster in Europe that’s using a different standard that’s not going to be supported. Everyone wants to make sure that they’re going with the leading technology that has the best level of support. That’s why it’s been so critical that we get this first mover advantage with LEXI in U.S. broadcast because that was the place where we had existing product market fit.

That was the place where we had the greatest market penetration at the time, and it was the biggest market side. And so, that’s really been what we’ve been doing in the last few years. And so, back in the day, Phil McLachlan would only go to NAV, which was the big show in Las Vegas, and IBC, which is the one next week.

What we’ve been doing now is, we’ve been breaking into new areas, we’ve been going to new and different trade shows. For example, the National Religious Broadcasters Association that’s looking at all of the mega-churches in the U.S., we went to that event a couple of months ago and we had 62 meetings with 62 customers from religious organization.

And so, what we’re looking to do and so now I think we’ve got maybe 17 or 18 different trade shows around the world that we go to, but continuing to invest in those trade-shows is essential. And every single major deal that we have signed has happened through some trade-show contact, one way or another.

It’s definitely a means to move the ball forward. And it’s also an opportunity then to continue those conversations. I mean being over in the U.S. for the last 4 months, I probably met with our key customers each half a dozen times, while I was over there.

That’s been really essential because they’re talking about kind of 7-figure changes for their overall technology infrastructure, but they’re also asking for road map visibility. What are the product opportunities going to look like in 2026 and 2027?

Should I go on and renew my human services contract with somebody else for dubbing for the next 3 years? Well, the answer to that is, no. You should have a short-stated contract. So, these are the conversations that we’re having with customers to really help us set up.

But the visibility that the trade shows give us and the confidence that it gives our customers that not only are we real, not only can they see the products, not only can they demo the product, so then they touch the product, but they can also talk to their colleagues in the industry to get comfort that this solution is working for them as well as it’s working for that particular organization.

I think that’s part of the key dynamic. But JB., I know the NAB was the first trade show you went to, and I think you were very pleasantly surprised by how effective it was as well.

John Bird

But, Tony, it was embarrassing. I tried to turn the CFO into a salesman. Look, one of the things is you almost need to touch the product. We had a stand where we had, I think it was a 610 sitting there, and people could speak in any language they wanted, and it would literally bring it up on the screen. This was the launch of LEXI.

And I think people were not only pleasantly surprised, but they would drag colleagues, friends, and others. So, not being biased, but I think we had the booth that was the most overrun of the entire NAV show because everybody wanted to play with the new toy.

And, as I mentioned in what I said, this is where we met with Netflix. This is where we met with Disney. This is where the NFL, the basketball league, they all came in to touch to see. SO, it’s the place that we spend the money. As Tony said, Phil was right, and I think we will continue to do that.

Operator

Tony, all the upcoming product launches, which one are you expecting to have the greatest commercial impact?

Anthony Abrahams

We’ll really put me on the spot there, Michael. Look, I think in the short term, probably LEXI DR in terms of this year, I think, of all of them, and that’s because it’s a box that every customer really should take it’s $10,000, it’s going to be a one-off hit, if you like.

So, that’s probably in FY ’25, it’s going to have the biggest impact. I think in the sort of across FY ’20 I’d say over the next 3 years, it will be really interesting for me to see whether LEXI Recorded are captioning or whether the Lexi recorded audio description and dubbing takes off more.

I think they’ll all do really well. As to exactly the level of take up, we’re running a bit of an internal pool on which of these is going to kick fastest. But look, we’ll have more to update on that, I think, following the actual launch of these products in September. But look, early indications are very, very positive from customers on LEXI Recorded and LEXI Audio description and LEXI Voice and dubbing.

And we’re going to try and do it all. And we can do it with, as I said, with the product and technology that we’ve got, there’s no technology gap that we need to acquire from anyone to deliver these products. And that’s an important point.

So, in a sense, it doesn’t really matter which one of these kicks first or kicks hardest. Certainly, there is significant savings to accrue to our customers if they can switch off their human workflows on all of their products. And different customers are coming to us saying, each of those 3 are a higher priority for them. So, really, we want to be able to do it all. J.B., I don’t know if you’ve got any flavor on that?

John Bird

No, that’s cool.

Operator

Stella says, fantastic results. Please, can you comment on where the service gross margin percent will stabilize from here or temp gross margins will be higher than historical levels in the second half of this year. Is 85% level sustainable? Or could it possibly even improve further with new product launches?

Anthony Abrahams

J.B., do you want to grab that?

John Bird

Yes. I think, Stella, l I’m probably the most conservative person you should be not talking to. Look, I think we will continue to focus on the services margin. So, as a decline in revenue, we will continue to manage the cost. So, I don’t see it necessarily changing very much.

We took a very conscious step to lose clients where we had a very low gross margin in the services business. And so, I think it’s now at a sustainable level. On the technology, look, there’s always pressure on technology pricing. We’re pretty comfortable that in the recurring revenue, so the iCap revenue, the LEXI revenue, that we’ve got a good price point.

I think we’ll sustain it in that SaaS space. And hardware is variable. We do big deals. We will give a discount. If we have a value-added reseller who wants to do a big deal, we give a discount. That drops straight to the bottom line. But we’re talking a 5-point difference, 1 month versus the next.

But overall, it should still sustain itself somewhat similar to where it is, maybe a little bit more growth, where the overall margin will improve is the buyer will head further and further to technology. So, we’ll move further and further towards the overall gross margin being a technology-led gross margin.

Operator

Also from Stella, John, hats off to you on conservative capitalization of technology development expenses. With a strong product launch pipeline, should we expect to capitalize development cost increase from a fairly modest second-half run rate?

John Bird

I’d like to say no. There are accounting standards that we have to conform with and we do that, but we tend to be objectively conservative. So, if there’s something that we actually made a new product that was a distinguishable product, yes, we would probably capitalize some of it.

But I don’t see us going ramp and like some tech organizations where we’re capitalizing millions of dollars. The most I can see is somewhere around $0.5 million every year might be reasonable. But a lot of that development occurs in our New York office. And a lot of it is symbiotic.

These developers suddenly get together in the disaster recovery box, I wouldn’t say it came out of nowhere. Somebody made the mention, a customer made a mention, and it almost became a skunkworks where they built this thing. And then we went, gee, we’re going to refine that and turn it into a product.

So, it’s a bit like the old 3M, go out and think about what you can do to add value. Am I going to capitalize those costs? No. I think we’re a very adept organization. I think the development team knows where they want to head, and I think they work very well with sales. So, we just will continue to build things that sales can sell, and we’ll continue to take a conservative approach.

Anthony Abrahams

I think JB., that might be a good time to also just flesh out some of the questions we had off-line around why our depreciation and amortization expense is so high if we’ve been so conservative in terms of capitalizing development efforts?

John Bird

Look, sure, Tony, and I think there was a question about that, and I know Nick and a few others are interested. Our depreciation and amortization expense is pivotal around some of the non-asset categories, things like customer contracts, capitalized development costs, even some software development type costs.

What we’re going to see is, there was $4 million depreciation and amortization. That will decline probably by about $800,000 next year and a further $800,000 a year after. And as the pool of assets that we’re depreciating declines, the value or the net book value, as we’re not putting a lot more into it, it will continue to decline. If I was to say it will be less than $0.5 million in 3 or 4 years’ time. I think that’s probably not far from the truth.

So, we’re not incurring those acquisition-type capitalized costs, as I said, customer contracts. We spent some money in sorting out manufacturing, but none of it is particularly material. I think in the U.S., we spent the best part of $0.5 million buying pick-and-place machines, which are used for building boards, if you like.

None of this is particularly material. And we have a workforce that we don’t need big premises costs. And so, I can see that depreciation will continue to drop and just plateau out at some million dollars in years to come.

Operator

We have a few questions here on the aspirational target of $150 million sales and $60 million in EBITDA. One, is that weighted to the end of the period? Or will it build more gradually year-on-year? And then the second part of that question is, would those numbers imply lower margins, for example, sub-64%?

Anthony Abrahams

Okay. So, first question, no. Well, I mean, we’re expecting the growth to be consistent. And in fact, it’s the maintenance of that mid- to high 30s growth rate that gets you to that point.

In terms of margins, obviously, we’re allowing ourselves in terms of these forecasts, some flex in terms of discounting, in terms of pricing, particularly for large customers, as J.B. said, given that the majority of our sales accrued to sort of the top 50 customers that we’ve got, really looking to super service those customers and try to identify large customers in the growth sectors that we’re talking about that are not current customers.

The fact that we need to allow for the fact that fewer of those sales are going to come from direct engines and more of them are going to come from value-added resellers, systems integrators, and other people in the ecosystem like AWS, then you’ve got to allow for 20, 25 points for them.

The other thing to keep in mind is that it’s not really comparing apples with apples, because we’ve got a 7% sales commission that we pay to all of our internal sales team, but doesn’t come off margin for some bizarre reason, in terms of the accounting standards, right?

So that’s probably why we’re being a little more conservative on the gross margin number when we do get up to that $150 million mark. But very much, we’re talking about delivering in a steady state, delivering that steady pace of growth that we have been delivering continued through the next 5 years. So, not something that’s going to be back-ended at all.

Operator

When you take ad tech revenue in December ’25, do you expect services revenue to decline significantly from now?

Anthony Abrahams

It will decline to get to the 20%, correct, but then it should stabilize.

Operator

And then just going back to gross margin targets, Tony, over the next, say, 2 to 3 years, once tech becomes more of a portion of overall revenue, what would be your gross margin target?

Anthony Abrahams

Look, I mean, we’ve said north of 80%. We reported 85% for our tech gross margin. As I said, there’s a 7% commission that you kind of comes off that. The services margin has held pretty constant at about 44% at the moment. You can just use the math to work out what the blended margin would be based on an 80% cash margin at that point.

Operator

And Stella has asked, after you start filling the third-party caption provider in November 2023, have you seen much churn among the iCap customer base?

Anthony Abrahams

Great question, Stella. Thank you. I think that classifies as Dorothy Dixer. Of the 80 competitor agencies that reluctantly find up to paying us money, that represented 100% of the base, and we’ve had 0 churn.

John Bird

But, Tony, can I add to that? Because whilst the customers, those end customers haven’t churned, we’ve actually seen some of what would have been captured by these companies has actually moved to LEXI. So, whether it’s Fox or whether it’s somebody else, they’ve now got an awareness that they’re playing for human captioning on the iCap network, and they’re going, well, hang on, why don’t I move it to LEXI?

So, we are seeing almost a reverse thing happen, which is great for us and we still want to keep the human captioning paying the iCap, but we’re moving it to LEXI. So, that’s been a double positive.

Operator

In FY ’25, do you expect EBITDA margin expansion?

Anthony Abrahams

Yes.

Operator

Nice and short. I like it, Tony. Based on the growth trajectory, the company should start to project significant amounts of free cash in the coming years. Will the company use its cash for acquisitions, begin paying dividends or a mixture of both?

Anthony Abrahams

Yes. No, look, I think, yes, we will expect to produce more cash as the company grows. But equally, we are expecting to see a number of opportunities open up as more of the customer base and more of the industry more confidently move towards AI.

My bias at the moment will be to just keep our powder dry for the moment while we’re at this point of inflection, recognizing as well, obviously, that a buyback is also an option within that particular configuration, which a lot of shareholders have been in favor of in the past.

Look, that discussion is going to be one for the Board in a couple of years’ time. But certainly, we’ll take an assessment of the landscape at the time. And there could well be some interesting more material acquisitions that would add to the $150 million target in organic growth that could be an inorganic opportunity that could be a multiple of that.

So, we’re not saying that we’re not interested in M&A, what we’re saying is we don’t think we need it to deliver this particular trajectory for the next 5 years based on organic growth. But there are other potential opportunities that we could look at to provide inorganic growth opportunities above and beyond that.

Operator

And that’s a good segue, Tony, to our final question, which is if acquisitions are part of the growth strategy, what type of companies are potential targets?

Anthony Abrahams

Again, I’ll reiterate, it was a very similar question that we got, I guess, at the beginning, which is a useful way to sort of round back. The most interesting company — I mean, people picked me all the time product companies, and that’s not interesting mainly because we don’t have a product gap that we need to fill.

Why did we buy EEG? We bought EEG because of the installed base of the encoder network and the iCap network that effectively allowed us to be in the preeminent position to receive the input from the customer to give the best possible outcome through the AI engine.

And that’s effectively allowing us to capture 85% of the economic value of that in terms of delivering LEXI. So, an ideal scenario would be, okay, where is there an analogous situation, where is there the large installed base of hardware that may not have LEXI available on it, but for which LEXI could be useful? And that for me is probably the area of greatest interest in terms of M&A.

But I’ve seen anything that’s right and ready at this point, but something that does allow us in kind of one fell swoop to kind of install iCap and LEXI across a base of customers in a new territory or new industry, that’s probably the area that I’d be most interested in.

Operator

And that looks to be our last question for today. If anyone does have any other questions, feel free to e-mail me through, and we’ll come back to you. I’ll pass back to you for final comments. Tony?

Anthony Abrahams

Thanks very much, Mel, and thanks very much to everyone for attending. As Mel said, we are very happy to take further questions. We’ve got a pretty full schedule for the road show, but always happy to add in some extra meetings.

Thanks very much for listening to the story. We’re in a very exciting point where as an Australian-listed company, we are profitable, cash flow positive, and we are delivering AI technology benefits to top-tier customers right around the world. And the largest market in the world is the one that we’ve tackled first and one in, which is U.S. broadcast.

And from now, what we’re looking to do is to replicate the success of U.S. broadcast in other geographies, in other sectors, including government and enterprise and by driving more AI products through that funnel, which is ultimately driven by that unique point of presence within our customers’ workflows being the encoder devices connected via iCap.

So, we’ll continue to execute on that. Thank you very much to everyone for your support. I know it’s been a rocky-few-years in terms of the share price. But as JB said, hopefully, that worm has turned, and we’re starting to be supported on this journey of increasing the AI componentry within the entire language services market around the world. Thanks very much all.

Note: This is a live chart. The technical analysis in this report should be considered up to the date of this report.

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Ai-Media Technologies 2024 Earnings Call

After a huge fall, the company is trying to pick itself up off the floor. Sadly, they do require the current conflicts in the world to continue for their shareholders to prosper.

After a huge fall, the company is trying to pick itself up off the floor. Sadly, they do require the current conflicts in the world to continue for their shareholders to prosper.

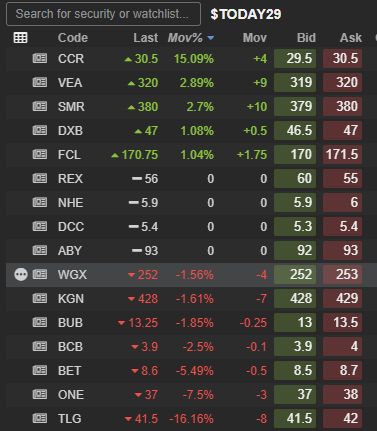

The Uranium trade was a good one for about 12 months. Not at the moment though.

The Uranium trade was a good one for about 12 months. Not at the moment though.

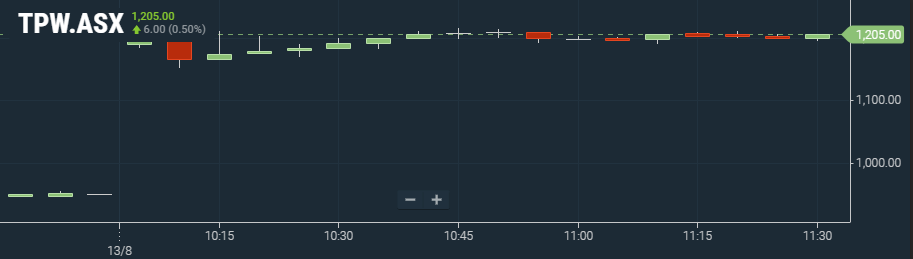

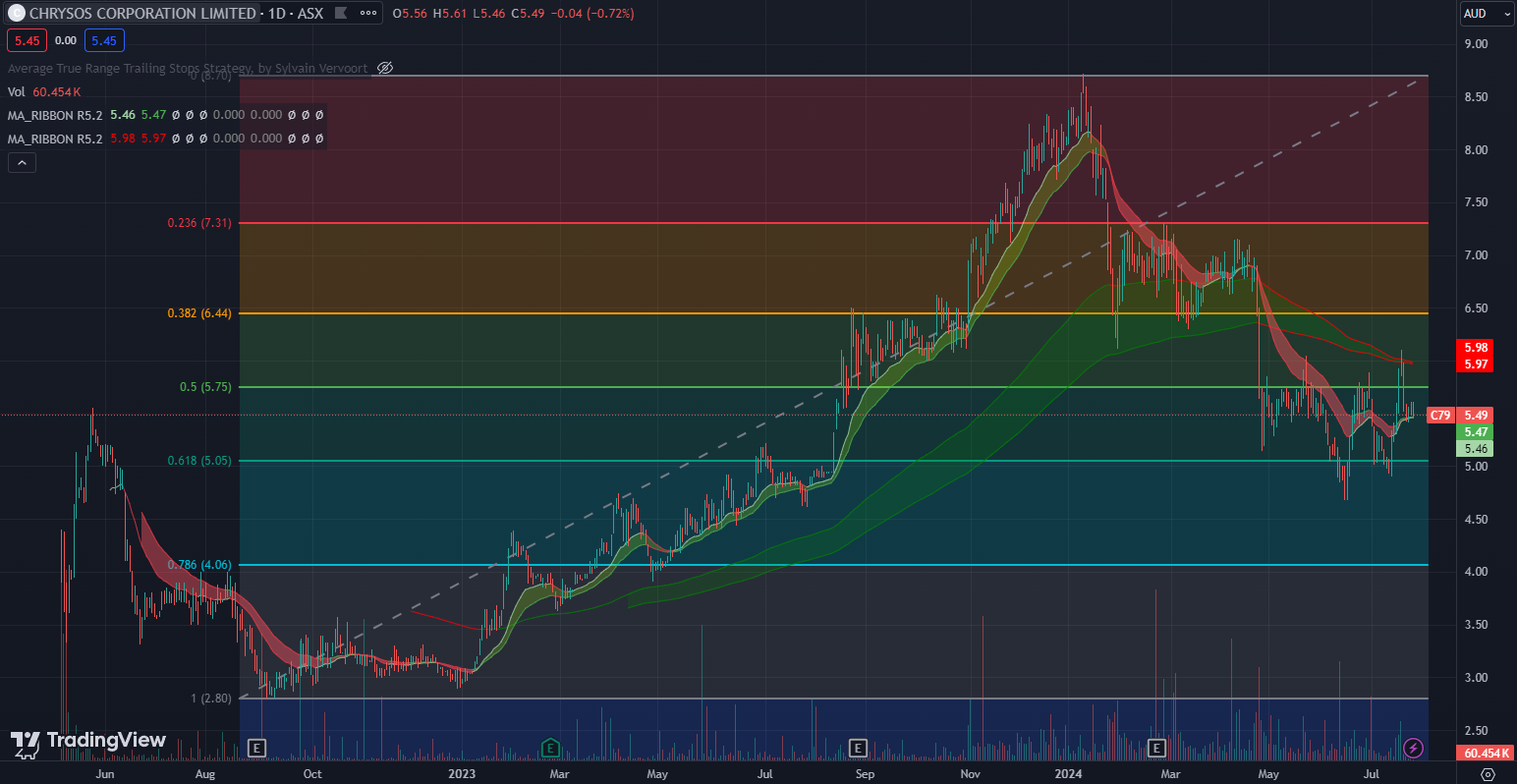

This is a typical chart of a company that is waiting to decide which way to trend again. Strong quarter with solid but unspectacular outlook. It may just not be enough considering the company is trading at over 20x revenues.

This is a typical chart of a company that is waiting to decide which way to trend again. Strong quarter with solid but unspectacular outlook. It may just not be enough considering the company is trading at over 20x revenues.

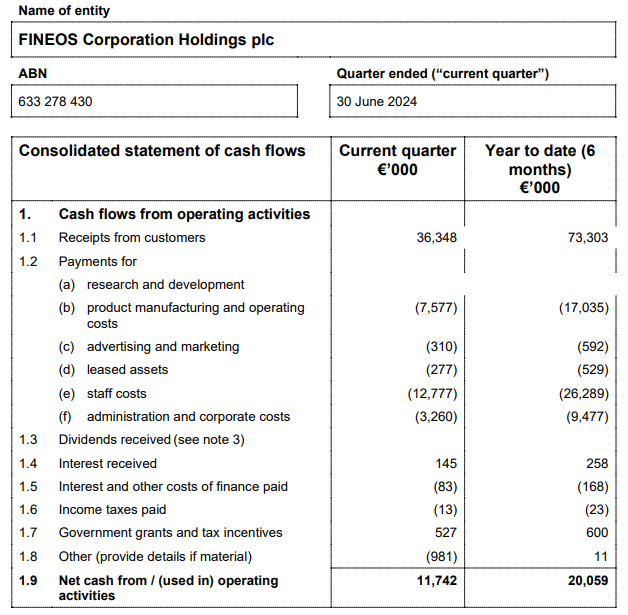

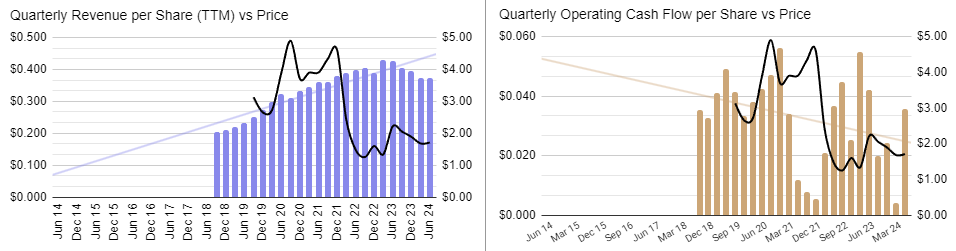

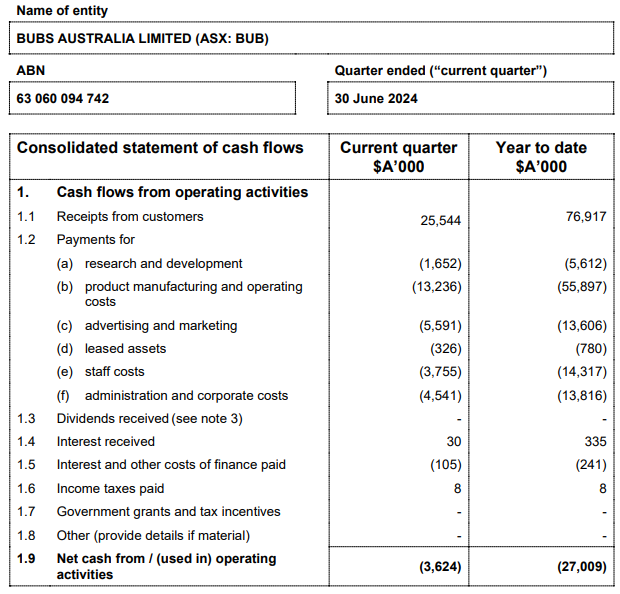

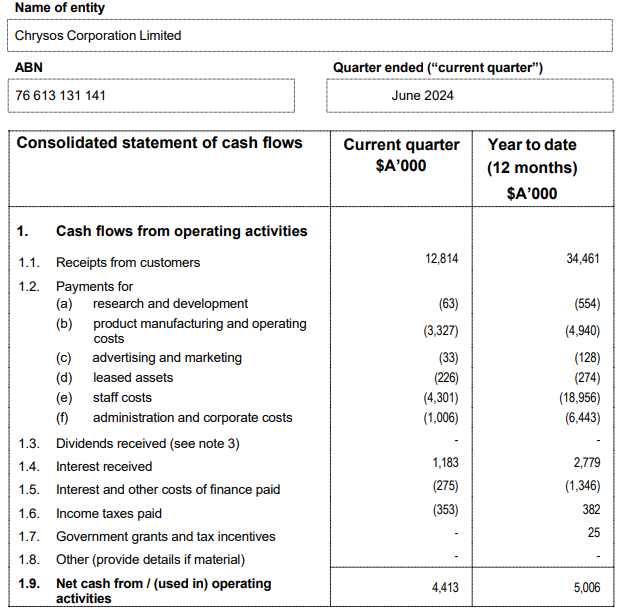

Ugly chart with nothing in that quarterly cash flow to encourage further investigation for me. Maybe next quarter.

Ugly chart with nothing in that quarterly cash flow to encourage further investigation for me. Maybe next quarter.

Sadly for anyone bullish on the silver price, this has been a poor way to play that theme. While Silver (in Australian Dollars) is up 30% in the last 3 years, this company is down 40%. In more recent times, the divergence has been even more glaring.

Sadly for anyone bullish on the silver price, this has been a poor way to play that theme. While Silver (in Australian Dollars) is up 30% in the last 3 years, this company is down 40%. In more recent times, the divergence has been even more glaring.