AVITA Medical – 2024 Full-Year Results Summary

Website: AVITA Medical

Overall Tone

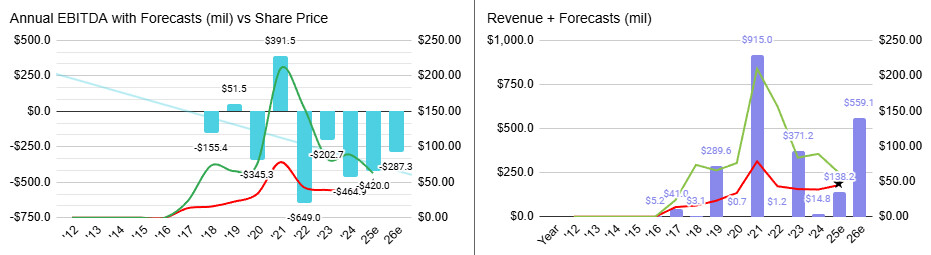

AVITA Medical delivered strong revenue growth in FY24, reflecting increased adoption of RECELL® technology across multiple treatment areas. While the company reported a larger net loss, key strategic milestones, expanded market approvals, and a revised financial outlook remain positives. The company’s ability to sustain its momentum in regenerative medicine positions it well for future growth.

Financial Results Summary

| Metric | FY 2024 | FY 2023 | YoY Change |

|---|---|---|---|

| Revenue from Ordinary Activities ($M) | $64.3M | $50.1M | +28% |

| Other Income ($M) | $0.16M | $9.91M | -98% |

| Statutory Net Loss ($M) | $(61.8)M | $(35.4)M | -75% |

| Total Comprehensive Loss ($M) | $(61.9)M | $(44.9)M | -38% |

| Net Operating Cash Flow ($M) | $(48.9)M | $(38.0)M | -28.7% |

| Net Tangible Asset Backing per Share ($) | $(0.17) | $1.82 | N/A |

| Dividend | N/A | N/A | No dividend declared |

Positive Surprises & Potential Concerns

- Positive: Robust revenue growth (+28%), driven by broader clinical adoption and expanded market penetration.

- Positive: Regulatory advancements, particularly in full-thickness skin defects and vitiligo indications.

- Positive: Strengthened financial position, securing amendments to its credit agreement that provide more flexibility for future growth.

- Concern: Net loss widened, primarily due to higher R&D and commercialization expenses as AVITA scales operations.

- Concern: Liquidity and cash burn remain areas to watch, though the company asserts it has sufficient funding for the next 12 months.

Outlook Commentary

- Continued revenue growth expected, fueled by broader U.S. and international adoption of RECELL®.

- Regulatory progress in new indications (vitiligo, trauma, chronic wounds) expected to unlock additional revenue streams.

- Operational efficiencies and pricing strategies to improve gross margins over time.

Guidance Statements

- Revenue: Expected to exceed $73M in Q1 2025, with sequential growth through the year.

- Cash Management: Continued focus on reducing burn rate, optimizing costs, and securing non-dilutive funding opportunities.

- Market Expansion: Further penetration in Asia-Pacific and European markets, leveraging new regulatory approvals.

Result vs. Market Expectations

- Revenue growth met expectations, but the net loss widened significantly, which may disappoint investors.

- The company’s expansion strategy and increasing market penetration are positive long-term factors, but short-term financial performance remains under scrutiny.

Market Positioning

- AVITA’s share price has seen volatility leading into the results, reflecting both optimism about revenue growth and concerns over rising losses.

- The stock remains well below its 52-week high, signalling cautious investor sentiment amid ongoing operational challenges.

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Quick Take: FY2024 ASX:AVH