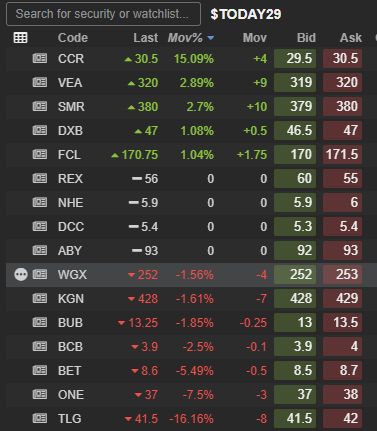

Let’s have a quick look at some announcements from today.

These companies have reported quarterly cash flows or had significant announcements today. I will proceed to comment on a few that have caught my eye for one reason or another.

There were plenty of other stocks that are not on that list. A lot of them are garbage stocks that are nowhere near operating cash flow positive let alone profitable.

Credit Clear ASX:CCR

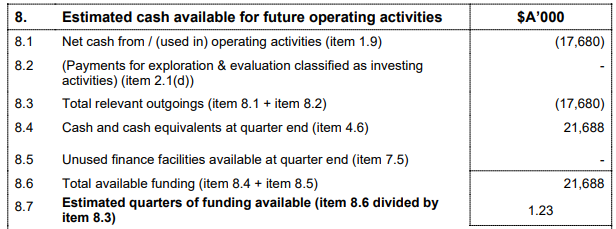

The standout quarterly report of the day and quite possibly their last since they have now achieved positive operating cash flows for the last 5 quarters and should no longer be required to do so.

It will be interesting to see where the share price finishes the day, but for now it’s looking like today’s result will see it break out of the range it has been trading in for most of this year.

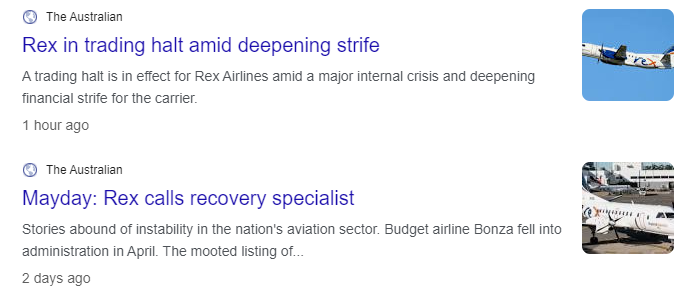

Regional Express ASX:REX

Not a stock I follow. When I saw this announcement my first thought was that perhaps they were going to receive a takeover bid. However, a quick google search suggests this won’t be a positive announcement.

Airlines are notoriously terrible investments. QANTAS ASX:QAN is (was?) considered one of the best in the world even it has had to lean on the government for support at different times over the years.

The chart of this company has been flashing “RED ALERT” for some time now. Ultimately it is a sad day as the Australian consumer will be the loser if this airline is about to fall over.

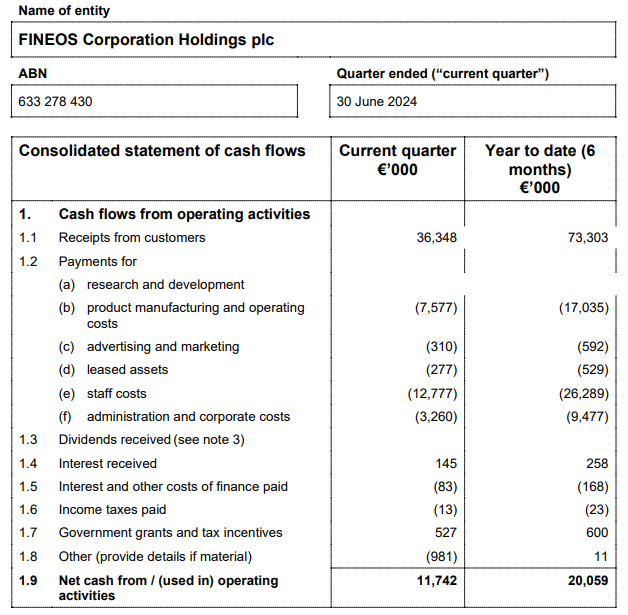

Fineos Corporation ASX:FCL

At face value, this looks to be a strong report for ASX:FCL. This company listed a while back now with a lot of hype surrounding it. The hype has proven to be unfounded.

There is nothing wrong with this result except this company has provided reports like this in the past only to slap shareholders in the face the following quarter. It needs to string a few more of these together before I will give it further consideration.

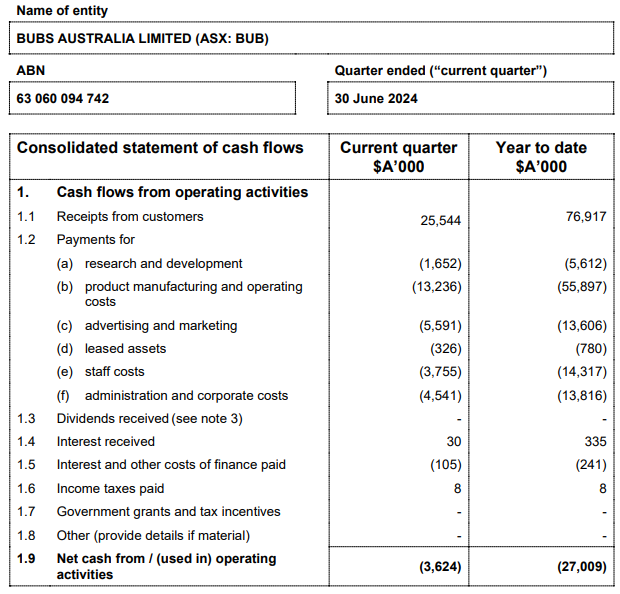

Bubs Australia ASX:BUB

Another 4c stock that seems promising at first glance since operating losses continue to narrow. However, a major concern is the significant shareholder dilution. Although the revenue has increased compared to the previous period, it’s actually decreased on a per-share basis. This underscores the importance of always reviewing a company’s share issuance history. If and when this company becomes cash flow positive and profitable, the sheer number of shares outstanding means it will need substantial growth to generate meaningful returns for shareholders.

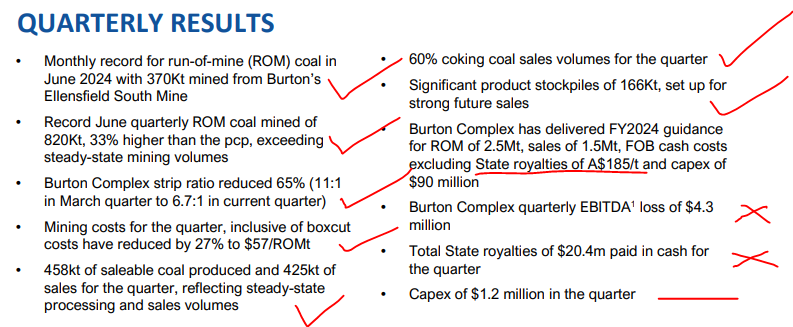

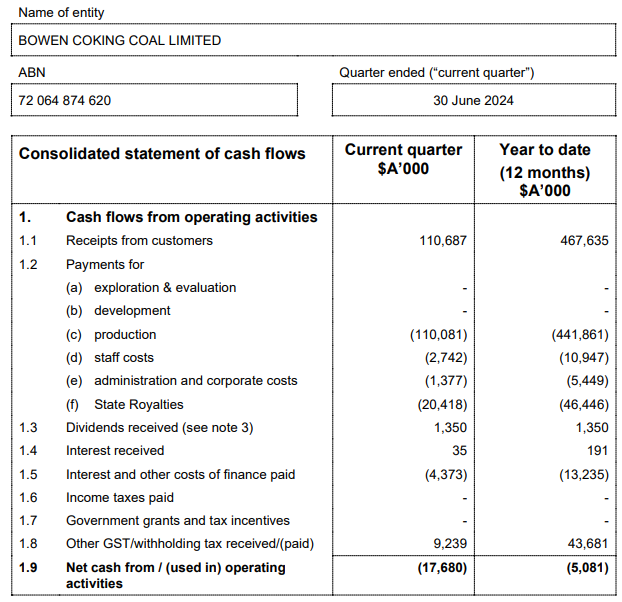

Bowen Coking Coal ASX:BCB

Doesn’t sound too bad. Often the commentary does.

This is why I almost always ignore the commentary unless these numbers appeal to me first. Yuck! Cost of production was the same as receipts. Pretty unfair they have to pay $20M in QLD state royalties when they’re not even close to profitable.

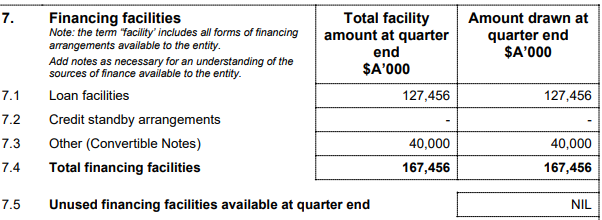

Oh dear, they’re in debt to their eyeballs too! Amazing to think I’ve seen this stock recently promoted as a spec buy by a very prominent stock broking house recently.

And for the trifecta, they’ve just about run out of cash.

I’ve heard a lot of commentary about coking coal vs thermal coal and how you want exposure to the former over the latter. This stock was proposed as one of the way to get that exposure. No thanks!

By the way, for what it’s worth, I don’t think either forms of coal and the stocks that give exposure to that are that enticing right now. For one they are highly cyclical so by definition can never be considered high quality. Ultimately ,they are producing something we need but it is bad for the environment. Lastly, they’ve never been great investments. Sure if you picked a few before Russia invaded Ukraine (which I did by the way but have since sold) then you will have done well. But before that yuck. Since then, some yuck, some ok. Going forward – why bother? Surely we can find better opportunities without the ups and downs of the cycle to worry about, with higher returns on equity that are actually contributing to the world in a positive manner?

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Announcements July 29

BCB a shocker. Got sucked in by the high quality coking coal that they have but market needs have changed. Was a stock I hoped to make some short term profit on and at one stage I was making a profit- but didn’t sell 😢😢

Sorry to hear that Steve. Yeah, things were looking good for them at one stage but the coking coal price isn’t as buoyant as it once was and the Queensland Royalties tax has been a highly questionable decision.

It’s one of those now that I will keep hoping for a bump. I had sold some earlier so I’m ok with keeping the rest. Still disappointing though. Bit like Kalium Lakes. High on potential but circumstances/ run by fuckwits has made for a sad tale.