Let’s have a look at some companies reporting today.

Reporting Season 21/08/2024

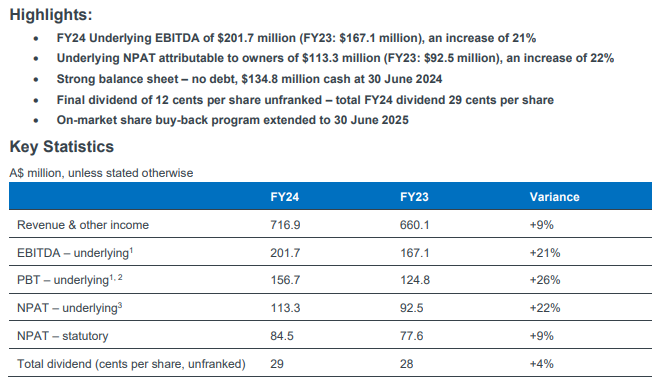

Corporate Travel Group ASX:CTD

https://www.travelctm.com/global/

Revenue: $716.9M vs $745.54 expected

EBITDA: $201.7M vs $215.16M expected

The result for this company look solid but well below market expectations. It would appear things have changed for this company but the market has been slow to accept it. The business is growing well but nothing like it has in the past.

Not a great outlook. This is certainly an above average company on our market and will at some point be worth buying again but it looks like their outlook for the next 6-12 months will be a disappointment to the market today.

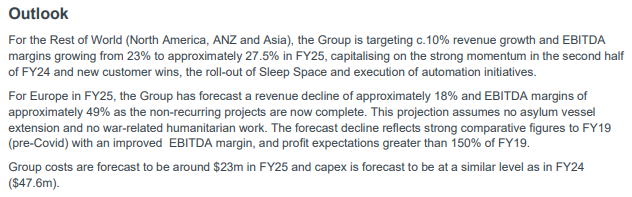

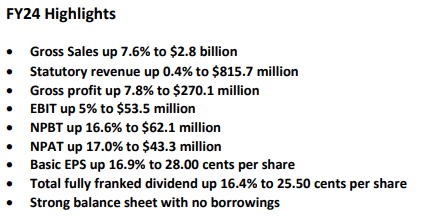

Data 3 ASX:DTL

Sales: $2.8B vs $2.85B expected

EBIT: $53.5M vs $54.45M expected

NPAT: $43.3M vs $43.5M expected.

Swings and round-about but all in all looks to be in-line with market expectations.

Outlook is upbeat but no guidance was provided.

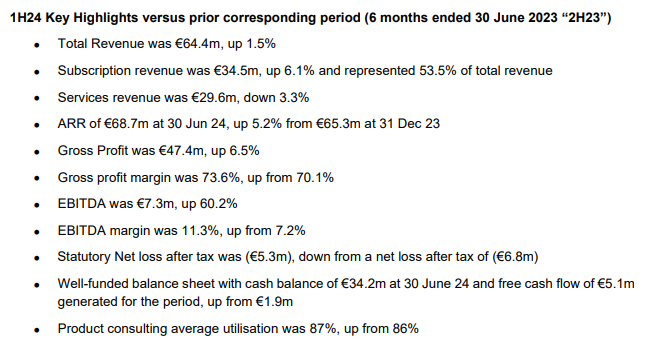

Fineos ASX:FCL

This is a company where I notice the analysts are always overly bullish. Let’s see if ASX:FCL finally lives up to the hype.

Revenue: 64.4M Euros vs $64.55M

EBITDA: 7.3M Euros vs (no guidance) (FY guidance $17.23M)

It’s a bit of a hard one. When we’re talking about revenue growth of 1.5% thought it’s hardly worth worrying about especially when there are so many other great companies reporting today.

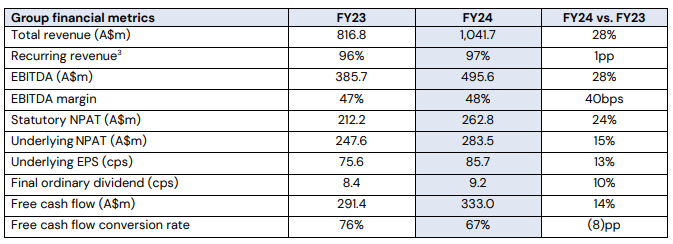

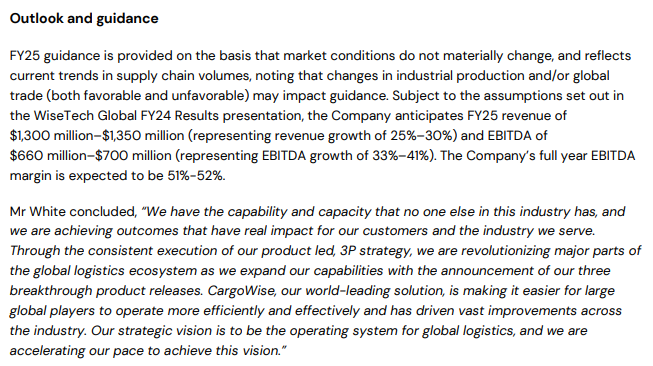

Wisetech ASX:WTC

This company has had a strong run in the past 6 months. It will be interesting to see if they can match what I gather to be lofty expectations.

Revenue: $1041.7M vs $1063.54M expected

EBTIDA: $495.6M vs $490.63M expected a beat based on higher margins

NPAT: $283.5M vs $272.83M

This looks like another very good result which has been able to exceed market hopes.

That is one helluva outlook!

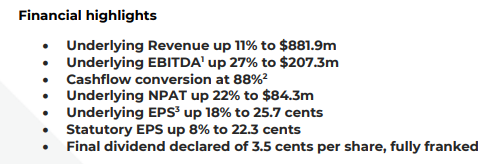

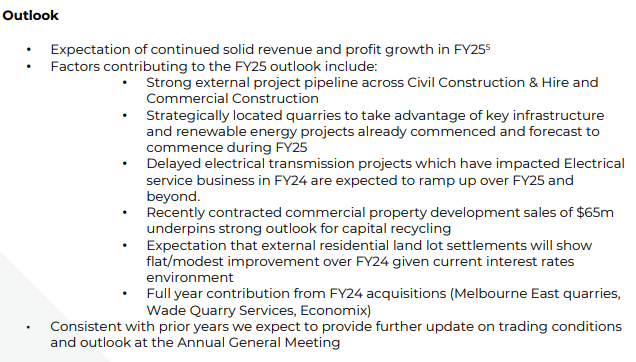

Maas Group ASX:MGH

Revenue: $881.9M vs $1008.14M expected

EBITDA: $207.3M vs $206.28M expected

NPAT: $84.3M vs $84.15M expected.

This appears to be an in-line result or a slight beat. Strange the revenue numbers seems to differ so greatly.

Sounds positive enough.

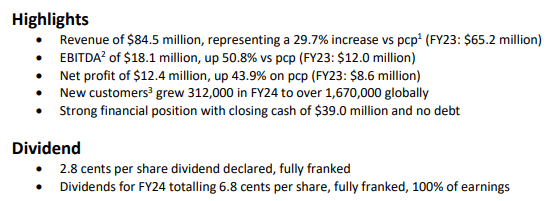

Step One Clothing ASX:STP

Revenue: $84.5M vs $83.6M expected

EBITDA: $18.1M vs $17.2M expected

Net Profit: $12.4M vs $12.2M expected

A very strong result and a slight beat on market expectations.

No numbers here.

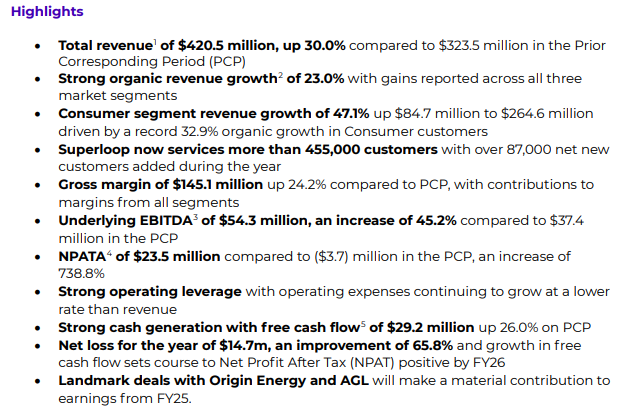

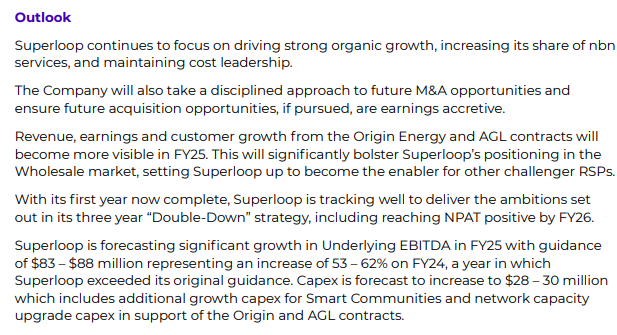

Superloop ASX:SLC

Revenue: $420.5M vs $412.51 expected

EBITDA: $54.3M vs $53.34M expected

NPATA: $23.5M vs $22.35M expected

A strong result which is slightly ahead of market expectations.

Guidance for very strong EBITDA growth to $83-$88M which the market was already expecting at $87M.

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Reporting Season 21/08/2024 – Today I have a look at ASX: