Let’s have a look at some companies reporting today. Much fewer than the last couple of days.

Reporting Season 23/08/2024

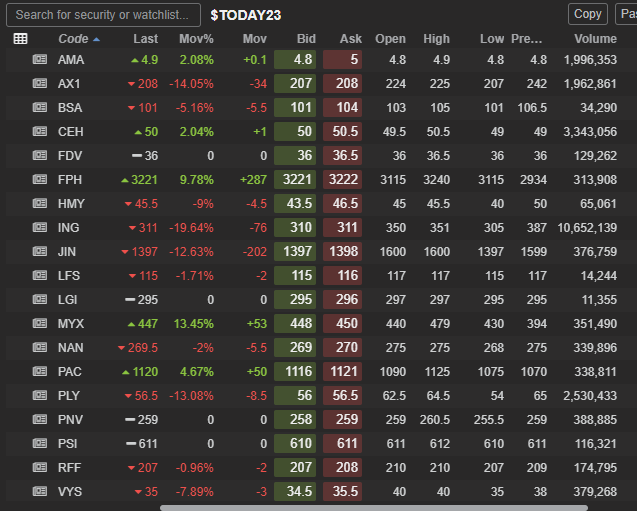

Playside Studios ASX:PLY

Revenues: $64.6M vs $64.4M expected

EBITDA: $17.5M vs $17.3M expected

NPAT: $11.3M vs $10.07M expected.

The result appears to be a slight beat. No guidance was provided by the company explaining they will do so at the AGM in October.

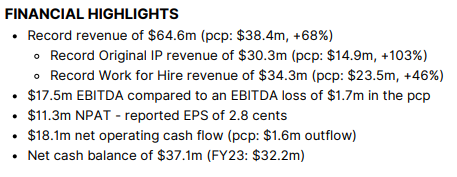

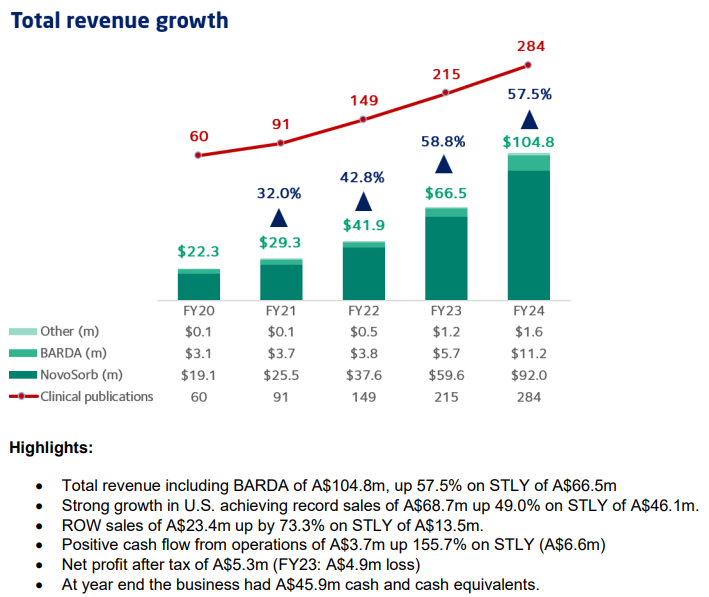

Polynovo ASX:PNV

This company provides quarterly updates so I can’t imagine there will be too many surprises in this one.

Revenues: $104.8M vs $104.4M expected and up 57.5% on last year.

NPAT: $5.3M vs $3.8M expected up from a lost last year of $4.9M.

This result looks like a solid beat at the NPAT level.

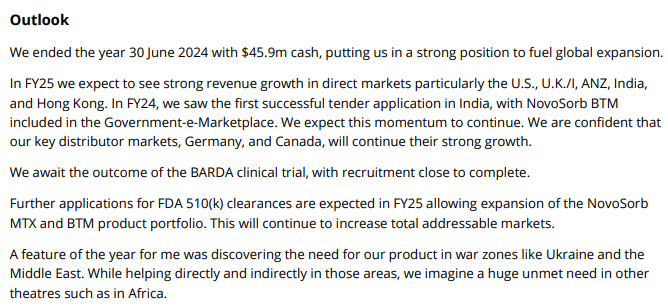

Positive outlook but no numbers given.

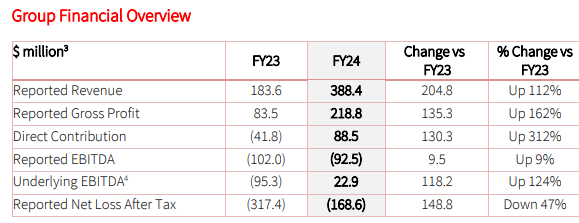

Mayne Pharma ASX:MYX

There’s some big “ups” there and a huge discrepancy between the reported EBITDA and Underlying EBITDA. A very messy company that is still losing a massive amount of money. But underneath all of that, is there a hidden gem?

Revenues: $388.4M vs $382.6M expected

Underlying EBITDA: $22.9M vs $18.96M expected

On those metrics the result looks like a beat.

Positive outlook but no numbers. The stock is up so the market is clearly happy to look through to the underlying and adjusted numbers to judge the performance of this business.

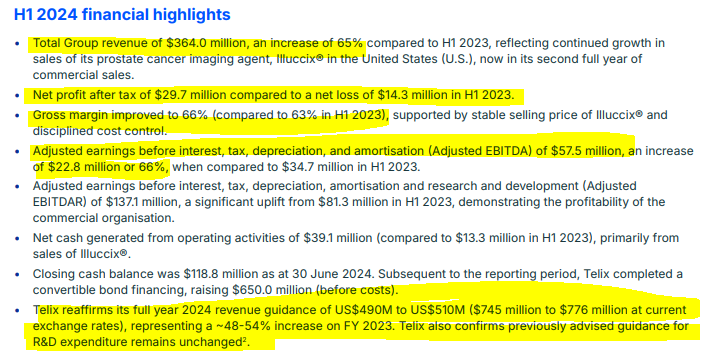

Telix Pharmaceuticals ASX:TLX (reported 1/2 year results yesterday after the close)

My data provider has already updated their numbers to reflect these results making comparisons between what is expected and what has been achieved difficult. I have annual numbers in my database so I will show how they have changed as a result of this updated.

Revenue forecast for 2024: Was $757.65M which has been revised higher to $764.66M

EBITDA forecast for 2024: Was $115.84M which has been revised higher to $124.71M.

All in all this company continues to grow at a phenomenal rate and is expected to continue doing so.

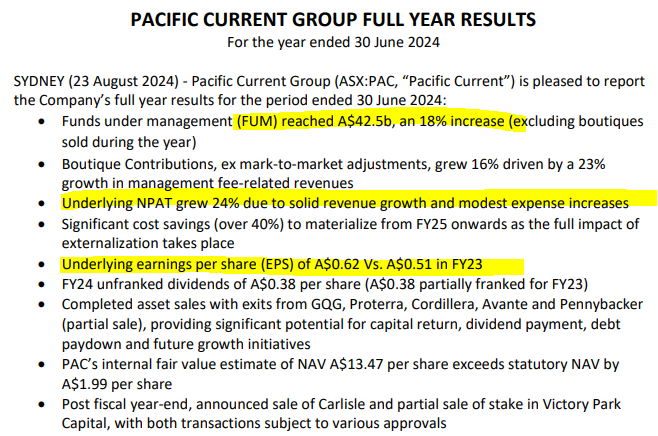

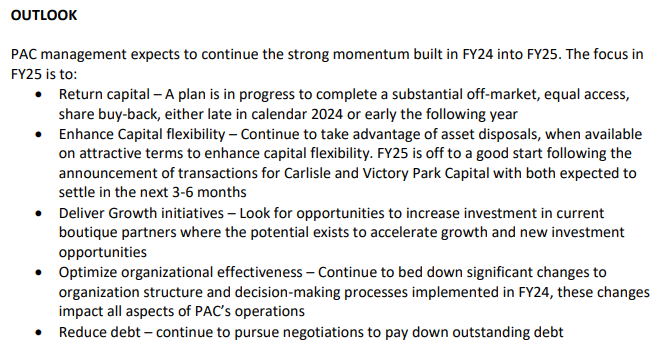

Pacific Current Group ASX:PAC

NPAT Growth: 24% vs 25.7% expected.

EPS: 62c vs 64c expected.

Not much to go on here. The company is growing strongly and the share price is up ~5% today. I notice the outlook for the company is positive while expectations are for revenues to fall and NPAT to fall 30%. I’d say the analysts may have been too negative on the prospects for this company next-year and some adjustments will be made, hence the positive share price reaction today.

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Reporting Season 23/08/2024 – Today I have a look at ASX:PLY, ASX:PNV, ASX:MYX, ASX:TLX and ASX:PAC