About

Austin Engineering Limited (ANG.AX) is an Australian-based global engineering company specializing in the design, manufacture, and supply of custom mining equipment and related services. Established in 1982, Austin Engineering focuses on creating innovative solutions for the mining industry, particularly in the areas of loading and hauling. Its product range includes off-highway dump truck bodies, excavator buckets, water tanks, and tyre handlers, all tailored to enhance productivity and safety in mining operations. The company operates through segments in the Asia-Pacific, North America, and South America, providing both proprietary products and repair and maintenance services. Austin Engineering has built a reputation for leveraging its engineering intellectual property and expertise to deliver customized solutions that meet the specific needs of mining companies, contractors, and original equipment manufacturers around the world.

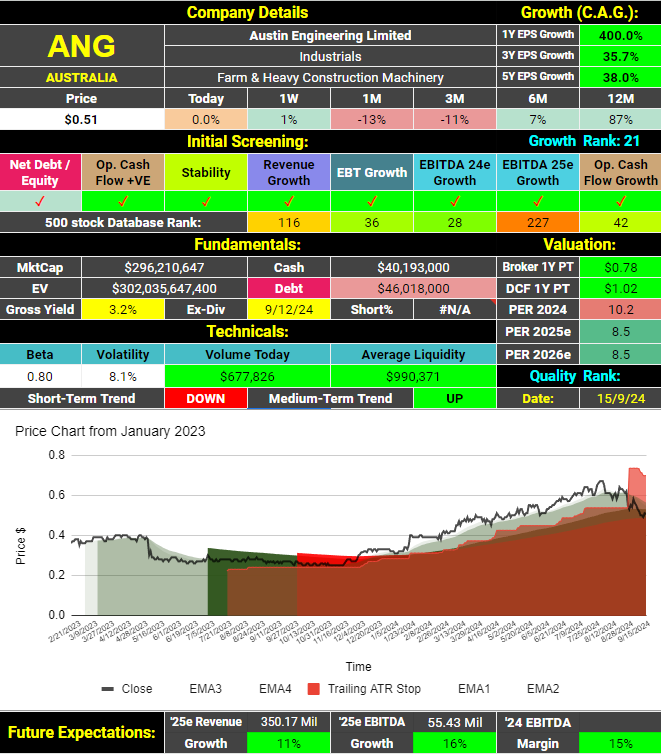

Update September 15, 2024

The full-year result announced in August has not been received well by the market. The share price has now moved in to a short-term down-trend. It does appear to have found some support at the medium-term duration moving averages. Growth from here is predicted to be slower than it was last year.

On a PER basis, the company appears cheap and the growth model agrees. The 2 analysts that cover Austin Engineering feel the shares are cheap with a consensus price target over 50% above the current price. Growth may be slowing but you would have to think the value investors out there would be getting interested in this company.

*** end update

Initial Screening

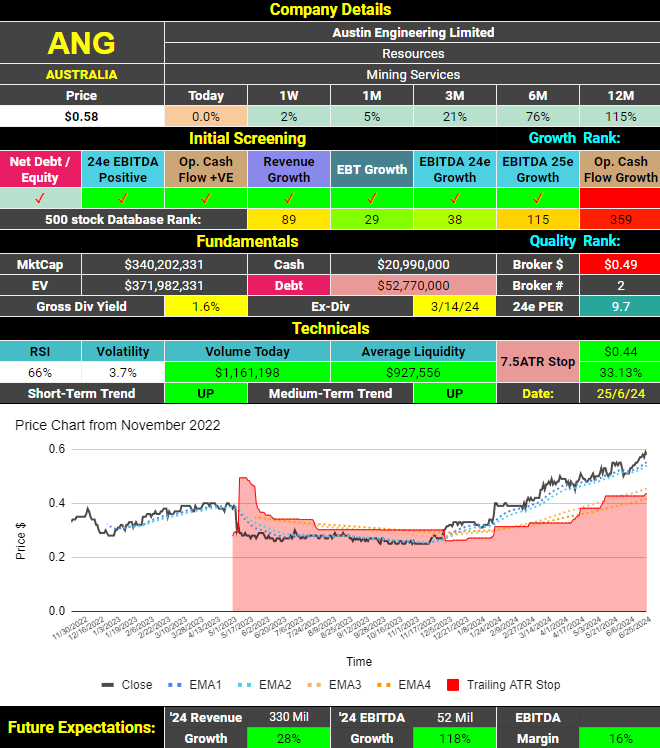

Austin Engineering (ASX:ANG) receives 7 out of 8 possible ticks in the initial screening. Debt is low and revenue and earnings are growing and expected to continue growing. The only blot on the report is that Operating cash flows have been falling. The company pays a small, fully-franked dividend. The share price has been in an impressive uptrend of over 12 months now seeing the shares 115% above what they were this time last year.

Fundamental analysis

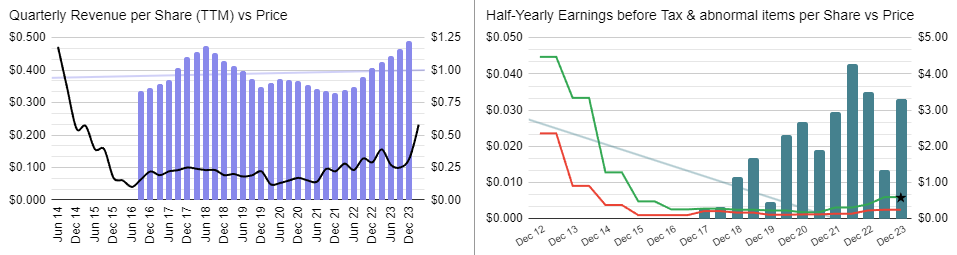

This company seems to be very different post ~2016 so we will look at it’s number from then:

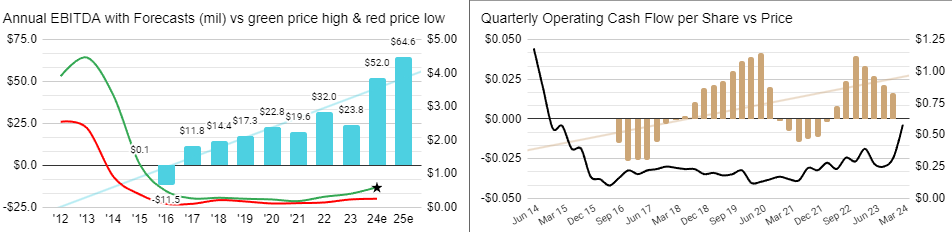

Like many mining services companies, historical performance appears cyclical. Presently the cycle seems to be in their favour.

Operating cash flows are most choppy of all for this company for some reason while EBTIDA has been more consistent. It could be that Operating cash flows fluctuate more due to changes in inventories since the company does manufacture and supply capital goods.

Austin Engineering (ASX:ANG) Analysis is #533 on the ASX list of most shorted stocks. This is less than 0.1% of the stock on issue. Short selling is not a factor for this company.

Quality Analysis

This company does not have a history of diluting its shareholders.

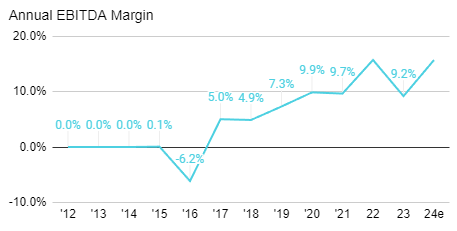

Revenues only increase slightly better than 1 in 2 times when this company reports. Earnings are more stable although nowhere near the levels of the best companies in this regard. Margins and ROE are both on the low side. Debt is low but regardless, this can only be considered a low quality company at this point in time.

Margins have been gradually trending higher which is clearly a positive. As we have seen above, earnings have been too. The company talks of being debt free this year. A lot of factors are moving in the right direction which will only see the quality of this company improve if they continue.

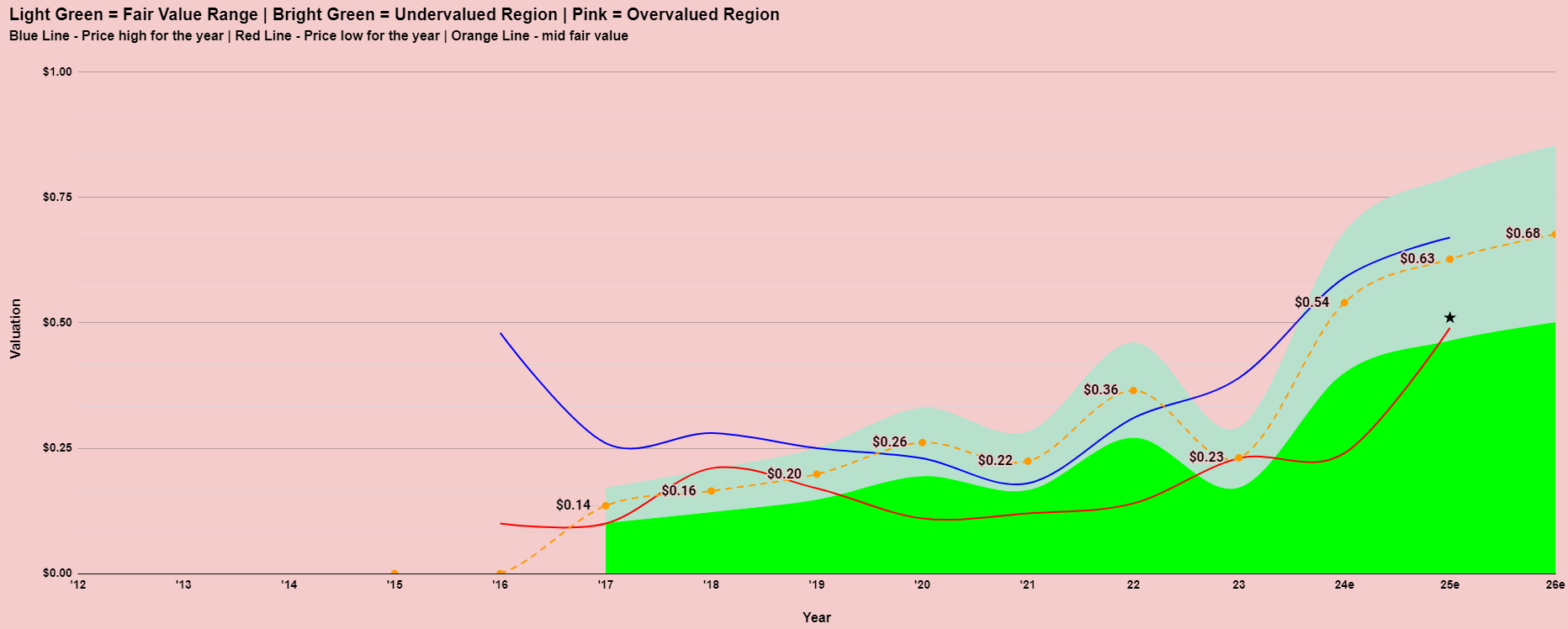

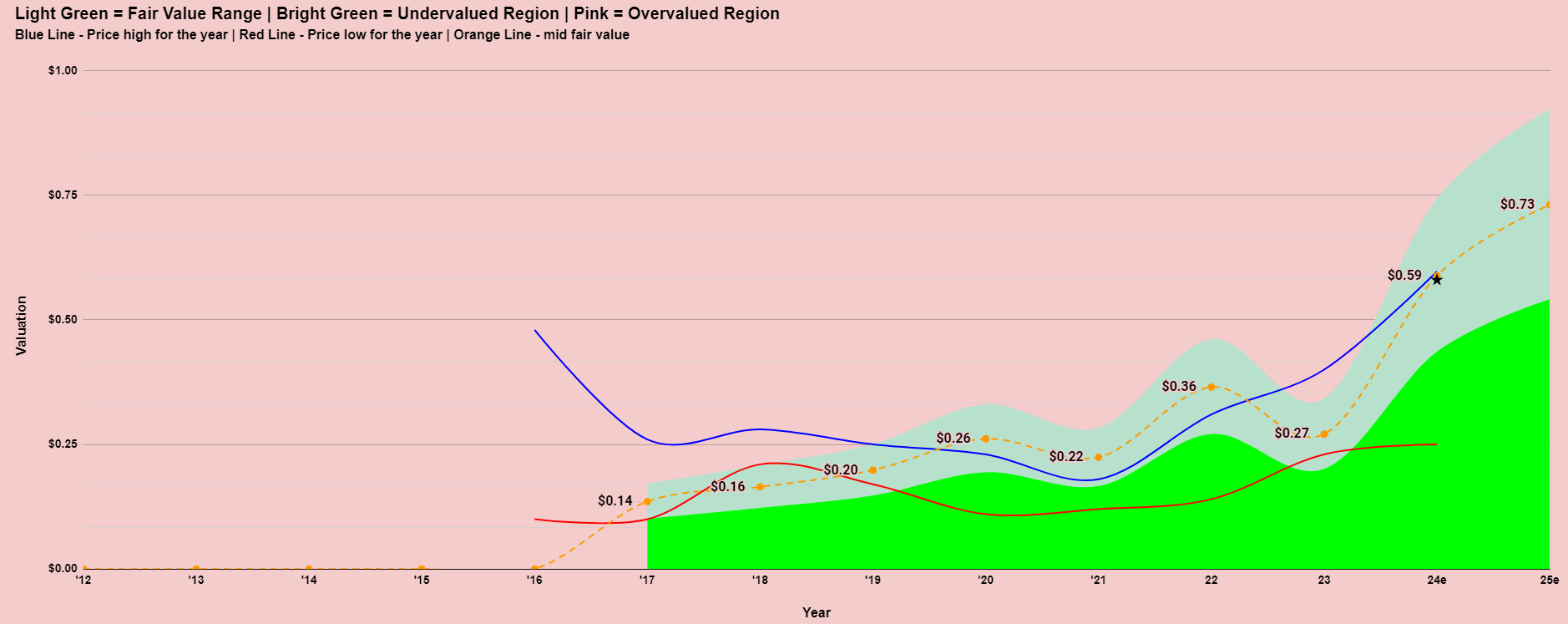

Valuation

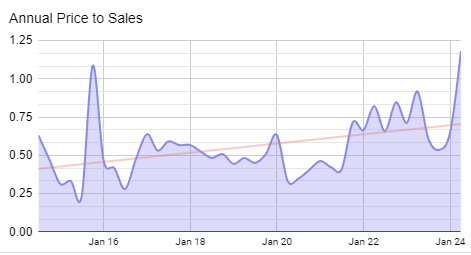

The market is viewing Austin Engineering (ASX:ANG) quite favourably at present with the shares being rewarded with its highest price to sales ratio ever over the period of time which I am looking. Despite this, the Price Earnings Ratio based on expected earnings this year (2024) is only 9.7. It is possible this will continue to rise as the company continues deliver improved results.

Having such a choppy past makes it hard to get a grip on the appropriate valuation of this company. The valuation model is suggesting its now trading somewhere around fair value. As we can see though, it has rarely traded around that level of extended periods of time.

News From The Company

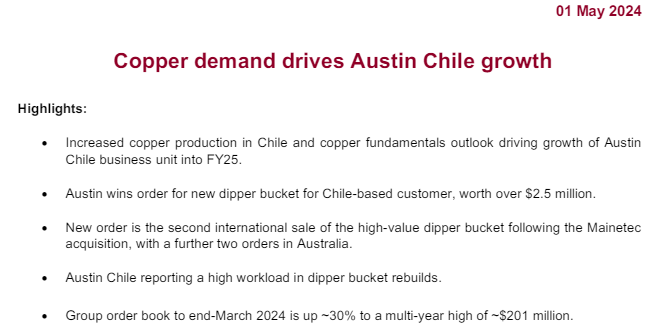

It would appear that the surge in copper price from February to May this year has been beneficial for this company. It must be noted that the copper price has fallen back quite a lot through June from a peak of over $5.10 a pound in May to a current price of $4.44 (25/6/24).

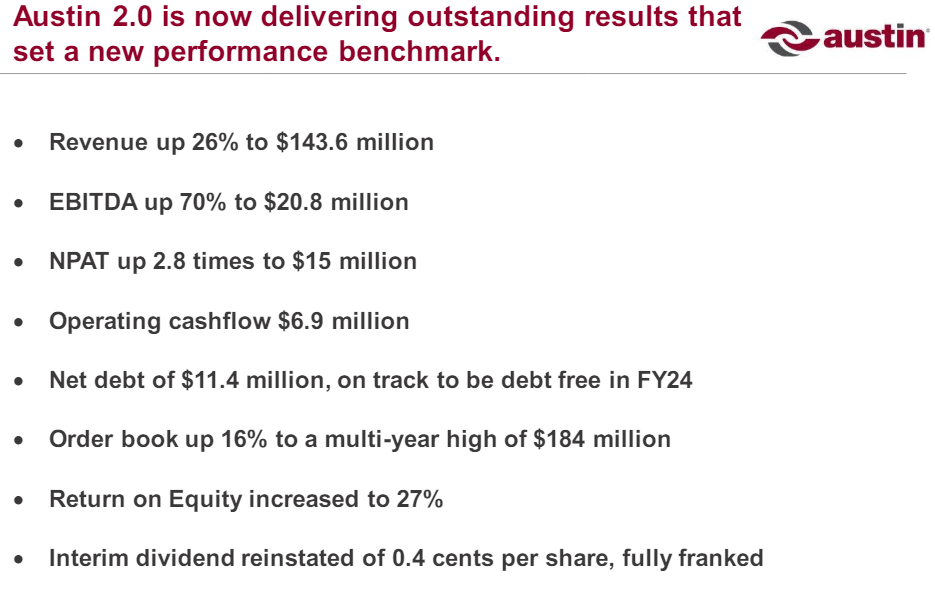

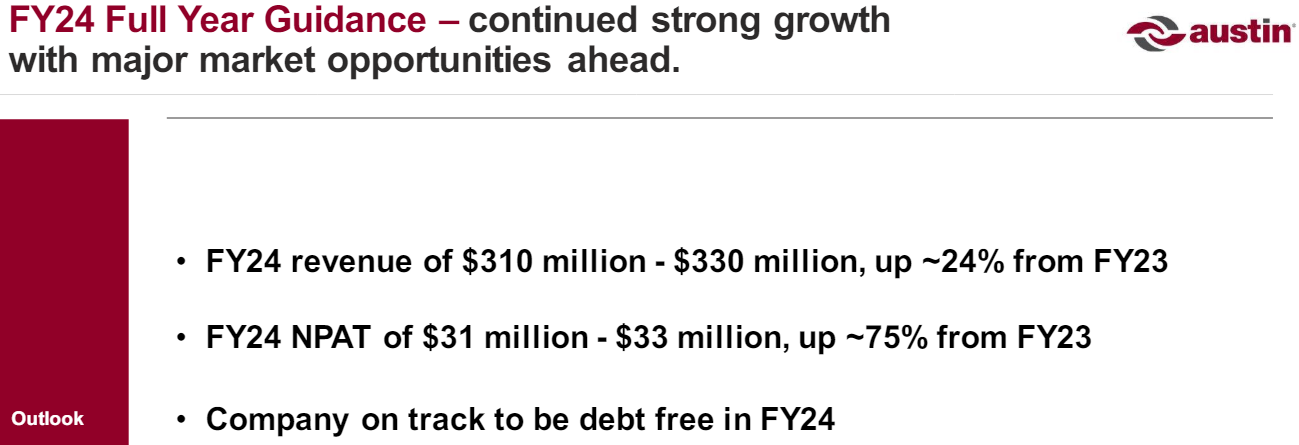

Source: Rottnest Conference Presentation March 2024

The company is very positive in their outlook .

Technical Analysis

Note: This is a live chart. The technical analysis in this report should be considered up to the date of this report.

The share price of this company is in a short and medium term uptrend.

Final thoughts on Austin Engineering (ASX:ANG)

Austin Engineering (ASX:ANG) is a turnaround story. Like many turnaround stories, it can look a bit ugly at first glance. If we allow ourselves to zoom in on what the company has been doing in more recent times then the picture improves a lot. This is a cyclical stock though, but nevertheless, the cycle seems to be favourable for them at the moment. The share price has been rising along with the valuation the market is prepared to give it. By many measures that valuation still appears low with a PER of just 9.7 based on expected earnings this year. The outlook from the company is positive with a strong forward order book. Momentum is to the upside and nothing from the latest communications from the company suggests that is about to change.

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Austin Engineering (ASX:ANG) Analysis