About

CSL Limited (ASX:CSL) is a global biopharmaceutical company based in Melbourne, Australia. Founded in 1916, it develops, manufactures, and markets biotherapies, vaccines, and blood plasma products. The company operates through two main segments: CSL Behring, which focuses on plasma-derived therapies for conditions like hemophilia and immune deficiencies, and Seqirus, which specializes in influenza vaccines. CSL Behring also plays a key role in recombinant protein and monoclonal antibody treatments for chronic and acute conditions. Known for innovation, CSL invests heavily in research and development, expanding its pipeline with gene therapies and novel vaccines. With operations in over 30 countries, it serves global markets, delivering life-saving and life-improving treatments.

Update January 27, 2025

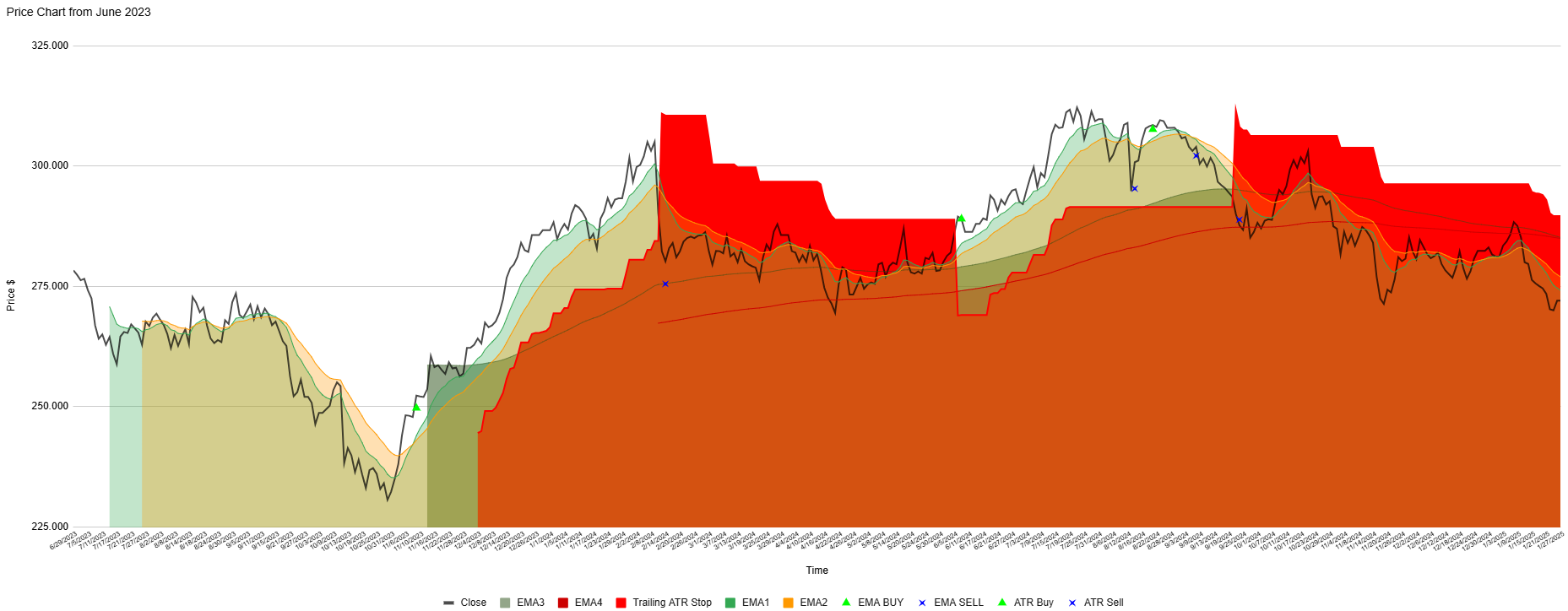

The price chart of CSL today is basically where it was at the start of the chart period. In that time, two profitable short-term trades have been generated by the 3EMA and ATR indicators with one losing trade. There are currently no open trades suggested as the share price is trending lower again.

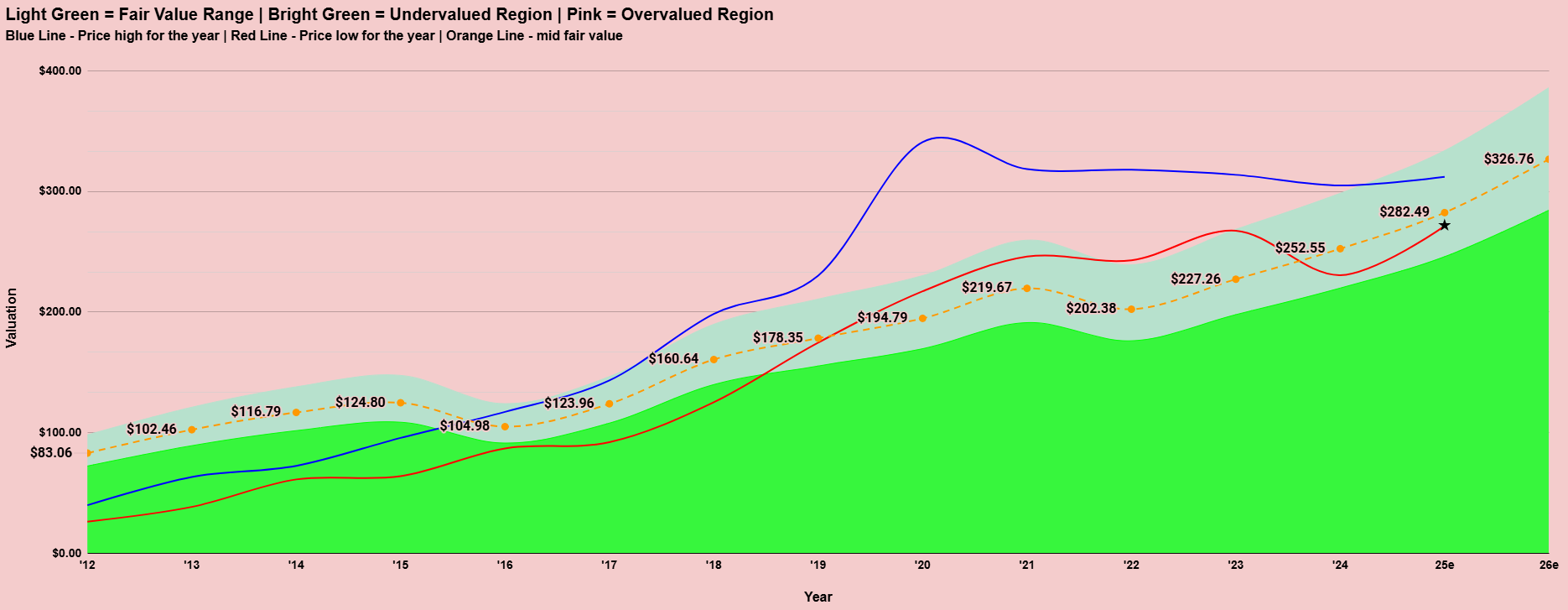

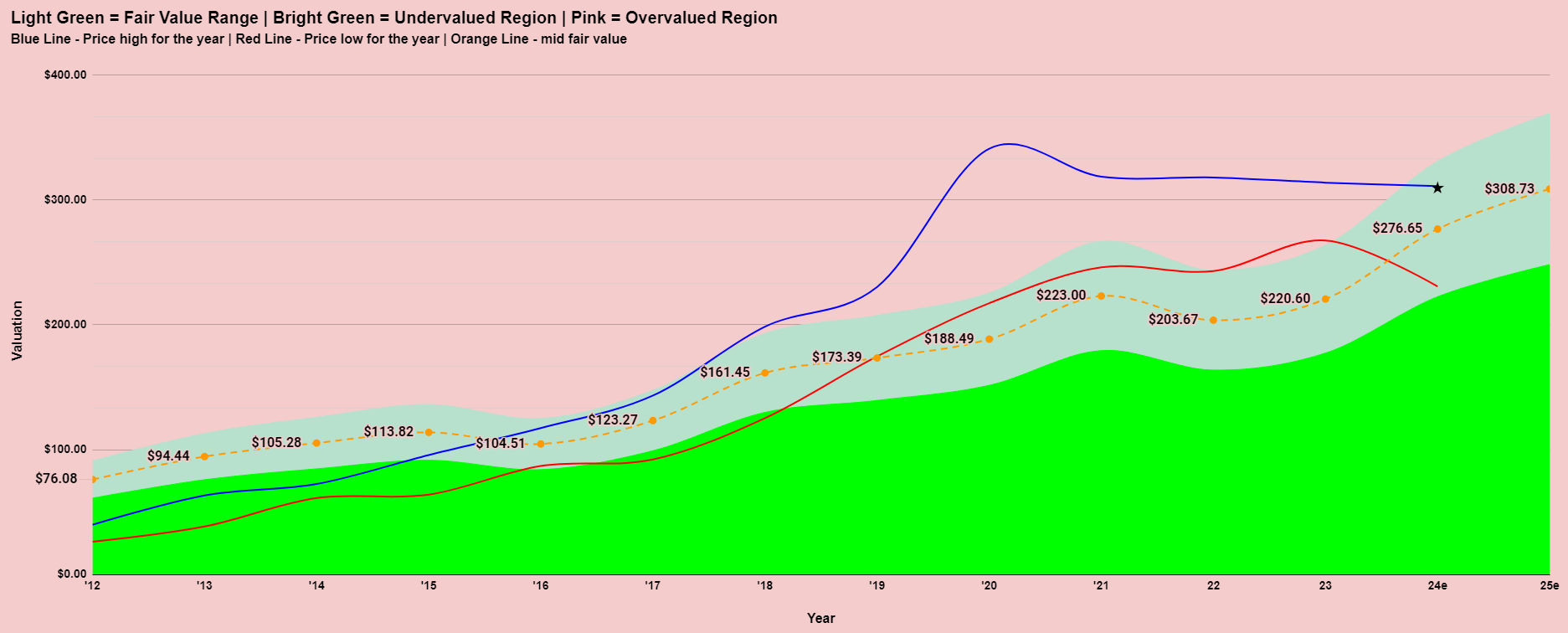

Overall, CSL has actually been in a sideways trading pattern since 2020 as can be seen on the valuation model chart below. In 2020, the valuation was over $100 above the model suggestion for fair value. After 4 solid years of consolidation, earnings have now caught-up and to the point where we now find CSL trading a little below fair value. If CSL can deliver some growth when it next reports around February 11, it might just be ready to start a new uptrend.

*** end update

Update September 16, 2024

The latest result was ok but not enough to push CSL up and out of the sideways pattern it has been trading in since 2020. The growth outlook is for lower growth than was expected in 2024. The acquisition from a couple of years ago has not delivered as they had hoped. The rest of the business continues to perform well. If they can get the Vifor acquisition to deliver, that would probably be the catalyst to see them move into an uptrend once again.

For now, there doesn’t appear much value here with a PER in the 40’s and forecast growth of just 14% in EBITDA and a grossed up dividend yield of just 1.4%. The valuation model which is based on how the market has been prepared to value the company in the past, suggests shares are trading close to fair value. The analysts love it though, suggesting the shares should be around 10% higher than they are today.

*** end update

Initial Screening

CSL (ASX:CSL) earns a tick on all 8 initial screening metrics. Revenue and earnings are again expected to have grown when they next report their results on August 13. The share price has recently moved into an uptrend based on the short and medium term moving averages although it remains within a longer term range. This has seen it move above the average broker price target. This is after an extended period of sideways price movement. It pays a small dividend and have a small amount of debt relative to its size.

Fundamental analysis

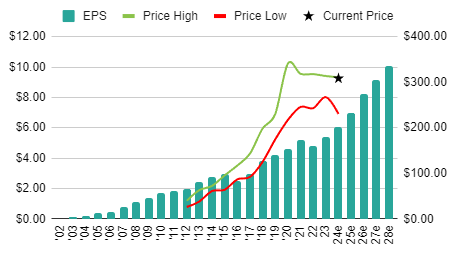

CSL (ASX:CSL) had been a great performer for investors over a number of years until the share price peaked in February, 2020. Despite the peak coming in 2020, the shares showed continued growth in earnings up until 2022. A fall for a year then saw a return to growth in 2023. Analysts are forecasting further growth in the years ahead.

CSL (ASX:CSL) is a growth stock, albeit there are many growing faster in my database.

CSL (ASX:CSL) is ranked #302 on the ASX Most Shorted Stocks List. 0.4% of its shares are currently short sold. This is insignificant.

Quality Analysis

Debt and shares on issue were reducing until 2022 when the company made an acquisition. Nevertheless, debt remains at conservative levels. It’s also encouraging to see that CSL has shown the desire to reduce debt in the past.

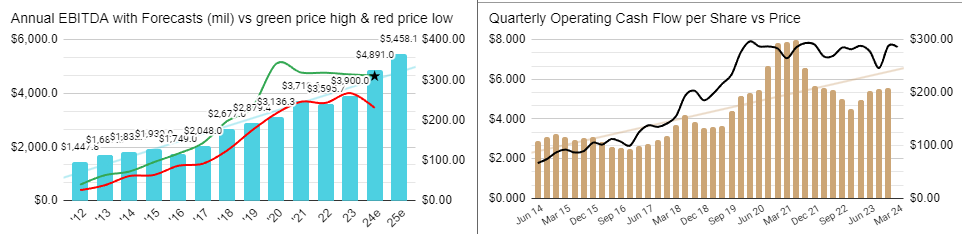

Zooming out, we can see that the company has been an incredible earnings grower for over 20 years. Analysts don’t see any reason why this won’t continue from here.

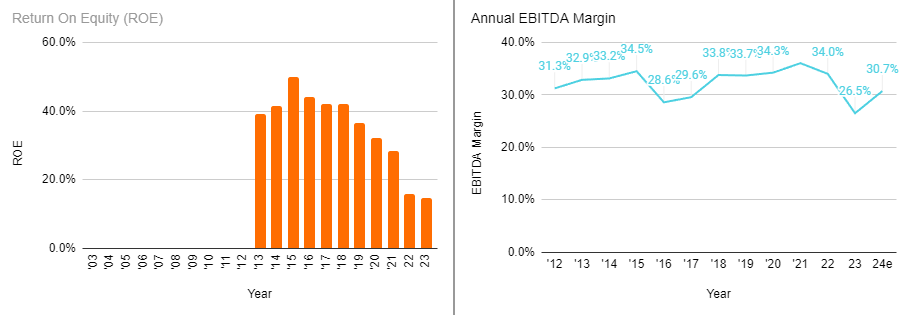

Return on Equity (ROE) has been falling since 2014. This could partially be explained by the declining debt in the company over that time. However, ROE failed to bounce back in 2023 despite the addition of some debt once again. EBITDA margins have hovered roughly between 30 and 35% although they were 26.5% in the last results. The market is forecasting them to bounce back when they next report.

The company reports an increase in earnings 87% of the time. Earnings before tax and excluding abnormal items is less at 67%. Margins of 27% are below historical highs as is the ROE of 15%. Debt is manageable at 65%. As it stands today, CSL (ASX:CSL) can only be considered a medium quality company. In the past it would have been amongst the highest quality companies on the ASX but some key metrics have deteriorated in recent years.

Valuation

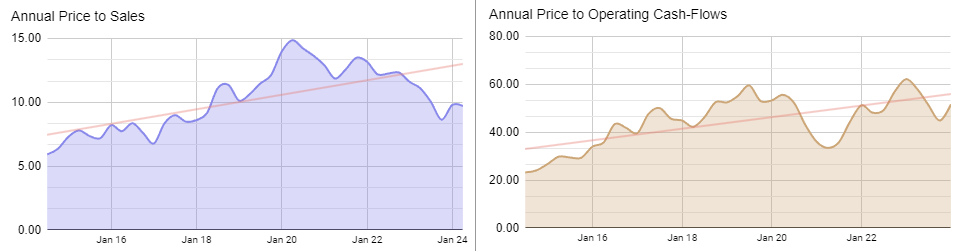

The long-term trend for Price to Sales and OCF to sales has been rising. Currently, the company sits comfortably below trend and certainly below previous highs for these metrics.

I think the valuation model tells the true story of this company and that is one of a valuation that got WAY ahead of itself. What followed from 2020 until today was an extended period of sideways price action as the market waited for the fundamentals to catch up. This year has seen the share price hovering in the fair value range once again.

Technical Analysis

As explained above, the share price has essentially been moving sideways after the uptrend ended in 2020. The share price is once again making a move towards the top of the range. The difference this time is that shares are no longer significantly overvalued. Should it be able to show a good result when it next reports it may just be ready to create a new high and start a new uptrend.

News From The Company

There has not been a lot of news coming out of the company. The most recent is a presentation from April.

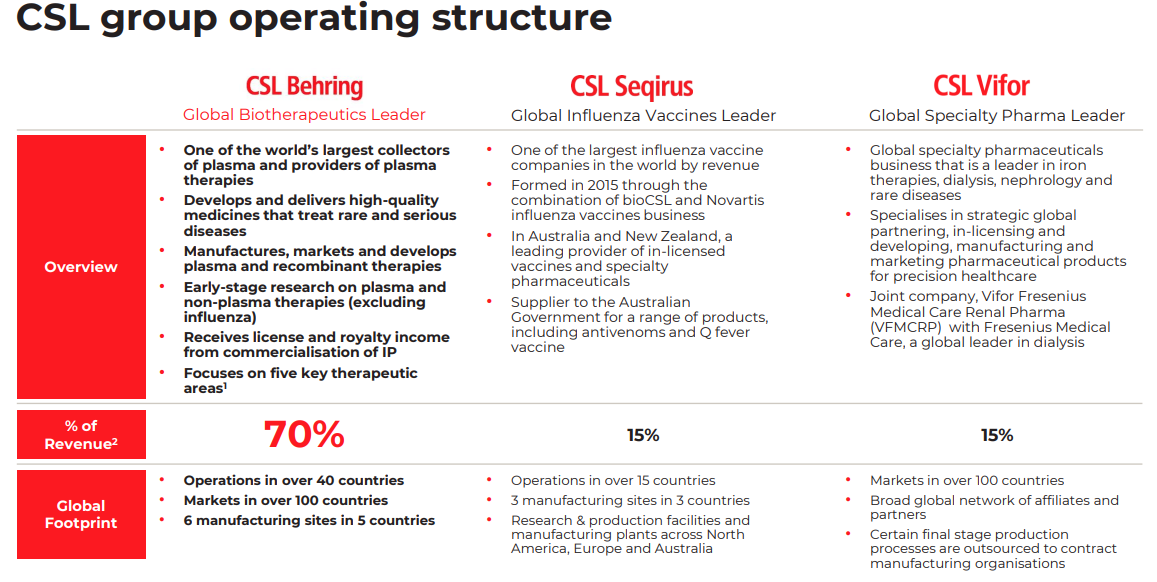

A lot of focus has been on the acquisition of Vifor. While this is clearly an important step for the company, it would not “break” them if it wasn’t as good as first thought. The CSL Behring division will always be the main driver with it comprising 70% of revenues.

Going back to their half year results presentation in February, we have this Outlook statement which would be assuring for investors if it is achieved.

Final thoughts on CSL (ASX:CSL)

CSL (ASX:CSL) experienced a period of overvaluation by the market, followed by years of consolidation, eventually bringing its valuation in line with fundamentals. Some quality metrics have declined due to COVID-19 disruptions and a less profitable-than-expected acquisition. However, the potential for the company to regain its former status remains.

Technically the shares have moved to the top of their 4 year range where once again they will attempt to break free and commence a new uptrend. This will need to be supported by fundamentals though. A strong outlook from the company in February could just be the catalyst for a meaningful move higher if achieved, when they report their full year results in August. A miss or a disappointing outlook could see them spend another year gyrating between ~$240 and ~$320.

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

CSL (ASX:CSL) Analysis