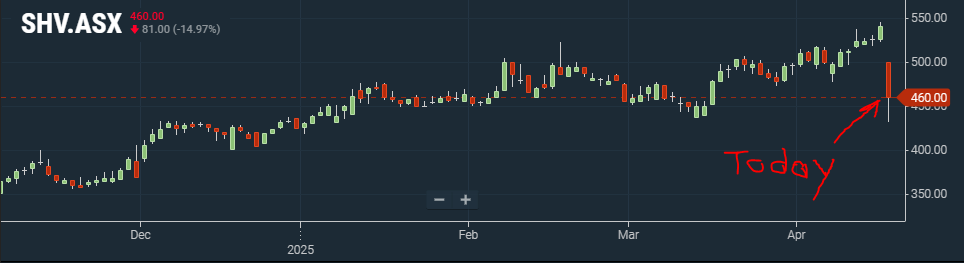

Select Harvests has released an update to the market today (Wednesday April 16). It included a downgrade to production with an upgrade to almond pricing. The market has responded negatively to the news in early trade. Let’s try and determine if this initial market reaction is appropriate.

🥜 Select Harvests – April 2025 Business Update Summary

Website: www.selectharvests.com.au

📢 Overall Report Tone

Select Harvests has issued a constructive update amidst a challenging crop year. Despite a lower-than-expected almond production, the strong pricing environment and strategic execution are expected to offset volume headwinds, reinforcing management’s confidence in delivering long-term value.

📊 Key Financial and Operational Metrics (Per Share Where Possible)

| Metric | FY24 (AGM) | March 2025 Briefing | April 2025 Update |

|---|---|---|---|

| Revenue | $337m | Confirmed | Not updated |

| Almond Price (forecast) | $7.69/kg | $9.20/kg | ↑ $10.35/kg |

| Crop Volume Forecast | 29,527MT (actual FY24) | 27,500–29,000MT (March) | ↓ 24,000–26,500MT |

| Exchange Rate Hedge | Not disclosed | 86% of 2025 crop hedged at 0.648 | Confirmed |

✅ Positive Surprises or Potential Positives

-

📈 Almond pricing upgraded to A$10.35/kg, up from A$9.20/kg in March and A$7.69/kg in FY24. This represents a +35% YoY price increase and supports profitability despite lower volumes.

-

🌐 Strong global demand, particularly from China and India, is sustaining price strength.

-

🏭 Processing capacity expansion continues at Carina West, helping to scale efficiently into future years.

-

💵 86% of 2025 crop is hedged, reducing FX risk in volatile markets.

⚠️ Potential Concerns or Headwinds

-

🌾 Crop downgrade from 27,500–29,000MT to 24,000–26,500MT, driven by poor bloom strength, large hulls, and frost damage (~500MT).

-

🌿 The Nonpareil variety’s crack-out rates are lower, impacting kernel yields.

-

🌧️ Continued weather volatility in NSW presents a risk for future crop consistency.

-

🧪 Strategy benefits expected from 2026 onwards, indicating muted near-term uplift from transformation efforts.

📊 Results vs Market Expectations

-

🔼 Analysts were previously modelling A$9.20/kg pricing, so A$10.35/kg represents a beat.

-

🔽 However, volumes are materially lower, likely dragging revenue and EBITDA forecasts down despite price support.

-

📊 Analysts will likely need to trim volume forecasts but increase realised price assumptions, creating a mixed revision outlook.

🔮 Outlook and Guidance

-

🌎 Almond macro tailwinds remain intact, including rising demand, constrained US supply, and low global inventories.

-

🏗️ Strategy remains unchanged – scale-up, cost management, customer expansion, and margin capture.

-

🌱 New horticultural strategy should show tangible results from 2026, with full benefits expected in 2027.

-

🔁 Despite lower 2025 crop, management sees no ongoing structural impact on future crops.

🔍 Analyst Forecast Revisions

🔻 Crop Downgrade

-

Previous FY25 Crop Forecast: 27,500 – 29,000 MT

-

Updated Forecast: 24,000 – 26,500 MT

-

This ~10% downgrade in volume reflects weaker bloom and low crack-out rates (particularly from Nonpareil), plus 500MT frost losses. This will likely pressure revenue and EBITDA forecasts downward, all else equal.

🔺 Pricing Upgrade

-

Previous FY25 Price Forecast: A$9.20/kg

-

Updated Forecast: A$10.35/kg (~12.5% increase)

-

Higher almond pricing, driven by global supply tightening (especially California) and strong demand from China and India, more than offsets the crop downgrade on a dollar basis, likely lifting margin expectations and partially or fully offsetting the crop volume impact on EBITDA.

🎯 Forecast Implication:

-

Revenue: Likely to remain flat to slightly up, as higher price offsets volume loss.

-

Adjusted EBITDA: Likely to be revised up slightly, particularly if hedging gains and cost discipline continue.

-

EBT (Earnings Before Tax): Should benefit from pricing tailwinds and lower production costs — mild upward revision likely.

📌Conclusion

Despite a crop downgrade, higher almond prices and favourable hedging are expected to offset volume losses, leading to stable or slightly higher revenue forecasts. Adjusted EBITDA and EBT are likely to be revised upward due to improved pricing, cost efficiencies, and operational execution. Overall, the outlook remains positive with strong momentum into FY25.

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Select Harvests (ASX:SHV) April Update