This content is restricted to Supporters. Please Sign In.

Not a member? Follow the for a Free 14 Day Trial (no credit card required).

This content is restricted to Supporters. Please Sign In.

Not a member? Follow the for a Free 14 Day Trial (no credit card required).

This content is restricted to Supporters. Please Sign In.

Not a member? Follow the for a Free 14 Day Trial (no credit card required).

📅 July, 2025

🌐 Website: https://findi.co/

Here is a forensic financial analysis of Findi (ASX:FND), based on its FY25 Annual Report (year ended 31 March 2025).

| Risk Indicator | Status | Comments |

|---|---|---|

| Goodwill >25% of Assets | 🔴 | Goodwill = $39.7M; Total Assets = $323M → 12% from Tata/BankIT acquisitions, but intangible assets overall ~$62M (19% of total) and rising rapidly. |

| Rising Receivables Days | ✅ | Receivables grew only slightly (to $8.2M from $8.1M) while revenue increased ~13%. No concerning rise observed. |

| Inventory Growth vs Profit | 🟠 Not Applicable | No inventory reported (services business). Not applicable but flagged as 🟠 to note working capital sensitivity to contracts. |

| High Borrowings | 🔴 | Total borrowings ~$123M ($85M current), Net Debt rising, finance costs up ~3x ($29.4M), Debt-to-Equity ~1.9x (258M liabilities vs 64M equity). |

| Loans to Related Parties | ✅ | No material related party loans disclosed beyond normal intra-group balances. |

| Idle Cash | 🟠 | ~$115.9M cash balance, but significant earmarked deployment. However, cash held exceeds 18 months of opex without detailed return disclosures. |

| Risk Indicator | Status | Comments |

|---|---|---|

| Revenue vs Profit Divergence | 🔴 | Revenue up 13%, but NPAT swung from $4M profit to ($12M) loss driven by finance costs and one-off debenture restructure. Underlying profitability questionable. |

| Capitalised R&D/Interest | ✅ | No large capitalisation of R&D; most intangible growth is goodwill from acquisitions. No major hidden costs observed. |

| Extraordinary Items | 🔴 | $7.2M extraordinary income write-back, improving EBITDA materially. This indicates reliance on non-recurring items. |

| Tax Rate Drop | ✅ | Effective tax benefit due to losses. No unexplained low tax rate. |

| Profit vs Cash Flow | 🟠 | OCF ($17.5M) materially below EBITDA ($33.3M), indicating large working capital/cost drag. |

| One-Off Gains Boosting Profit | 🔴 | Write-back of $7.2M provision plus revaluation gains; without these, EBITDA and NPAT would have been weaker. |

| Risk Indicator | Status | Comments |

|---|---|---|

| Auditor Changes | ✅ | Hall Chadwick continues as auditor. No recent changes disclosed. |

| Audit Qualifications | ✅ | Clean audit opinion. |

| Exec Departures | 🟠 | CEO change mid-strategy: Mohnish Kumar transitioned to Vice Chairman. No major rationale elaborated. |

| Transparency Issues | 🟠 | Extraordinary income and significant transaction impacts disclosed but diluted across notes; segment profitability clarity limited. |

| Board Weakness | ✅ | Board includes experienced finance professionals and independent directors. |

| Executive Pay Misalignment | 🔴 | Chairman remuneration jumped from $150k to $675k amid swinging to losses. Board remuneration >$1.4M while net loss increased. |

| Promotional Language | 🟠 | Repeated promotional claims (“transformative milestones,” “unparalleled financial access”) despite poor earnings. |

| Risk Indicator | Status | Comments |

|---|---|---|

| Chronic Unprofitability | 🟠 | FY25 loss was primarily transactional, but 3-year profitability track record inconsistent. Loss narrowing uncertain. |

| Revenue < Capex | 🟠 | ~$17M capex + ~$75M acquisitions vs $75M revenue; heavy reinvestment phase with unclear payback timelines. |

| Funding Dependency | 🔴 | Equity raises in FY25 ($40M placement + SPP), plus debt refinancing. Repeated external funding critical to operations. |

| Customer Concentration | 🟠 | Major contracts with State Bank of India, Union Bank, and Central Bank—customer concentration risk likely >50%. |

| Pre-commercial Product Risk | ✅ | Core business operational with revenue streams; no pure pre-commercial dependence. |

| Short Cash Runway | ✅ | Cash holdings sufficient for >12 months operations. |

| Regulatory/Compliance Exposure | 🟠 | Heavy reliance on RBI licences, acquisition integration risk. |

| Leadership Turnover During Expansion | 🟠 | CEO transitioned mid-expansion. Management continuity not fully explained. |

| Category | 🔴 Red Flags | 🟠 Amber Flags |

|---|---|---|

| Balance Sheet | 2 | 2 |

| Income Statement | 3 | 1 |

| Governance / Disclosure | 1 | 3 |

| Strategic Risk Factors | 1 | 4 |

🔴 Total Red Flags: 7

🟠 Total Amber Flags: 10

🔴 High Borrowings: Debt-to-equity approaching 2x with finance costs tripling.

🔴 Extraordinary Items & One-off Gains: $7.2M non-recurring write-back and revaluations masked underlying losses.

🔴 Executive Pay Misalignment: Chairman and board fees rose sharply during a swing to losses.

🔴 Funding Dependency: Equity raises and debenture restructuring are critical to liquidity.

🔴 Revenue vs Profit Divergence: Revenue rose while NPAT fell into loss.

🔴 One-Off Gains Boosting Profit: Extraordinary income contributed materially to reported EBITDA.

🟠 Idle Cash: Large cash holdings without clear disclosure of return strategy.

🟠 OCF vs EBITDA: Cash flow lagged EBITDA significantly.

🟠 Transparency: Disclosures of transaction impacts fragmented across notes.

🟠 Leadership Turnover: CEO transitioned during major expansion.

🟠 Customer Concentration: Dependence on large public sector banks.

🟠 Capex vs Revenue: Heavy investment relative to annual turnover.

🟠 Chronic Unprofitability: Inconsistent profitability trend.

🟠 Regulatory Exposure: Reliant on RBI licences, regulatory compliance critical.

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Forensic Analysis: Findi ASX:FND

This content is restricted to Supporters. Please Sign In.

Not a member? Follow the for a Free 14 Day Trial (no credit card required).

June, 2025

June, 2025

Website: http://bigriverindustries.com.au/

Website: http://bigriverindustries.com.au/

The technical picture for Big River has turned positive in recent months.

I asked A.I. if there were any signs of a turnaround occurring in this company, based on the most recent half-year report (released in February). This was the response I received:

From the report, here are the positive or potentially improving indicators worth noting:

These are early, tentative signs. The structural risks remain significant:

Yes—there are signs that trading conditions may be stabilising, and the worst earnings pressure could be past. But it’s too early to say a sustained turnaround is underway. I would monitor the next 1–2 quarters very closely for:

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Big River Industries: Turnaround Potential?

📅 June, 2025

🌐 Website: http://bigriverindustries.com.au/

Here is a forensic financial analysis of Big River Industries (ASX:BRI), based on its Half-Yearly Report for the period ended 31 December 2024.

| Risk Indicator | Status | Comments |

|---|---|---|

| Goodwill >25% of Assets | 🔴 | Goodwill of $33m vs total assets of $235.6m (~14%) but note prior goodwill was ~$53m with a $20m impairment this period. High risk due to repeated write-downs. |

| Rising Receivables Days | 🔴 | Receivables fell from $56m to $44m in 6 months while revenue fell 3%; however, high impairment charges ($0.7m) suggest collectability concerns. |

| Inventory Growth vs Profit | 🔴 | Inventories remain flat (~$71m) while profit has swung to a $17m loss. |

| High Borrowings | 🔴 | Debt of $46m with net tangible assets ~$55m; debt to equity >0.9, and large debt relative to equity. |

| Loans to Related Parties | ✅ | No evidence of related party loans. |

| Idle Cash | 🟠 | Cash declined from $20.5m to $18.8m; not excessive but limited liquidity relative to debt. |

| Risk Indicator | Status | Comments |

|---|---|---|

| Revenue vs Profit Divergence | 🔴 | Revenue fell 3% but profit declined over 300% (from +$7m to -$17m) due to impairment. |

| Capitalised R&D/Interest | ✅ | No material new capitalised R&D or significant trend. |

| Extraordinary Items | 🔴 | $20m impairment of goodwill and $0.5m restructuring costs materially impact profit. |

| Tax Rate Drop | ✅ | Effective tax rate is consistent (~30% nominal). |

| Profit vs Cash Flow | 🟠 | Cash flow from operations positive ($9m) despite net loss due to non-cash charges. |

| One-Off Gains Boosting Profit | ✅ | No gains offsetting the loss. |

| Risk Indicator | Status | Comments |

|---|---|---|

| Auditor Changes | ✅ | No change in auditor (BDO). |

| Audit Qualifications | ✅ | No qualifications reported. |

| Exec Departures | ✅ | No disclosed executive departures. |

| Transparency Issues | 🟠 | Limited disclosure around impairment triggers and expected recovery. |

| Board Weakness | ✅ | Board appears independent. |

| Executive Pay Misalignment | 🟠 | Interim dividend maintained despite major loss. |

| Promotional Language | 🟠 | Optimistic commentary on market “stabilisation” despite substantial impairment and losses. |

| Risk Indicator | Status | Comments |

|---|---|---|

| Chronic Unprofitability | 🟠 | Significant loss this period but prior profitability. Watch for trend continuation. |

| Revenue < Capex | ✅ | No evidence capex exceeds revenue. |

| Funding Dependency | 🟠 | Debt remains high and contingent consideration obligations ($2.4m) still exist. |

| Customer Concentration | ✅ | No disclosed concentration risk. |

| Pre-commercial Product Risk | ✅ | Core operations are established products. |

| Short Cash Runway | 🟠 | ~$19m cash with ~$7m lease liabilities due in <12 months; runway likely <18 months if losses continue. |

| Regulatory/Compliance Exposure | ✅ | No regulatory issues disclosed. |

| Leadership Turnover During Expansion | ✅ | No turnover disclosed. |

| Category | 🔴 Red Flags | 🟠 Amber Flags |

|---|---|---|

| Balance Sheet | 4 | 1 |

| Income Statement | 3 | 1 |

| Governance / Disclosure | 0 | 3 |

| Strategic Risk Factors | 0 | 3 |

🔴 Total Red Flags: 7

🟠 Total Amber Flags: 8

Balance Sheet: Multiple red flags—inventory not reducing despite losses, significant impairment of goodwill, high borrowings relative to equity.

Income Statement: Large divergence between revenue and profit, extraordinary non-cash items driving losses.

Governance: Amber concerns around maintaining dividends despite losses and promotional commentary.

Strategic Risk: Cash runway under pressure and reliance on debt facilities.

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Forensic Analysis: Big River Industries ASX:BRI

📅 June, 2025

🌐 Website: www.catapult.com

Here is a forensic financial analysis of Catapult (ASX:CAT), based on its FY25 Annual Report.

| Risk Indicator | Status | Comments |

|---|---|---|

| Goodwill >25% of Assets | ✅ | No explicit disclosure indicating goodwill dominance; likely under threshold given SaaS model and modest acquisition activity. |

| Rising Receivables Days | 🟠 | Receivables growth implied by ACV and revenue growth; no explicit receivables days trend disclosed—warrants monitoring as revenue expands rapidly. |

| Inventory Growth vs Profit | Not Applicable | SaaS business—minimal inventories, but capital equipment sales (~6% of revenue) could create deferred recognition risk. |

| High Borrowings | ✅ | Debt reduced significantly to $3.5M (from $11M), net cash position of ~$7M. Low leverage. |

| Loans to Related Parties | ✅ | No evidence of related party loans disclosed. |

| Idle Cash | ✅ | Cash position adequate ($10.7M) and reducing borrowings—no indication of hoarding. |

| Risk Indicator | Status | Comments |

|---|---|---|

| Revenue vs Profit Divergence | 🟠 | Revenue +16.5%, Management EBITDA margin improved to 12.7%, but still net loss ($8.8M). Improving trend but not fully profitable at statutory level. |

| Capitalised R&D/Interest | 🔴 | Significant capitalised development: $16.7M (~14% of revenue). This is material and flat YoY, supporting profit margins—requires close scrutiny. |

| Extraordinary Items | ✅ | No recurring extraordinary items disclosed. |

| Tax Rate Drop | ✅ | Loss-making entity—no abnormal tax benefits disclosed. |

| Profit vs Cash Flow | ✅ | Free Cash Flow improved materially to +$8.6M from +$4.6M. Cash flow moving positive. |

| One-Off Gains Boosting Profit | ✅ | No asset revaluations or disposals used to boost earnings. |

| Risk Indicator | Status | Comments |

|---|---|---|

| Auditor Changes | ✅ | No auditor changes reported. |

| Audit Qualifications | ✅ | No qualifications noted in the audit opinion. |

| Exec Departures | ✅ | Stable leadership, no major CEO/CFO turnover. |

| Transparency Issues | 🟠 | Heavy reliance on non-IFRS metrics (Management EBITDA, ACV). Clear definitions provided but high non-IFRS usage warrants caution. |

| Board Weakness | ✅ | Board appears experienced, no independence concerns noted. |

| Executive Pay Misalignment | 🟠 | Share-based payments remain material ($12.5M), dilutive incentives persist despite statutory losses. |

| Promotional Language | 🟠 | Marketing-heavy language (“unleash potential,” “category-defining”)—some caution on optimism bias. |

| Risk Indicator | Status | Comments |

|---|---|---|

| Chronic Unprofitability | 🟠 | Still net loss-making, but trend improving with positive FCF. |

| Revenue < Capex | ✅ | Capex mainly R&D; total capex not exceeding revenue. |

| Funding Dependency | ✅ | No new equity raises disclosed in FY25; reduced borrowings. |

| Customer Concentration | ✅ | No material concentration disclosed. |

| Pre-commercial Product Risk | ✅ | Core products commercialised and scaling. |

| Short Cash Runway | ✅ | Net cash positive; free cash flow positive; no immediate runway concerns. |

| Regulatory/Compliance Exposure | 🟠 | Trademark litigation with Adidas in the US—stated immaterial but worth monitoring. |

| Leadership Turnover During Expansion | ✅ | No turnover reported during scaling period. |

| Category | 🔴 Red Flags | 🟠 Amber Flags |

|---|---|---|

| Balance Sheet | 0 | 1 |

| Income Statement | 1 | 1 |

| Governance / Disclosure | 0 | 3 |

| Strategic Risk Factors | 0 | 2 |

🔴 Total Red Flags: 1

🟠 Total Amber Flags: 7

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Forensic Analysis: Catapult ASX:CAT

📅 June, 2025

🌐 Website: https://www.sks.com.au

Here is a forensic financial analysis of SKS Technologies (ASX:SKS), based on its FY24 Annual Report, 1H25 Interim Results Presentation, and the May 2025 announcement of a $100 million data centre contract.

| Risk Indicator | Status | Comments |

|---|---|---|

| Goodwill >25% of Assets | ✅ | No indication of excessive goodwill; balance sheet primarily reflects tangible expansion |

| Rising Receivables Days | ✅ | Working capital usage rose slightly due to growth, but receivables remained controlled and cash conversion was solid |

| Inventory Growth vs Profit | Not Applicable | Service-based business with limited inventory exposure |

| High Borrowings | ✅ | No long-term debt; increased use of short-term facilities remains proportionate and manageable |

| Loans to Related Parties | ✅ | No such transactions noted |

| Idle Cash | ✅ | Cash used effectively for operations and M&A; no signs of hoarding |

| Risk Indicator | Status | Comments |

| Revenue vs Profit Divergence | ✅ | Revenue and EBITDA up YoY; NPAT impacted by project timing and cost adjustments but still positive |

| Capitalised R&D/Interest | ✅ | No aggressive capitalisation observed |

| Extraordinary Items | ✅ | Interim results reflect operational performance; no major one-offs identified |

| Tax Rate Drop | ✅ | No abnormal tax reduction noted in interim figures |

| Profit vs Cash Flow | ✅ | Operating cash flow strong despite modest NPAT, indicating earnings quality is sustained |

| One-Off Gains Boosting Profit | ✅ | No signs of non-operating gains inflating interim profit |

| Risk Indicator | Status | Comments |

| Auditor Changes | ✅ | No recent changes; consistent auditor retained through interim period |

| Audit Qualifications | ✅ | No qualifications noted in audit/review of interim financials |

| Exec Departures | ✅ | Leadership remained stable through H1 FY25 |

| Transparency Issues | ✅ | Continued clear disclosure of segment and performance data in interim release |

| Board Weakness | ✅ | Board composition unchanged and retains relevant expertise |

| Executive Pay Misalignment | ✅ | No material changes to pay noted during the interim period |

| Promotional Language | 🟠 | Some optimistic tone in outlook commentary, generally substantiated by ongoing growth |

| Risk Indicator | Status | Comments |

| Chronic Unprofitability | ✅ | Company remains profitable at NPAT and EBITDA levels in 1H25 despite some margin compression |

| Revenue < Capex | ✅ | Capex remains proportionate to revenue and growth plans |

| Funding Dependency | ✅ | No new equity raised; facilities extended prudently to support scaling |

| Customer Concentration | 🟠 | Data centres still account for ~60% of secured work, reinforced by new $100M contract; strategic diversification continues |

| Pre-commercial Product Risk | ✅ | All offerings are revenue-generating and commercially deployed |

| Short Cash Runway | ✅ | Sufficient facilities and cash flow to support near-term needs; new contract to be funded from existing resources |

| Regulatory/Compliance Exposure | ✅ | No compliance issues or regulatory red flags raised in interim period |

| Leadership Turnover During Expansion | ✅ | Management remained stable through strategic execution |

| Category | 🔴 Red Flags | 🟠 Amber Flags |

| Balance Sheet | 0 | 0 |

| Income Statement | 0 | 0 |

| Governance / Disclosure | 0 | 1 |

| Strategic Risk Factors | 0 | 1 |

🔴 Total Red Flags: 0

🟠 Total Amber Flags: 2

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Forensic Analysis: SKS Technologies ASX:SKS

📅 June, 2025

🌐 Website: www.cogstate.com

Here is a forensic financial analysis of Cogstate (ASX:CGS), based on its Half-Year Report for the period ended 31 December 2024, and the FY25 guidance update released on 24 June 2025.

| Risk Indicator | Status | Comments |

|---|---|---|

| Goodwill >25% of Assets | ✅ | No goodwill recorded; all intangibles are internally developed IP and software |

| Rising Receivables Days | ✅ | Receivables stable YoY (~US$10M) despite 19% revenue growth |

| Inventory Growth vs Profit | 🟠 Not Applicable | Company operates a services model without physical inventory |

| High Borrowings | ✅ | No borrowings recorded; debt-free status maintained |

| Loans to Related Parties | ✅ | No related party loans disclosed |

| Idle Cash | ✅ | High cash holdings (US$34.2M) are being actively deployed through an ongoing share buy-back program |

| Risk Indicator | Status | Comments |

|---|---|---|

| Revenue vs Profit Divergence | ✅ | Revenue up 19%, NPAT up 95% — positive operating leverage |

| Capitalised R&D/Interest | 🟠 | Capitalised software dev costs of US$655K (~5% of opex); rising trend should be monitored |

| Extraordinary Items | ✅ | No material one-offs or adjustments reported |

| Tax Rate Drop | 🔴 | Effective tax rate fell to 25% from 96% YoY due to prior year deferred tax adjustments |

| Profit vs Cash Flow | ✅ | OCF US$5.0M vs NPAT US$3.9M — strong cash conversion |

| One-Off Gains Boosting Profit | ✅ | No asset sales or revaluation gains boosting profit reported |

| Risk Indicator | Status | Comments |

|---|---|---|

| Auditor Changes | ✅ | Auditor (Pitcher Partners) unchanged |

| Audit Qualifications | ✅ | Clean review report with no qualifications |

| Exec Departures | ✅ | No senior executive or board departures reported |

| Transparency Issues | ✅ | Strong disclosure across segments and revenue categories |

| Board Weakness | ✅ | Board comprises experienced professionals with sectoral and governance expertise |

| Executive Pay Misalignment | ✅ | No material pay rises; buy-backs and profitability suggest aligned incentives |

| Promotional Language | ✅ | Tone of reporting is factual and grounded in operating data |

| Risk Indicator | Status | Comments |

|---|---|---|

| Chronic Unprofitability | ✅ | Company remains consistently profitable with strong YoY improvement |

| Revenue < Capex | ✅ | Revenue (US$23.9M in 1H25) substantially exceeds capex (US$655K + PPE) |

| Funding Dependency | ✅ | No new equity raised; company returning capital via buy-backs |

| Customer Concentration | 🟠 | Eisai remains a significant revenue source, especially in Healthcare |

| Pre-commercial Product Risk | ✅ | Revenue-generating segments are commercialised |

| Short Cash Runway | ✅ | Cash reserves (US$34.2M) and positive cash flow eliminate short-term funding risk |

| Regulatory/Compliance Exposure | ✅ | No regulatory or compliance breaches reported |

| Leadership Turnover During Expansion | ✅ | Stable leadership during revenue acceleration and segment expansion |

| Category | 🔴 Red Flags | 🟠 Amber Flags |

|---|---|---|

| Balance Sheet | 0 | 0 |

| Income Statement | 1 | 1 |

| Governance / Disclosure | 0 | 0 |

| Strategic Risk Factors | 0 | 1 |

🔴 Total Red Flags: 1

🟠 Total Amber Flags: 2

🔴 Tax Rate Drop: Effective tax rate fell materially from prior period (96% to 25%), with no detailed commentary provided.

🟠 Capitalised R&D: Ongoing capitalisation of development costs suggests rising reliance on deferred expensing.

🟠 Customer Concentration: Eisai continues to contribute a significant portion of Healthcare revenue, posing concentration risk.

As of 24 June 2025, Cogstate upgraded full-year guidance:

FY25 Revenue forecast: US$52–54M (+20–24% YoY)

FY25 Profit Before Tax forecast: US$12–14M (+69–97% YoY)

This reinforces operational strength and reduces future financial risk. If realised, these figures would materially enhance margin quality and further validate the capital return strategy.

Disclaimer: This report is for educational purposes and does not constitute financial advice. It does not account for personal circumstances. All investors should conduct their own research or consult a qualified adviser before making financial decisions.

Forensic Analysis: Cogstate ASX:CGS

🗓 June, 2025

🌐 Website: www.collinsfoods.com

Here is a forensic financial analysis of Collins Foods (ASX:CKF), based on its Appendix 4E and 2025 Annual Report for the year ended 27 April 2025.

| Risk Indicator | Status | Comments |

|---|---|---|

| Goodwill >25% of Assets | ✅ | Not flagged in summary; likely below material threshold. |

| Rising Receivables Days | ✅ | No evidence of adverse receivables movement or commentary on deterioration. |

| Inventory Growth vs Profit | 🔹 Not Applicable | Inventory commentary not disclosed; restaurant model limits relevance. |

| High Borrowings | ✅ | Net debt fell to $137.9M with leverage ratio down to 0.93 from 1.07. |

| Loans to Related Parties | ✅ | No indication of such transactions. |

| Idle Cash | ✅ | Cash deployed toward growth and dividend; not excessive idle cash noted. |

| Risk Indicator | Status | Comments |

| Revenue vs Profit Divergence | 🔴 | Revenue up 2.1%, but statutory NPAT plunged 88.5% to $8.8M. |

| Capitalised R&D/Interest | ✅ | No evidence of aggressive capitalisation. |

| Extraordinary Items | 🔴 | $42.3M in non-trading items (impairments, compliance provisions). |

| Tax Rate Drop | ✅ | Effective tax rate stable YoY. |

| Profit vs Cash Flow | ✅ | Operating cash flow ($181.4M) well above NPAT; strong conversion. |

| One-Off Gains Boosting Profit | ✅ | No abnormal gains in FY25 (FY24 included Sizzler Asia sale). |

| Risk Indicator | Status | Comments |

| Auditor Changes | ✅ | No change noted. |

| Audit Qualifications | ✅ | Clean audit opinion. |

| Exec Departures | 🔶 | CEO turnover in FY25 with handover to new MD; managed transition. |

| Transparency Issues | ✅ | Clear disclosures, especially on impairments and provisions. |

| Board Weakness | ✅ | Experienced, diversified board with relevant industry expertise. |

| Executive Pay Misalignment | 🔶 | STI forfeited due to low NPAT; LTI vesting tied to performance. |

| Promotional Language | 🔶 | Optimistic tone present, but balanced with discussion of challenges. |

| Risk Indicator | Status | Comments |

| Chronic Unprofitability | ✅ | Underlying NPAT $51.1M; not chronically unprofitable. |

| Revenue < Capex | ✅ | Capex and expansion aligned to revenue scale. |

| Funding Dependency | ✅ | No equity raises in FY25; debt reduction evident. |

| Customer Concentration | ✅ | QSR model, diversified locations; no concentration risk noted. |

| Pre-commercial Product Risk | ✅ | Fully commercial model. |

| Short Cash Runway | ✅ | Strong operating cash flow and reduced leverage. |

| Regulatory/Compliance Exposure | 🔶 | Wage compliance issue noted, under remediation with regulator. |

| Leadership Turnover During Expansion | 🔶 | CEO handover during strategy reset and Taco Bell exit. |

| Category | 🔴 Red Flags | 🔶 Amber Flags |

| Balance Sheet | 0 | 0 |

| Income Statement | 2 | 0 |

| Governance / Disclosure | 0 | 3 |

| Strategic Risk Factors | 0 | 2 |

🔴 Total Red Flags: 2

🔶 Total Amber Flags: 5

Disclaimer: This report is for educational purposes and does not constitute financial advice. It does not account for personal circumstances. All investors should conduct their own research or consult a qualified adviser before making financial decisions.

Forensic Analysis: Collins Foods ASX:CKF

📅 June, 2025

🌐 Website: https://www.xero.com/

Here is a forensic financial analysis of Xero (ASX:XRO), based on its FY25 Annual Report (Appendix 4E).

| Risk Indicator | Status | Comments |

|---|---|---|

| Goodwill >25% of Assets | ✅ | Goodwill is present but remains under 25% of total assets. |

| Rising Receivables Days | ✅ | Receivables growth is aligned with revenue growth. |

| Inventory Growth vs Profit | Not Applicable | Not relevant for Xero’s SaaS model. |

| High Borrowings | ✅ | Net cash position reported with no major debt burden. |

| Loans to Related Parties | ✅ | No related party loans disclosed. |

| Idle Cash | ✅ | Cash is deployed towards R&D, acquisitions, and growth. No hoarding observed. |

| Risk Indicator | Status | Comments |

|---|---|---|

| Revenue vs Profit Divergence | ✅ | Revenue and net profit both grew in FY25. Operating leverage appears improving. |

| Capitalised R&D/Interest | 🟠 | Capitalised development costs increased. While common in SaaS, trend should be watched. |

| Extraordinary Items | ✅ | No major one-off items affecting earnings. |

| Tax Rate Drop | ✅ | Effective tax rate remained stable. |

| Profit vs Cash Flow | ✅ | Strong operating cash flow aligns with reported net income. |

| One-Off Gains Boosting Profit | ✅ | No material gains distorting the result. |

| Risk Indicator | Status | Comments |

|---|---|---|

| Auditor Changes | ✅ | No recent changes in auditor. |

| Audit Qualifications | ✅ | Clean audit opinion. |

| Exec Departures | 🟠 | Some senior leadership turnover post-strategy shift. |

| Transparency Issues | ✅ | Clear segment reporting and cost breakdowns. |

| Board Weakness | ✅ | Independent board with tech and financial expertise. |

| Executive Pay Misalignment | ✅ | Remuneration structure aligned with performance and shareholder value creation. |

| Promotional Language | ✅ | Report maintains a measured tone with data-supported claims. |

| Risk Indicator | Status | Comments |

|---|---|---|

| Chronic Unprofitability | ✅ | The company has turned the corner with consistent net profit in FY25. |

| Revenue < Capex | ✅ | Revenue well exceeds capex; strong commercial traction. |

| Funding Dependency | ✅ | No capital raises; cash flow supports operations. |

| Customer Concentration | ✅ | Revenue diversified across geographies and customer bases. |

| Pre-commercial Product Risk | ✅ | Core platform is commercial; no major speculative product risk. |

| Short Cash Runway | ✅ | Strong balance sheet and operating cash flow provide a healthy runway. |

| Regulatory/Compliance Exposure | ✅ | No adverse findings or regulatory actions noted. |

| Leadership Turnover During Expansion | 🟠 | Executive turnover occurred amid product expansion and AI strategy rollout. |

| Category | 🔴 Red Flags | 🟠 Amber Flags |

|---|---|---|

| Balance Sheet | 0 | 0 |

| Income Statement | 0 | 1 |

| Governance / Disclosure | 0 | 1 |

| Strategic Risk Factors | 0 | 1 |

🔴 Total Red Flags: 0

🟠 Total Amber Flags: 3

🟠 Executive turnover: Key changes following new strategic priorities and AI focus.

🟠 Leadership change during expansion: Timing may impact continuity if not well-managed.

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Forensic Analysis: Xero ASX:XRO

This content is restricted to Supporters. Please Sign In.

Not a member? Follow the for a Free 14 Day Trial (no credit card required).

This content is restricted to Supporters. Please Sign In.

Not a member? Follow the for a Free 14 Day Trial (no credit card required).

This content is restricted to Supporters. Please Sign In.

Not a member? Follow the for a Free 14 Day Trial (no credit card required).

This content is restricted to Supporters. Please Sign In.

Not a member? Follow the for a Free 14 Day Trial (no credit card required).

This content is restricted to Supporters. Please Sign In.

Not a member? Follow the for a Free 14 Day Trial (no credit card required).

This content is restricted to Supporters. Please Sign In.

Not a member? Follow the for a Free 14 Day Trial (no credit card required).

June 16, 2025

June 16, 2025

Website: https://www.superloop.com

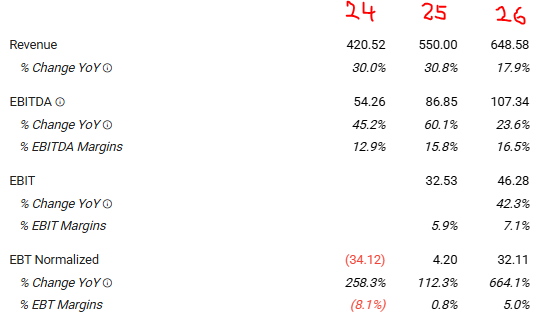

I asked AI to analyse the first half report of Superloop ASX:SLC and assess whether they were likely to reach, exceed or fall short of current analyst estimates. This was the result:

Based on the provided financial estimates and the interim results for Superloop for the six months ended 31 December 2024, here’s an assessment of how the company is tracking against analyst forecasts:

Revenue

FY24A: $420.5M

FY25E: $550M (YoY +30.8%)

FY24 1H actual: $257.5M (YoY +33.3%)

✅ On Track: With $257.5M revenue in 1H25, Superloop is on pace to meet or slightly exceed the $550M FY25 target, assuming H2 performance remains strong.

EBITDA

FY24A: $54.3M

FY25E: $86.9M (YoY +60.1%)

EBITDA margin FY24A: 12.9%

1H25 GM: $87.9M; OPEX: $63.6M → Est. 1H25 EBITDA ≈ $24.3M

⚠️ Slight Lag: 1H EBITDA is ~28% of the FY target. To hit $86.9M, H2 must deliver >$60M EBITDA—ambitious but potentially feasible with expected margin expansion from Origin customer base.

EBT (Normalized)

FY24A: -$34.1M

FY25E: $4.2M

1H25: EBT = -$17.0M

🟥 Behind Schedule: While significantly improved YoY, a $17M 1H loss means Superloop needs a sharp profitability swing in H2 to break even on a normalized basis.

1. Operating Cash Flow

1H25: $30.6M

1H24: $23.7M

✅ Positive and Improved: Operating cash flows rose 29%, indicating better cash efficiency, despite higher marketing and transaction costs.

2. EBT Comparison

1H25 EBT: -$17.0M

1H24 EBT: -$22.4M

Improvement: $5.4M (~24%)

✅ Improving Trend: Still negative, but significantly improved YoY.

Customer Growth: +209K (up 46%), led by the Origin Energy transition.

Gross Margin: $87.9M (YoY +28%) — strong margin contribution from Consumer and Wholesale segments.

Balance Sheet: $55.9M cash vs $56.0M debt; modest leverage, and revolving credit facility with $52.1M capacity still available.

Trajectory Assessment:

Revenue: On or slightly above track.

EBITDA: Slightly behind, but attainable with H2 cost discipline and margin expansion.

EBT: Most challenging—requires a strong swing into profitability in H2.

Verdict: Analysts appear realistically optimistic. The company is broadly on track with revenue and has made major strides in cost leverage. However, achieving EBITDA and especially EBT targets will require exceptional execution in H2 FY25.

Let me know if you’d like a revised financial forecast based on current run-rate and margin assumptions.

I then uploaded an announcement released to the market since the half-year report that would appear to me to provide more clues as to how they are progressing. I asked the AI if this announcement strengthened or weakened the above thesis:

The announcement of Superloop reaching Milestone 3 of the Origin Energy contract—with over 200,000 Origin broadband subscribers now migrated to Superloop’s network as of 13 May 2025—strengthens the outlook provided in the interim report.

Impact on Revenue & EBITDA

This milestone confirms the full migration of the Origin customer base, which was already underway in 1H25.

With 200,000+ Origin subscribers now active, the full run-rate revenue and margin benefits will be realized in H2 FY25, providing a meaningful uplift to both revenue and EBITDA.

✅ Revenue: Supports the view that FY25 revenue of $550M is achievable or beatable.

✅ EBITDA: Strengthens the case for a strong H2 margin contribution. Assuming favorable gross margins from this cohort, Superloop is in a better position to approach the $86.9M target—though execution and cost discipline remain key.

🟥 EBT: The milestone alone doesn’t guarantee EBT breakeven, but it materially enhances operating leverage, improving the probability of a positive swing.

This milestone reinforces the bullish thesis. It doesn’t change the core narrative but adds confidence to revenue and EBITDA projections, especially for H2 FY25. If cost trends remain controlled, this could help Superloop exceed EBITDA targets and close the gap on positive earnings before tax.

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Pre-Results Analysis: Superloop

June 15, 2025

Most companies report their annual results in August which is still some way away. However, we have already seen some stocks update the market as to how they are tracking relative to market and their own expectations. Let’s have a look at some of the key announcements since the start of June:

Ticker: NXT | Sector: Technology | Industry: Information Technology Services | Website: https://www.nextdc.com

| Aspect | Assessment |

|---|---|

| Tone | Strongly positive |

| Operational Outlook | Upgrade |

| Magnitude | Material (7% uplift in ~1 month) |

| Strategic Implication | Very constructive – signals execution strength and rising AI demand |

This update is a clear operational upgrade and signals growing demand for NEXTDC’s AI-optimised data infrastructure. While the financial uplift won’t be felt immediately (with FY27–FY28 impact), the contracted utilisation jump and record order book point to substantial medium-term growth. It strengthens the investment case and underlines NEXTDC’s execution capabilities and positioning in a structurally growing sector.

Ticker: ZIP | Sector: Financial Services | Industry: Credit Services | Website: https://zip.co/au

| Aspect | Assessment |

|---|---|

| Tone | Strongly positive |

| Earnings Outlook | Upgrade |

| Magnitude | Moderate (~4.6%) |

| Strategic Implication | Constructive – validates growth strategy, especially in the US |

This is a clear and confidence-boosting upgrade. The improvement in cash EBTDA guidance—while modest in percentage terms—builds on a strong US performance and confirms sustained momentum. Zip is executing well on both growth and risk fronts, and the ongoing buyback program reinforces management’s confidence. This update should be viewed as positively reinforcing the investment case, especially for those tracking Zip’s turnaround and US expansion story.

Ticker: MTS | Sector: Consumer Defensive | Industry: Food Distribution | Website: https://www.metcash.com

| Aspect | Assessment |

|---|---|

| Tone | Positive |

| Earnings Outlook | Slight upgrade |

| Magnitude | Minor (~0.4–1.8%) |

| Strategic Implication | Constructive for long-term growth, particularly in Hardware |

This update should be viewed as incrementally positive. While the earnings upgrade is small, it reinforces stability in a tough environment and demonstrates strategic discipline. The Hardware division realignment signals intent to scale and streamline, which could support better margins and returns over time.

Ticker: LGL | Sector: Consumer Defensive | Industry: Farm Products | Website: https://www.lynchgroup.com.au

| Aspect | Assessment |

|---|---|

| Tone | Positive |

| Earnings Outlook | Reaffirmed / Slightly Up |

| Magnitude | Moderate growth (~7% revenue, stronger China EBITDA) |

| Strategic Implication | Sound execution across both geographies with upside emerging in China |

This is a positive update. Both Australian and Chinese operations are delivering well, with China showing signs of margin and revenue recovery. Despite minor weather-related disruptions, the group remains on track for solid growth, with no surprises in guidance and execution clearly improving. The business appears to be navigating global uncertainty effectively, and the outlook is constructively optimistic.

Ticker: MGH | Sector: Industrials | Industry: Engineering & Construction | Website: https://www.maasgroup.com.au

| Aspect | Assessment |

|---|---|

| Tone | Constructively positive |

| Earnings Outlook | Reaffirmed (neutral) |

| Magnitude | N/A |

| Strategic Implication | Positive – confirms long-term direction and progress in core segment |

This update should be viewed as strategically positive but financially neutral. There’s no upgrade to earnings guidance, but confidence is reinforced through the reaffirmation of FY25 EBITDA and asset sale targets. MGH’s continued simplification toward a quarry-led, vertically integrated Construction Materials model aligns well with macro trends and positions the business for long-term growth. Investors looking for a steady compounder with solid infrastructure exposure will see this as a well-executed continuation of strategy.

Ticker: ASX | Sector: Financial Services | Industry: Financial Data & Stock Exchanges | Website: https://www.asx.com.au

| Aspect | Assessment |

|---|---|

| Tone | Neutral to mildly positive |

| Earnings Outlook | No change (guidance confirmed) |

| Magnitude | N/A (no upgrade/downgrade) |

| Strategic Implication | Mixed — good cost control but higher FY26 expenses offset gains |

This update is strategically positive but financially neutral. ASX reconfirms existing FY25 guidance, showing disciplined expense and capex control. However, rising costs in FY26—driven by regulatory and tech factors—could weigh on margins in the short term. The introduction of EBITDA margin as a key performance metric signals greater financial focus, while long-term tech upgrades (e.g. CHESS) show strategic alignment. Investors should view this as steady progress, but not a near-term upgrade or downgrade to the financial outlook.

Ticker: COH | Sector: Healthcare | Industry: Medical Devices | Website: https://www.cochlear.com

| Aspect | Assessment |

|---|---|

| Tone | Cautiously negative |

| Earnings Outlook | Downgrade |

| Magnitude | Moderate (~7–9%) |

| Strategic Implication | Product cycle transition; FY26 improvement possible |

This is a moderate earnings downgrade, reflecting weaker-than-expected Services revenue and a soft patch in developed markets. While implant volumes are growing, profitability is being dented by lower-margin mix and modest share loss.

The tone is measured but realistic, with Cochlear pointing to product upgrades and FY26 recovery as catalysts. For now, however, investors will likely view this as a short-term disappointment during a mid-cycle transition.

Ticker: AX1 | Sector: Consumer Cyclical | Industry: Apparel Retail | Website: https://www.accentgr.com.au

| Aspect | Assessment |

|---|---|

| Tone | Cautious / negative |

| Earnings Outlook | Downgrade implied |

| Magnitude | Mild (~2%–5% EBIT decline) |

| Strategic Implication | Suggests margin pressure, soft consumer conditions |

This is a mild downgrade and should be viewed as modestly negative. While the decline in EBIT is not dramatic, the deterioration in like-for-like sales and margin compression points to a weak retail trading environment. Management commentary focuses on discipline rather than opportunity, and there is no suggestion of near-term improvement. Unless the macro or consumer backdrop improves quickly, FY26 could face similar pressures.

Ticker: CTT | Sector: Consumer Cyclical | Industry: Luxury Goods | Website: https://www.cettireinvestors.com

| Aspect | Assessment |

|---|---|

| Tone | Cautious to mildly negative |

| Earnings Outlook | Downgrade implied |

| Magnitude | Mild – near-breakeven EBITDA, with FX impact |

| Strategic Implication | Management focused on margin discipline and geographic diversification |

This update is best viewed as a mild downgrade. While headline sales are up slightly, margin pressures and weak US demand have pushed profitability to near-zero levels. The company’s strategic pivot to Emerging Markets and operational cost discipline are appropriate responses, but execution risk remains high in a volatile environment. Investors should interpret this update as defensive in tone, with Cettire signaling caution rather than growth in the near term.

Ticker: IEL | Sector: Consumer Defensive | Industry: Education & Training Services | Website: https://www.idp.com

| Aspect | Assessment |

|---|---|

| Tone | Cautious to negative |

| Earnings Outlook | Clear downgrade |

| Magnitude | Material (~20%–27% EBIT drop) |

| Strategic Implication | Defensive positioning; navigating long-term disruption |

This is a clear and material downgrade. Volume drops of nearly 30% in Student Placement and 20% in Language Testing reflect a deeply challenged global environment for international education. While IDP is taking appropriate defensive actions (cost control, strategic review), it cannot offset the sector-wide contraction driven by shifting government policies.

Investors should view this as a significant near-term setback with ongoing headwinds into FY26, though the company’s scale, balance sheet, and positioning leave it well placed for long-term recovery — if and when market conditions stabilise.

Ticker ANG | Sector: Industrials | Industry: Farm & Heavy Construction Machinery | Website: https://www.austineng.com

| Aspect | Assessment |

|---|---|

| Tone | Mixed (positive revenue, negative margin) |

| Earnings Outlook | Downgrade (EBIT) |

| Magnitude | Moderate (~18% EBIT downgrade from prior guidance) |

| Strategic Implication | Still constructive – underlying business demand is strong, but margin execution must improve |

This update is mixed — a clear revenue upgrade driven by strong demand and operational expansion, offset by a moderate earnings downgrade due to underperformance in Chile. Management is acting decisively by reallocating production to relieve capacity constraints and protect margins in the future.

For investors, this should be interpreted as short-term pain for long-term gain, with solid revenue momentum and a growing order book suggesting the underlying demand trend remains very strong.

| Theme | Description |

|---|---|

| AI Infrastructure Boom | NEXTDC’s performance reflects strong AI-related capex demand |

| US Exposure = Upside | ZIP’s update shows the benefit of operating in a healthier US economy |

| Consumer Bifurcation | Strong demand for essentials (Lynch), weaker for discretionary (Accent) |

| Margin Pressure Broadening | Across sectors, rising costs and lower volumes are squeezing profitability |

| Execution Risk is Real | Even in growing markets, missteps (Austin, Cochlear) can damage earnings |

| Policy Overhang | IDP’s outlook highlights how regulatory changes can derail even strong franchises |

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Pre-Earnings Season: Early Indications