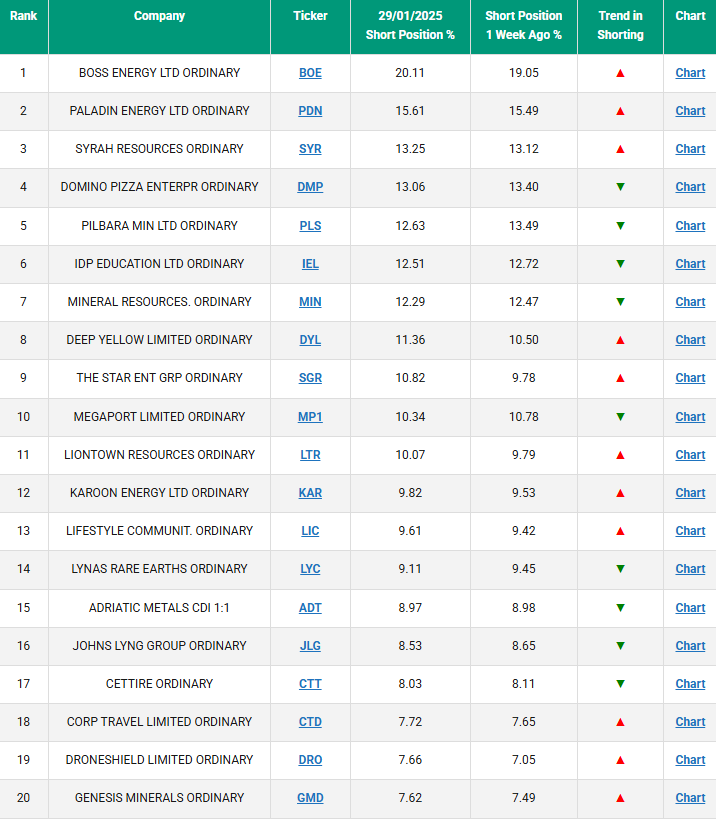

The top 20 ASX companies with the highest short-sold positions:

Source: https://stocksunderthehood.com/asx-most-shorted-stocks/

Let’s examine why a significant percentage of these companies’ shares are being shorted, indicating that traders are betting on their share prices falling.

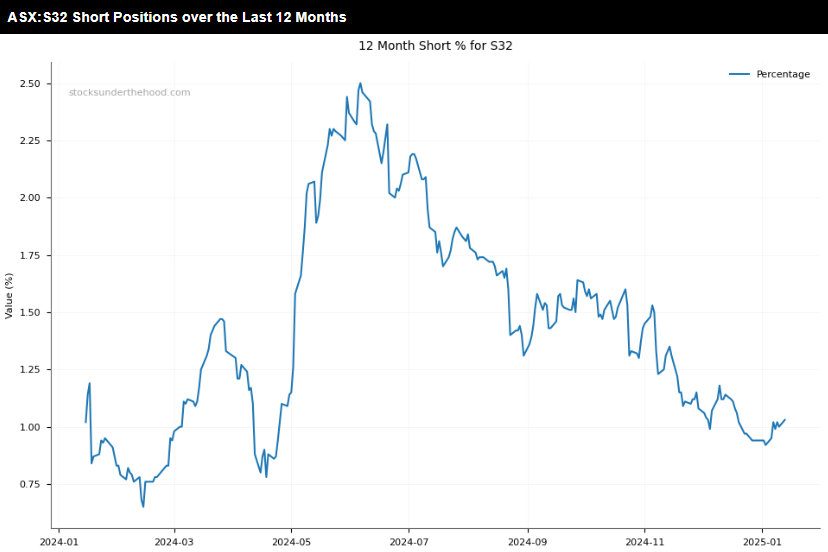

Uranium (BOE, PDN & DYL)

Boss Energy (BOE): Medium term, share price falling, Shorts rising

Paladin (PDN): Medium term, share price falling, Shorts rising

Deep Yellow (DYL): Medium term, share price flat, Shorts rising

Nuclear demand is supposed to be increasing right? Uranium is a great investment right?

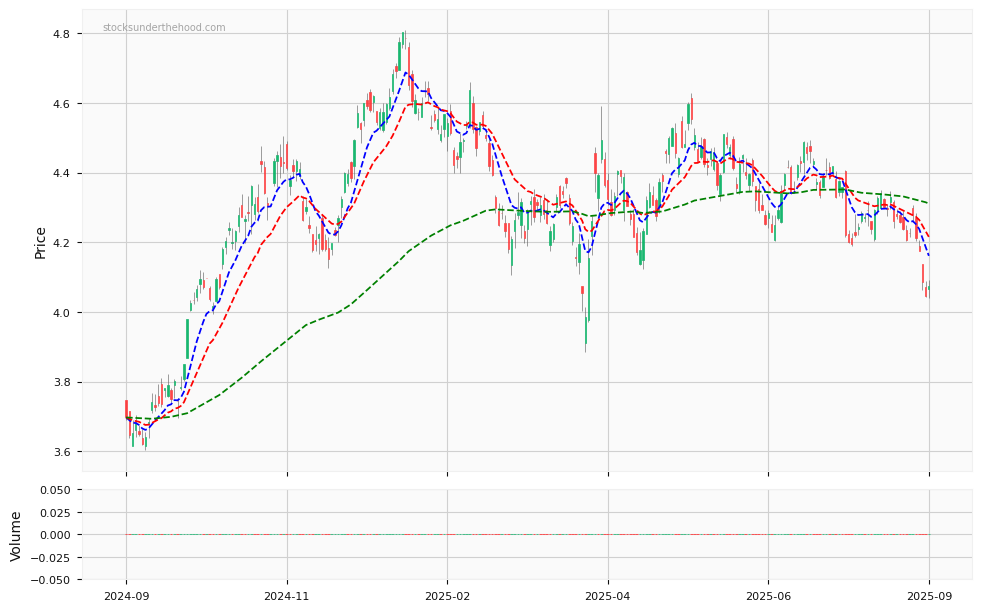

The blue line in the chart represents the spot uranium price, which has fallen 33% from its peak. This may surprise some, as much of the commentary around uranium has been bullish. However, the short positions in these three uranium stocks are simply following the trend in uranium prices.

Lithium (PLS, MIN, LTR)

Pilbarra Minerals (PLS): Medium term share price falling, short positions falling

Mineral Resources (MIN): Medium term share price falling, short positions rising

Liontown Resources (LTR): Medium term share price falling, short positions flat

The same can be said for Lithium (blue line). Mineral Resources has had some other issues which some would like to blame for the fall in share price. That may or may not be the case but it’s clear they have been swimming against they tide of a falling Lithium price.

Medium term share price rising, short positions flat

Silver prices are up, and so is ADT. So why is there a large short position? Without a deep analysis, one possibility is that short-sellers anticipate a capital raise. ADT currently has $59M in cash and $176M in debt, which is concerning given their negative cash flows.

Medium term share price rising, short positions falling

Similar to ADT, Genesis Minerals’ share price has been rising, largely in tandem with the gold price. A couple of years ago, the company set ambitious growth plans, which came with significant execution risks, making it an attractive target for short-sellers. However, over time, they have successfully delivered on their strategy. As a result, short positions have steadily declined over the past 12 months.

Medium term share price falling, short positions rising

Oil prices have been in a downtrend since April 2024, and Karoon’s share price has followed suit, with short positions rising. Textbook shorting strategy.

Medium term share price down, short positions flat

The graphite market has been pressured by increased Chinese synthetic supply. SYR has $81M in cash and $221M in debt, with no cash flows, making it an ideal short-selling candidate.

Medium term share price flat, short positions flat to down

This one is more complex, but its 9% short position cannot be ignored. The key rare earth element, Neodymium, has remained flat in 2024. LYC also trades at a high price-to-earnings ratio (PER) of 40, which is steep for a cyclical resource company. That valuation is likely what attracts short-sellers.

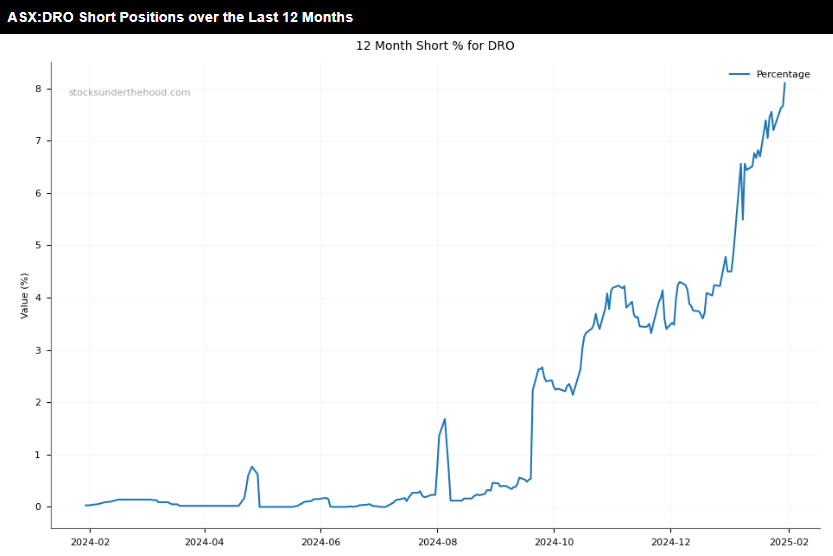

Medium term share price down, short positions up

A fallen angel. Once a market darling, DMP is now struggling to find growth in Australia and its expansion into Japan has been challenging. With $1.4B in debt, it’s easy to see why short-sellers are betting against it.

Medium term share price down, short positions flat

Another fallen angel. A former high-flyer, IEL has struggled to find growth in recent years, much to the delight of short-sellers.

Medium term share price down, short positions up

The well-documented problems at The Star, combined with a significant debt burden, have made it a prime target for short-sellers. The share price chart resembles those of companies that ultimately went bankrupt. Can they turn it around, or will they meet the same fate?

Medium term share price down, short positions up

Same story as IEL—a former market darling that has been re-rated as growth slowed.

Medium term share price down, short positions up

Yet another high-flyer that has fallen back to earth as growth has slowed.

Medium term share price down, short positions up

Another fallen angel that got ahead of itself before being re-rated when growth rates slowed substantially.

Medium term share price down, short positions up

Similar to JLG, re-rated as growth slowed.

Medium term share price up, short positions up

After a big fall, CTD shares have been rallying. However, short positions remain high. Valuations are now more realistic, and the balance sheet looks healthy. Will short-sellers be forced to cover, or will CTD disappoint the market?

Medium term share price down, short positions up

Balance sheet is safe after two large capital raises at peak prices, but profitability remains uncertain. Their latest cash flow report suggests profitability is still a long way off.

Key Observations

- 11 of the 20 are resource stocks

- 3 uranium stocks

- 3 lithium stocks

- 1 silver stock

- 1 gold stock

- 1 oil stock

- 1 graphite stock

- 1 rare earths stock

- 8 of 9 non-resource stocks are fallen angels

Short-Seller Strategy

✅ Target resource stocks when the underlying commodity price is in a downtrend.

✅ Short high P/E companies once growth expectations fail to materialize.

✅ Focus on businesses with high debt, especially those that may need to recapitalize or risk default.

Conclusion Most Shorted ASX Stocks 5/2/25

Taking a long position in the most shorted ASX stocks as of 5/2/25 requires strong conviction. So far, short-sellers have executed their strategy exceptionally well. Genesis Minerals (GMD) stands out as the only major exception, where they may have got it wrong.

Their success rate remains impressive, especially with the ASX near all-time highs. However, nothing lasts forever. At some point, a few of these companies will recover, and when they do, large short positions could fuel a sharp and sustained rally.

Disclaimer: This information is provided purely for educational purposes. It takes no account of an individual’s personal financial circumstances and hence can in no way constitute financial advice. The above data may be subject to errors or inconsistencies for which the author takes no liability. It is imperative that all investors do their own research or if they need advice, seek it from a qualified financial adviser.

Most Shorted ASX Stocks 5/2/25